Fair value represents a step-up in the Financial Conduct Authority's expectations in relation to consumer outcomes. Demonstrating compliance will be a challenge so how can financial services firms get proactive? James Clarke looks at how to assess consumer outcomes and address potential product gaps.

Contents

Fair Value is one of the four outcomes outlines in the FCA's Consumer Duty. It seeks to provide context for how firms should assess whether the price of their products and services offer fair value to help strengthen the firm-consumer relationship. In turn, firms have the opportunity to improve their internal business performance and enhance consumer engagement by ensuring they're meeting best practice.

A new Consumer Duty

The new Consumer Duty provides an opportunity for you to review your product offerings to consider how they may improve value for your customers – and also customer trust and business value as a whole. But the Consumer Duty sets a higher bar for firms to demonstrate that their products deliver good consumer outcomes:

Products and services – products and services must be fit for purpose, and their design must meet the needs, objectives and characteristics of the targeted consumer

Price and value – consumers must receive fair value from products, such that there's a reasonable relationship between the price of a product and the benefits received from it

Consumer understanding – communication from firms must empower consumers to make informed decisions

Consumer support – support from firms must meet the needs of the consumer throughout the product’s life

These four components are considered key to the formation of a healthy customer-firm relationship. Assessing fair value in a data-driven way will help identify potential risks early and ensure you have the necessary economic and financial resources in place to get it right and meet best practice.

Test for fair pricing

The Financial Conduct Authority (FCA) wants to establish a clear and consistent expectation for how firms assess whether the price of products and services offers fair value. The FCA’s expectations are based on a ‘reasonableness’ test. In practice, this means that you're responsible for outcomes that are foreseeable and within your grasp to control.

Potential tests for fair pricing:

Internal benchmarking – value consistency across comparable products internally within the firm

External benchmarking – value consistency across comparable products both internally and externally with other comparable products on offer from competing firms

Cost modelling – the degree to which prices are dislocated from underlying costs

Consumer research – reaching out to customers through surveys and similar methods to gauge how customers value products

Equality analysis – the degree to which protected and vulnerable customers are discriminated against

Compliance and gap analysis – the gaps in compliance and implementing a plan to address such risk areas

What to consider when testing for fair value:

Fair value must be assessed across a product’s life cycle, allowing for the price to reflect changes to costs and risks associated with the product

Firms must be aware of any deviations from fair value that their products experience, including their magnitude and duration

A variety of customer needs, characteristics and objectives should be considered

Firms can carefully bundle together similar products in their assessment of fair value, providing that their customer base, complexity and risk of consumer harm is sufficiently similar

The methodology used to assess fair value must demonstrate that the cost, price and benefits of the product are commensurate to the product and customer characteristics

To help firms create a fair value framework, the FCA recently published its findings from its review of 14 fair value assessment frameworks. It found that while firms are making substantial efforts to meet fair value requirements on time, there were questions as to how effective these efforts would be in practice. The FCA recommended four areas for further consideration:

Ensuring the collection and monitoring of evidence demonstrates that fair value is present in products and services

Ensuring clear oversight, and the accountability of remedial actions should they not provide fair value

Ensuring that all customers within a portfolio are accounted for when assessing fair value, such that broad averages are insufficient in demonstrating fair value for all customer groups

Ensuring summaries and the presentation of fair value assessments enable decision makers to discuss whether a product represents fair value, including any limitations in the analysis or evidence provided.

Bespoke economic analysis that helps you make the right decisions.

Learn more about how our Economic consulting services can help you

Assessing the fair value of mortgages can be complex and time-consuming due to how elaborate the process can be and the difficulty in making the right decision when designing the mortgage product. There's significant scope for variation in product and customer characteristics, as demonstrated in the table below.

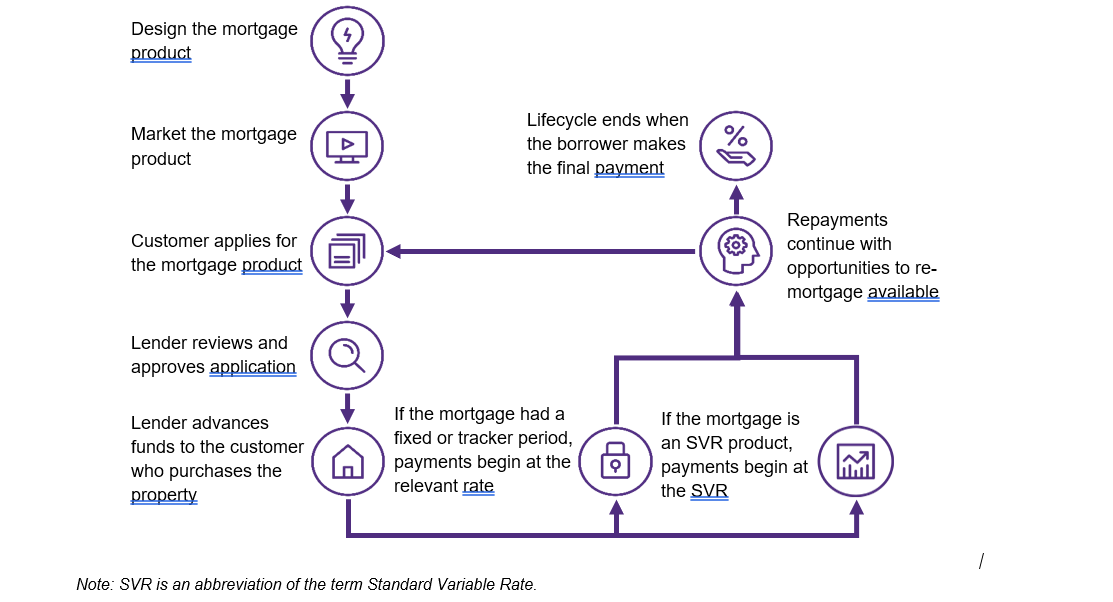

Life cycle of a mortgage product

There are several key decisions in the mortgage product life cycle – and points at which lenders would likely be expected to assess fair value. At these stages, product features may alter substantially, such that fair value considerations are triggered anew. Fair value assessment may also be appropriate when there are market developments that impact on whether a product is likely to be considered fair value. For example, changes in the cost of capital, changes to benchmark rates such as the Bank of England base rate, or house price changes.

Exercises to evaluate the fair value of mortgage products

Internal benchmarking – when assessing the fairness of a mortgage portfolio, internal benchmarking allows you to recognise mortgage products that are less competitive than others available from the same lender; this might be tested through fees, interest rates or other metrics

External benchmarking – this methodology can be used to demonstrate whether a mortgage product aligns with similar mortgage products offered on the market; commercially available datasets allow mortgage products to be compared across time, segmented by numerous characteristics

Cost modelling – this methodology can benchmark costs against the profits associated with a mortgage product, while considering factors such as the level of risk inherent in a portfolio; it's particularly useful for mortgage products as their cost structures are often complex

Similar methodologies can be employed to assess the fair value of products across other sectors, such as insurance products. By following these steps, you can enhance current models to ensure you comply with Consumer Duty rules.

Benchmarking the fair value of mortgage products

Benchmarking is a robust approach to assessing fair value that relies on identifying products with comparable features and assessing whether prices are comparable. It's important to distinguish internal and external benchmarking to make the most of its functionality.

Internal benchmarking methods involve assessing internal value consistency – a necessary but insufficient condition in achieving fair value. In such an assessment, the objective is to demonstrate that the benefits associated with a product can't be obtained at a significantly lower price from another product within the portfolio.

The methodology groups a lender’s internal products into comparable buckets according to product and customer characteristics. For instance, buckets might differ by interest rates. Within each bucket, value is examined both graphically and descriptively to answer the question of whether a sufficiently similar product exists at a far better deal for the customer.

Factors that lead to the outlier might include product characteristics. A key consideration would be the risk profile of the customers who take the more expensive mortgage product. For example, a customer with a greater likelihood of default may not be able to choose from the cheaper products. Other factors such as flexibility, portability or the quality of service provided to the customer might also lead to the outlier. Where such discrepancies exist, an analysis of any differential benefits should be undertaken to capture differences in customer value.

Plotting measures of these additional benefits against the upfront fee and/or the interest rate of the mortgage product will help gain an understanding of whether the product represents fair value. If a product has similar additional benefits to the other mortgage products despite the additional costs to the customer, then it may be deemed unfair and possible remedies should be considered.

Internal benchmarking can't measure fairness across firms, however. This limitation means unfairness may not be picked up through internal benchmarking alone as the unfairness may be inherent in an entire firm’s portfolio. External benchmarking may provide the solution.

External benchmarking is more robust than its internal counterpart. It involves conducting a comparison of products across firms, as well as within firms, to investigate whether the product represents fair value when compared to the entire market’s offerings. Given the number of products involved and the broader differentiation, the additional robustness does come at the cost of additional complexity.

External benchmarking also allows for the creation of a simulated price, based on the prices of all other products in the market, against which the price is benchmarked. If the difference between the actual price and the simulated price is sufficiently large, further consideration needs to assess whether the product offers fair value. For mortgages, revert rates (standard variable rates) – that is interest rates applied on mortgages after an initial fixed rate period – could be assessed to see if they offer fair value through external benchmarking.

Initially, a descriptive approach compares the SVR of the mortgage product being assessed with the SVRs of all other mortgages in the market. The interest rate of the mortgage product is then compared to buckets of mortgage products that share similar characteristics.

A more robust approach relies on econometric techniques. This approach involves comparing the SVR of mortgages on a like-for-like basis by removing the impact of other product characteristics and factors, such as macroeconomic conditions, on SVRs. More specifically, SVRs are modelled as a function of borrower characteristics, product characteristics and macroeconomic factors. This model is then used to predict a range of interest rates that are consistent with the characteristics of the illustrative mortgage product and the creditworthiness of its customers.

It's important to have a firm grasp over internal and external benchmarking models and how it can be used to enhance your fair value requirements. We're likely to see a variety of changes in the coming year from the regulator on how firms can help their customers and providing a better service, so having oversight over this process is necessary.

The Consumer Duty will be introduced on 31 July 2023 for new and existing products available for sale, and from 31 July 2024 for products in closed books. Firms must assess the fair value of their products in a robust and comprehensive manner, documenting their approach and outcomes before this deadline to ensure they are meeting best practice.