Healthcare review Q4 2022

What's happening in healthcare?

Private healthcare is robust. Q4 M&A was down on the previous quarter, but superlative activity in that period makes it an unfair comparison for subsequent months.

The stability of the last quarter and the interest of real estate investment trusts in healthcare assets - returning to action after the fallout from the mini-budget - may be a better barometer of the sector's long-term fortunes.

This is all happening in the context of a lot of operational challenges in the market, around staffing pressures, uncertainty around what fee rates/funding will do this year and growing regulatory activity in a post-pandemic environment. However, the sector's underlying demand and supply appeal remains. This will start a race to quality as the struggling operators really struggle and the good operators become even more attractive.

You'll find out about all this in our latest quarterly review.

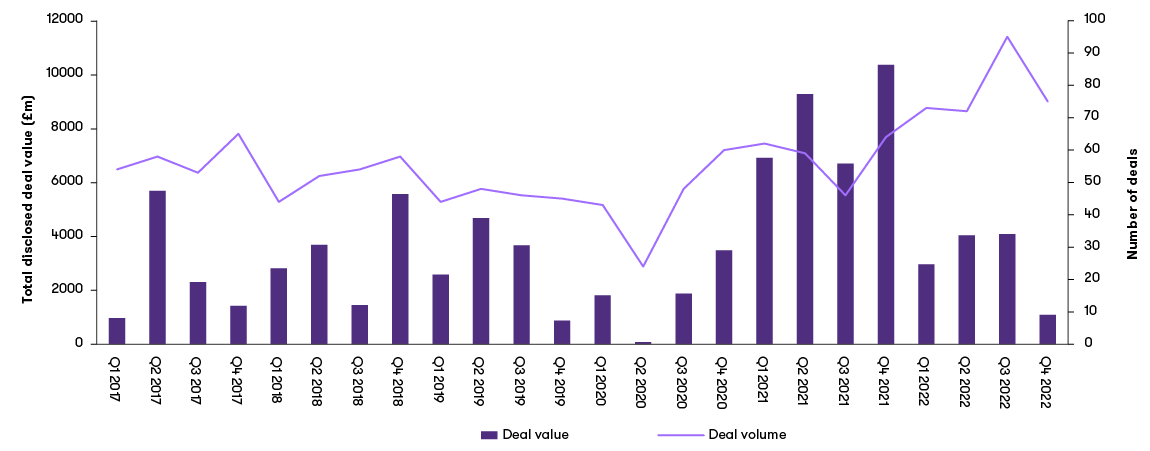

While deals activity in the private healthcare market is down from last quarter the sector is proving robust in all areas considering the economic climate. We've seen continued investment from private equity (PE) and private buyers from both the UK and abroad.

Announced M&A activity in healthcare (quarterly)

This quarter has seen investor interest across many of the private healthcare subsectors. PE activity has reduced this quarter, which is in line with overall M&A activity in the private healthcare market. 42% of the Q4 deals still had private equity involvement, which is just 8% down from last quarter.

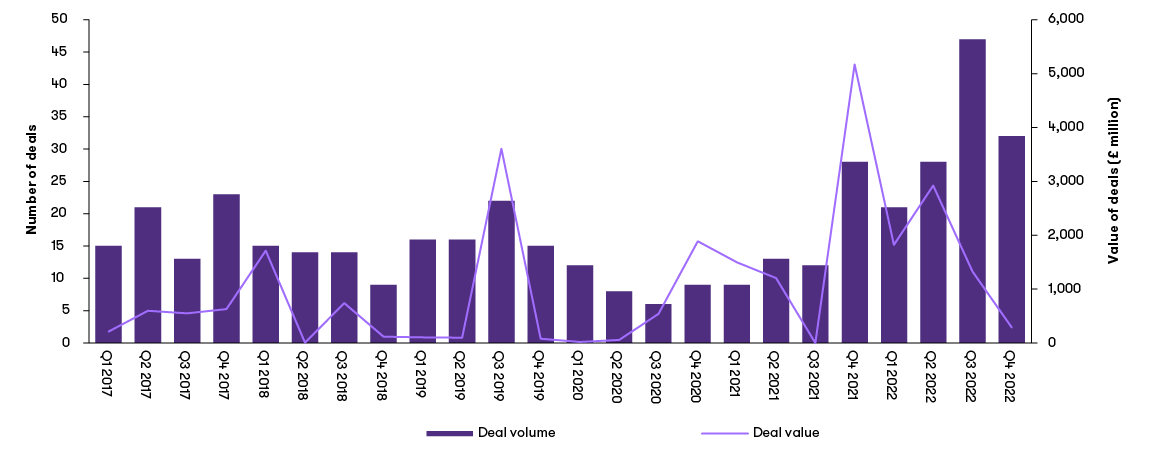

Announced PE activity in Healthcare (quarterly)

Elderly care

Social care has seen a slight decrease in activity, but still remains a core focus for investors. While the European REITs haven't been as active this quarter, we've seen Aedifica continue to invest in this market with the acquisition of one operational care home and two sites to build two new care homes. The Sanctuary Housing Association has acquired Cornwall Care, which operates 16 care homes in Cornwall and Tristone Healthcare Ltd has acquired K Bond Healthcare Ltd (trading as Next Steps), a Manchester, UK-based residential and nursing care services provider. Santerre completed their acquisition of 49 Caring Homes care homes, uniting the ownership of the property and operations of the 49 homes.

Specialist care

The Specialist care market has continued activity through this quarter seeing Civitas acquire a £200 million property portfolio from CareTech under a sale and leaseback scheme, this follows the privatization of CareTech backed by Three Hills Capital in June 2022. At the end of the quarter, Civitas also acquired through specialist care provider ivolve Group (previously Envivo), Cavendish Care, who we advised.

Q4 also saw Swanton Community Care, backed by Apposite Capital make four acquisitions. They acquired Deanston House Ltd, a UK-based disabled adults care home operator, Freedom Care and Support Ltd, a UK-based supported living and home care services provider; Child and Family Services (CFS); and Care Homes for Adults with Disabilities (CHAD). These acquisitions will give Swanton the ability to expand through the local hubs.

Medical devices

The medical devices market remains interesting to investors in the UK and abroad. KKR has acquired a majority stake in CliniSupplies Ltd which supply chronic care medical devices. Halma plc has acquired IZI medical the US developer and manufacturer of radiology and imagery medical devices. UK medical device developer Nexa Medical UK Ltd was acquired by the US medical device manufacturer Advance Oxygen Therapy Inc.

Digital health

As private healthcare continues to move into the digital space, we continue to see the digital health market grow with interest from investors and overseas buyers. Octopus VCT plc led a group of investors to invest in HelloSelf Ltd, the local provider of a digital therapy service platform. The UK-based menopause app Vira Health acquired Alva, a UK-based menopause treatment prescriber. Palatine PE invested in Redmoor Health Ltd, a UK-based digital healthcare technology consulting, web design and marketing services provider, and August invested in Onetouchtelecare Ltd, the Ireland-based healthcare patient and staff SaaS provider.

Retail healthcare

The retail healthcare market saw sustained motion this quarter, which is very positive for the sector considering the economic climate. We advised on the sale of Veincentre Ltd a UK-based varicose veins treatment clinic operator to CBPE Capital LLP. Dentex resumed its acquisition path with the acquisitions of four dental groups, Rory Morris Dental Excellence, Alex Jones Dentistry Ltd, Hedon Dental practice and Edward House Dental Studio. RCI Group, part of the Literacy Capital portfolio has acquired Prometheus a healthcare services company providing support to individuals with mental health needs. Spire Healthcare Group has acquired The Doctors Clinic Group Ltd, a private GP office operator for a consideration of GBP 12 million.

Pharma services

Once again pharma services have proved a very appealing subsector of private healthcare for investors. M Ventures headquartered in the Netherlands has invested in Nucleome Therapeutics Ltd, the biotechnology company and Storm Therapeutics Ltd, the UK-based research laboratory, focused on the identification and development of small molecule drugs. Aspire Pharma, owned by H.I.G Capital acquired Morningside Pharmaceuticals Ltd, a UK-based pharmaceutical products distribution services provider. RxCelerate, an international out-sourced drug discovery and development platform, acquired Methuselah Health UK Ltd a drug discovery company, the launch of ProQuant, a proteomics service has followed this acquisition.

Three key deals

Veincentre

Veincentre is a leading private provider of varicose vein treatments, founded in 2003 by husband and wife, Dr David West and Deborah West. Palatine Private Equity’s Impact Fund invested in the business in 2019 and substantially grew the clinic base across the UK. The business has focused on increasing the accessibility and affordability of treatment; serving to both alleviate the burden on the NHS, and increase the number of individuals who have benefited.

Having invested in and successfully exited SpaMedica earlier in the year, with healthcare and pharmaceuticals being a core sector, CBPE were both management and the founder’s preferred partner – based on their extensive knowledge of private healthcare clinic rollouts and commitment to the delivery of the Veincentre values.

Cavendish Care

Cavendish Care is a specialist care provider located in the South-East of England, providing residential care and supported living for adults with learning disabilities and challenging behaviours. The business has been family-owned and run since its inception 25 years ago, developing into an important asset to the local community.

Civitas Investment Management Limited is a fund manager dedicated to investing exclusively in social care and social infrastructure in the UK. Civitas and ivolve Group established a partnership in 2018 to acquire high-quality specialist care operators in the UK. This acquisition represents their eighth acquisition since the inception of the partnership and provides them with an established footprint in the South East of England.

ivolve Group, formerly known as Envivo Group, recently entered the market following its integration of existing providers Heathcotes, New Directions, and TLC Care and Support into a new enlarged brand name. With the acquisition of Cavendish Care, ivolve Group becomes one of the largest social care providers in the UK.

Alva Health Limited

Alva runs an online portal where women experiencing menopause can be prescribed hormone replacement therapy, specific hormones that boost oestrogen in the body and relieve symptoms.

UK-based Vira Health founded in 2019 is a digital healthcare company that has created an App ‘Stella’ that supports women through menopause by combining data, clinical best practices and behaviour change to solve the health and quality of life problems that affect billions of women worldwide.

Vira acquired Alva as part of its expansion in the UK following the launch of a government-led Menopause Taskforce to change societal attitudes. Co-Founder Rebecca Love says “Acquiring Alva allows us to rule out alternative conditions, diagnose their stage of menopause and, when appropriate, recommend the appropriate HRT for their specific symptoms.”

Healthcare M&A Outlook

The activity above shows that the private healthcare market maintains strength in all areas. We're still seeing continued investments from private equity and commercial firms in the UK as well as abroad. We've seen a slight downturn in the volume of deals this quarter compared to the previous quarter, but the volumes remain in line with the start of 2022.

Looking back at 2022, private healthcare has sustained growth and activity despite the unpredictable markets, while elderly care picked up activity following COVID-19, but activity did slow with the cost-of-living crisis. The digital healthcare market has been an area of keen interest which we would expect to continue in 2023, as more companies and associations introduce digital solutions to improve services and care.

We anticipate that the 2023 market may prove difficult for some, but the private healthcare sector has shown to be resilient in the past and has been a continued area of interest for investors.

For more insight and guidance, get in touch with Peter Jennings, Dan Smith and Matthew Stannard.

The UK government introduced real estate investment trusts (REITs) in 2007 as a tax-efficient wrapper for individual and institutional shareholders to get exposure to real estate without holding assets directly. They offer diversification and liquidity as investors can sell their shares if they decide to exit. Their popularity in private healthcare (and other sectors) grew significantly in the extended period of low-interest rates: focusing on private pay elderly care, local authority, primary care, specialist care, and supported living. These sub-sectors have a reliable rent-paying tenant base, which is set to grow as the population ages.

From success to slowdown

The final quarter of 2022 saw a dramatic change in fortune. Throughout the year REITs were quietly getting to grips with challenging macroeconomics as the pandemic recovery and the war in Ukraine drove global inflation. In response, central banks sought to tame this rise by increasing interest rates. Then came the turmoil of Liz Truss's mini-budget. Returns dropped, lenders closed shop, and asset values fluctuated.

The storm, however, may have accelerated an inevitable correction. REITs couldn't enjoy a period of close-to-zero base rate forever. The end simply came sooner than expected. Share prices fell sharply in the expectation that asset values would decrease to provide an acceptable return for investors above the higher cost of capital.

However, with inflationary pressures set to recede and more visibility on base rates, it seems REITs are back in business. The green shoots of recovery are shown in an uptick in equity markets since the beginning of the year, particularly in the US – often an indicator of the UK's performance. Another positive signal is the completion of several private market deals in Q4 and January.

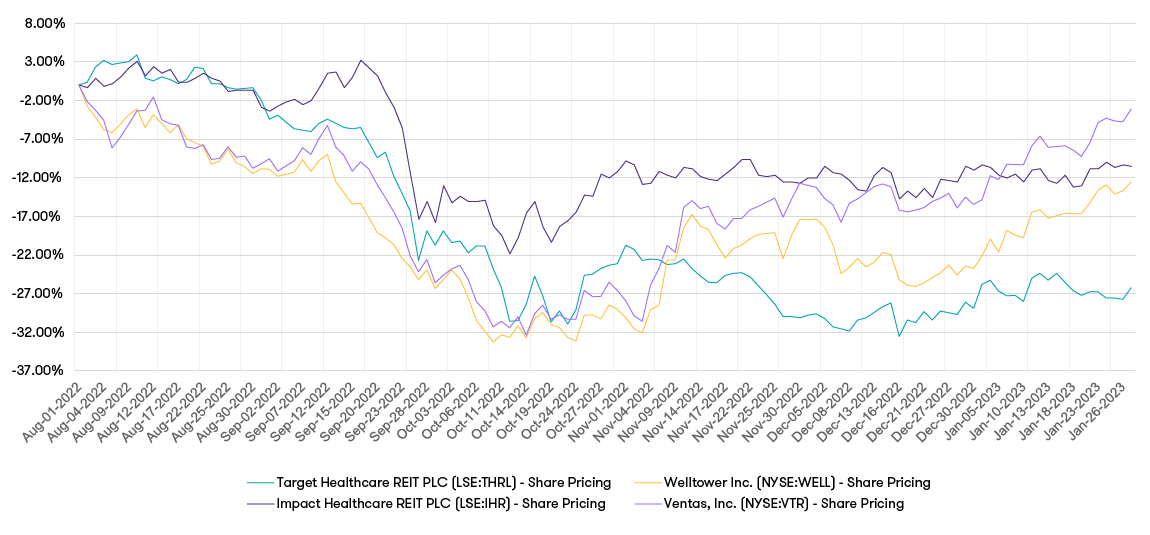

Figure 1: share prices from a selection of US and UK REITs. Source: Capital IQ

Safety in scale

REIT shareholders expect (at least) a better return than government bonds to provide an appropriate risk premium. They need sound operating models, strong management teams, and well-structured balance sheets to deliver this amid high-interest rates. In addition, they need scale. Larger REITs benefit from a lower cost of capital, so they can cut rents in a downturn, and invest in their buildings to combat depreciation and make them 'green'. Looking back on recent takeover activity that our teams advised on shows how these factors may come into play in the year ahead.

REITs get active – the key deals

Impact Healthcare REIT acquires six care homes from Morris Care

Impact Healthcare paid Morris Care £56 million for a portfolio of six care homes (438 beds, with 400 ensuite rooms). The operational management team of Morris Care will transfer to Welford Healthcare (an existing Impact REIT tenant and operating partner.)

The deal was financed partly by cash and partly with an issue of impact shares. Structures like this – where REITs issue shares in full or part consideration for acquisitions – give the seller exposure to a more diversified portfolio. It also gives them liquidity in the form of shares.

Civitas acquires Cavendish Care

Civitas Investment Management REIT partnered with Ivolve Care (formerly Envivo) to acquire Cavendish Care, a specialist provider providing residential care and supported living for adults with learning disabilities and challenging behaviour.

This is the eighth acquisition by Civitas and Ivolve since 2018, giving them an established footprint in South East England. It is an example of a successful PropCo/OpCo partnership.

Civitas Investment Management REIT acquires adult specialist care homes from CareTech

Civitas is the first REIT dedicated to investing in social care housing and healthcare facilities. In December 2022, it announced a £200 million sale and leaseback of a portfolio of special schools, children's homes and adult specialist care homes from CareTech.

The deal shows REITs going into adolescent care for the first time. This exemplifies a trend of larger REITs looking for adjacencies to their primary offering, which can benefit from economies of scale.

Activity spotlight

FTSE 250-listed LXi REIT plc completed a public takeover of AIM-listed Secure Income REIT plc to create a company with a combined portfolio of 346 properties in the UK and Germany and a valuation of £3.9 billion. Our team provided buy-side tax advisory.

Workspace Group plc completed a £272 million takeover of McKay Securities plc to bolster their flexible office portfolio. Our team provided buy-side financial and tax advisory.

Why partner with a REIT?

A third funding option

Debt and equity markets are still hurting from economic turmoil. A REIT joint venture provides healthcare operating companies with an alternative source of capital. This was the case following the 2008 global financial crisis. More recently, in November 2022, Northwest Healthcare Properties, a Canadian REIT, announced a £500 million joint venture with an unnamed UK investor to support UK healthcare real estate.

Clarity on pricing

One of the main challenges in M&A across all sectors is the recalibration of price expectations following the economic downturn. However, recent REIT completions provide a readymade guide for anyone looking to sell this year. In addition, REITs' listed status makes their performance publicly visible to potential partners, creating clarity during dealmaking.

Expertise in Real Estate and ESG

Successful REITs understand that a prosperous tenant drives solid shareholder returns, and have expertise in areas such as property management and ESG to help. Affordable rents provide dependable returns for investors, and extending lease terms can, in turn, have a positive impact on asset values and investment attractiveness. It's a win-win for operators and REITs. A good example (albeit from another sector) is LXi, which in December agreed to a lease re-gear to give its partner Travelodge Hotels more affordable terms.

The outlook for REITs in 2023

REITs offer a viable option for private healthcare companies looking to sell or raise funds in 2023. First, it's essential to find the right REIT, preferably a sector specialist that will help tenants grow. Operators should avoid mistakes made by Southern Cross, which famously failed due to over-renting and committing to leases with upward-only rent reviews. They must also ensure that their tax structure is attractive to REITs.

In turn, REITs have a window of opportunity to seize healthcare investment amid reduced competition from debt and equity markets. However, they should also acknowledge that amid the positives, recovering from an interest rate shock means that the economy is still difficult to predict.

For more insight and guidance, get in touch with Peter Jennings and Matthew Stannard.

Care-home profitability has been on a downward trajectory for the last decade. The uncertainty and disruption of 2022, not only worsened the position of operators already struggling to balance the books but introduced extra challenges for those who thought they had a healthy operating model.

The cost of living is hitting homes

At the start of 2022, Laing Buisson estimated a 30% increase in operating costs, comprising utilities and food; higher insurance costs in the wake of the pandemic; and staff shortages exacerbated by Brexit. The actual rises, however, could be much more.

Consumer price inflation in December 2022 was c.11%. While it may reduce depending on the extent of government support, the pain is likely to continue for some time. Staple foods, such as bread, meat, dairy, oils and fats are seeing inflation of between 16% and 29%. The Financial Times has reported that care-home providers face insurance rates of up to four-times pre-pandemic levels: potentially putting many at risk of going out of business.

Nurses and care workers

Staff are by far care homes' most valuable resource. In the last 12 months, staff have been lost faster than they can be recruited, resulting in an increased reliance on more costly agency workers. Staffing is impacted by increases in the National Living Wage, with a further rise from £9.50 to £10.42 being implemented from 1 April 2023.

The severity of recruitment and retention issues in the sector is well demonstrated by care workers leaving for supermarkets and retailers. Some might say this is because society doesn't value the work being done in social care, however, other employers outside the healthcare sector do pay more than the minimum wage, and some even offer a joining bonus.

A recent Care England survey of c.70,000 beds in England, advised that over 88% of providers reported difficulty securing agency resources and that rates had more than doubled between 2019 and 2022.

Utilities and the energy crisis

Energy is a significant cost for care home providers and is a serious concern for those who were unable or failed to hedge their utility costs. Energy broker Box Power CIC and Care England reported that energy costs for care homes had increased dramatically during 2022, with its latest reports finding a significant increase in costs:

- August 2021: energy costs were c.£660 per bed per annum/ £13 per week

- July 2022: energy costs were c. £3,950 per bed per annum/ £76 per week (433% increase on August 2021)

- August 2022: energy costs were £5,166 per bed per annum/ £99 per week (683% increase on August 2021)

Care England advises that most providers who hadn't re-contracted their energy costs in the last 12 months expected very significant price increases. This is because providers with less than 1,000 beds are unlikely to be on a fixed-price energy contract as their volumes aren't conducive to a hedging policy.

- The Energy Bill Relief Scheme and then the Energy Bills Discount Scheme (EBDS) will discount energy costs for businesses until April 2024, although as it is a discount and not a price cap, care homes could still see an increase in their utility costs. If providers are required to move onto fixed price contracts, which could see more than six-fold increases (despite the EBDS discounts), these costs won't be affordable.

What does the future hold?

For some operators, the future could be bleak. Years of long-term austerity, coronavirus, spiralling costs, and the staffing crisis are combining to create the most challenging year the sector may have ever faced.

Predicting the future of the energy market is impossible and it's uncertain how much support may actually come from the government. This position is further exacerbated by the certainty that inflation is high and may remain so for a while, placing upward pressure on operating costs, and leaving no opportunity for real cost savings. Furthermore, commentators expect the Bank of England may increase interest rates to over 5% by mid-2023, placing further pressure on providers with high levels of borrowings.

It now seems inevitable that the government will need to provide some additional financial support in the coming months and beyond, or face the real prospect of some homes closing down, precisely at the time when they're needed the most.

For more insight and guidance, get in touch with James Hichens.

Get the latest insights, events and guidance about TMT straight to your inbox.

![]()