Update - on the 26 February 2025, the European Commission published the Omnibus legislative proposals for sustainability reporting. The proposals, if passed, will impact the scope and timelines set out in this article. We will update this page in due course, once these proposals are finalised. For the latest see Life after the EU Omnibus: Taking a no regrets approach to CSRD adoption.

The Corporate Sustainability Reporting Directive (CSRD) revises the 2014 Non-Financial Reporting Directive (NFRD), extends the scope of covered companies, and strengthens the reporting requirements for them.

Approximately 50,000 companies will eventually be required to report on sustainability, including larger companies and listed small and medium-sized enterprises (SMEs). Approximately a 1,000 businesses individually meet the reporting criteria and have ultimate parent ownership based in the UK.

What are the goals of the corporate sustainability reporting directive?

A key objective of the CSRD is enabling businesses to increase transparency and accountability of their reporting, and give stakeholders insight and guidance through analysis, benchmarking, and auditing. It's also intended to broaden the scope of sustainability management and reporting to include sustainability risks and opportunities. Ultimately, this should encourage businesses to develop a strategy to improve on sustainability.

A guide to the new requirements

The new directive introduces substantial sustainability-related reporting requirements, with small variations for the different companies in scope.

Companies will now need to report:

- Specific details about the business model and strategy, with notable reference to sustainability-related opportunities, resilience, and plans to ensure compatibility with the transition to a climate-neutral economy and the limiting of global warming to 1.5 °C.

- Sustainability targets, including, where appropriate, 2030 and 2050 greenhouse gas emission reduction targets and a description of relevant progress

- The role, expertise and skills of the administrative, management and supervisory bodies for sustainability, and incentives offered to members

- Relevant business policies

- The due diligence process implemented for sustainability matters

- The principal actual or potential adverse impacts connected with the business operations and value chain

- Any actions taken to prevent, mitigate, remediate, or end the identified adverse impacts and their results

- Principle sustainability risks and how they are managed

All relevant disclosures will now extend to the reporter’s value chain, including products and services, business relationships, and supply chain.

Key things to know about the CSRD

Double materiality

Double materiality is fundamental to the new rules. In-scope companies will now have to report on a double materiality basis, identifying sustainability risks and opportunities, and the impact of the company on people and the environment. This means that companies will have to identify both the external impact on society and the environment (impact materiality), as well as the impact on the enterprise value (financial materiality).

close

Companies will now need to report

-

Specific details about the business model and strategy, with notable reference to sustainability-related opportunities, resilience and plans to ensure compatibility with the transition to a climate neutral economy and the limiting of global warming to 1.5 °C.

-

Sustainability targets, including, where appropriate, 2030 and 2050 GHG emission reduction targets and a description of relevant progress.

-

The role, expertise and skills of the administrative, management and supervisory bodies for sustainability. The existence of sustainability incentives offered to those members.

-

The business policies for sustainability.

-

The due diligence process implemented with regard to sustainability matters.

-

The principal actual or potential adverse impacts connected with the business operations and value chain.

-

Any actions taken to prevent, mitigate, remediate or bring an end to actual or potential adverse impacts, and their results.

-

The principal sustainability risks and how those are managed.

This is different to the approach taken by the IFRS Sustainability Standards and the Task Force on Climate-related Financial Disclosures (TCFD), which focus on financial materiality. There's likely to be some divergence for corporates who are in scope of these regulations too.

Sustainability reporting standards

Disclosures will need to be undertaken in accordance with the European Sustainability Reporting Standards (ESRS) issued by the European Financial Reporting Advisory Group (EFRAG). It's indicated that the ESRS will aim to avoid imposing additional administrative burden on international companies who are caught by multiple global reporting requirements, hence they shall be considering, to the greatest extent possible, the work of global standard-setting initiatives for sustainability reporting.

Sustainability assurance

Introduction of an EU-wide requirement for limited assurance on sustainability information with the aim of moving to reasonable assurance in the long term. More specifically, under the directive, the Commission must adopt legislation to provide for limited assurance standards (1 October 2026), as well as further legislation to provide for reasonable assurance standards (1 October 2028). The assurance certification must come from an accredited independent auditor or certifier, ensuring that the sustainability information complies with the certification standards that have been adopted by the EU. It should be noted that there are currently no mandatory assurance requirements on sustainability reporting in the UK.

Which companies are in scope?

Companies already subject to the NFRD. That is, essentially, large EU 'public interest entities' with regulated market listed securities, credit institutions, and insurance companies with more than 500 employees.

Parent companies of a large group. Large groups are groups consisting of parent and subsidiary companies included in a consolidation, fulfilling two of the following criteria:

- A balance sheet total exceeding EUR 25,000,000

- A net turnover exceeding EUR 50,000,000

- An average of more than 250 employees during the financial year (on a consolidated basis)

All 'large' EU companies (including EU subsidiaries of a UK parent) fulfilling two of the following criteria:

- A balance sheet total exceeding EUR 25,000,000

- A net turnover exceeding EUR 50,000,000

- An average of more than 250 employees during the financial year

The total asset and net turnover thresholds have been adjusted to account for inflation, following the adoption of a delegated directive by the European Commission on 17 October 2023.

Listed small and medium-sized enterprises, with lighter disclosure requirements and the ability to opt-out until 2028.

Other EU and non-EU companies (with the exception of micro undertakings) with securities listed on EU regulated markets. Those include debt securities with denominations of less than EUR 100,000 or equivalent listed on an EU regulated market. It's noted that the directive doesn't apply to securities listed on EU multilateral trading facilities.

The pressure to report your ESG progress is growing. Do your targets measure up?

Learn more about how our ESG metrics, targets and disclosures services can help you

Application to non-EU companies

Non-EU companies (including EU subsidiaries of a UK parent) that operate in the EU may also fall under the CSRD scope, regardless of whether they're listed or not. They shall be required to provide sustainability disclosure if:

- their net turnover generated in the EU (at the consolidated or individual level) exceeds EUR 150 million for each of the last two consecutive financial years

- they have at least one subsidiary in the EU (either a large EU company, or an EU company listed on an EU regulated market which isn't a micro undertaking), or an EU branch with an annual net turnover exceeding EUR 40 million in the previous financial year.

Steps you can take now to prepare

Determine in-scope status of your group entities

This may start with identifying entities within your group, which are incorporated in the EU or entities with turnover generated in the EU and considering whether the scope criteria set out in the regulations are met.

Undertake a double materiality assessment

This will bring focus to your CSRD readiness project and enable you to determine for which topics additional disclosure requirements will arise ahead of your first reporting period. This may include policies, KPIs, and targets. We believe this starting point ensures you don’t spend time aligning components that may not be material in light of CSRD principles, but also will provide valuable input for your strategy.

Compare disclosure requirements

Comparing the new disclosure requirements to your current state will help you identify gaps you'll need to address to enable your organisation to comply with the regulations.

Build an implementation roadmap

Having identified the gaps, your roadmap sets out how they will be addressed. Identify who within your organisation will be responsible for this, and, for discussing as a project team, how it will be done.

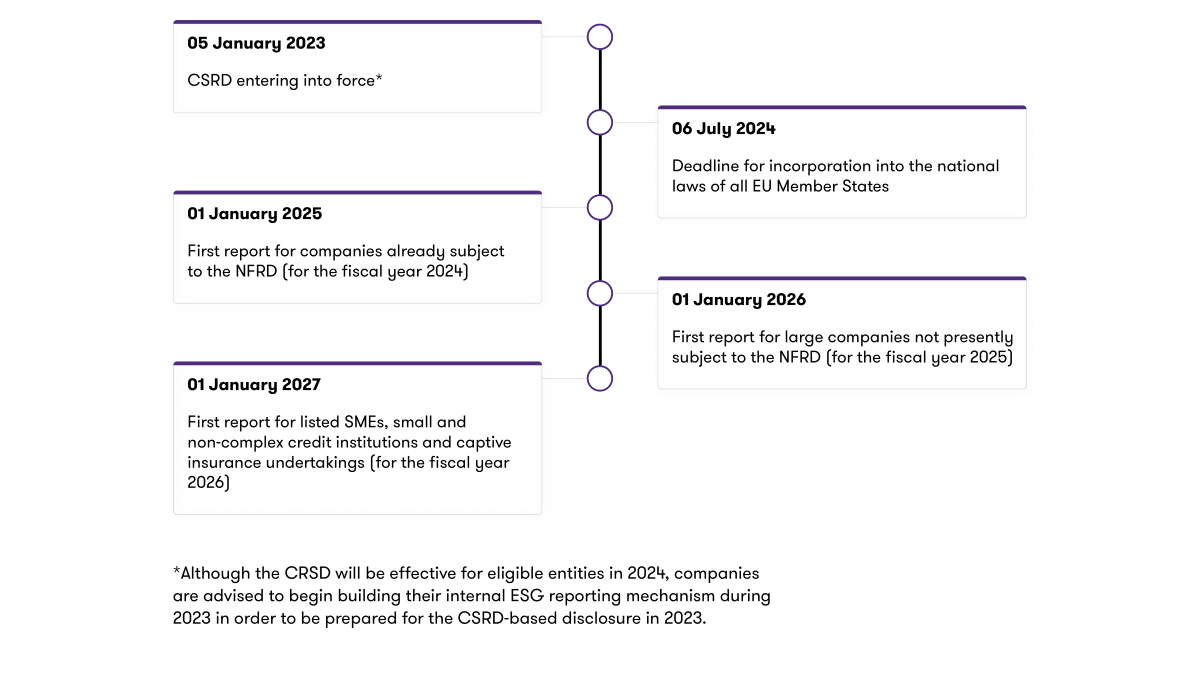

Milestones of the CSRD implementation

![]()

Embedding the positive potential of ESG into the future of your business

Learn more about how our Environmental, social and governance (ESG) services can help you

First time reporting date

Impact of the delay in sector-specific ESRS for EU companies and general ESRS for non-EU companies by two years until 2026

Existing timeline remains, but less reporting is required for EU companies. EU companies must adhere to the general ESRS as planned, following the Commission's adoption in July 2023. Pronouncement by EU Parliament on postponing adoption of sector-specific sustainability standards for EU companies only affects the reporting scope, as the sector-specific impact reporting will not be mandatory until 2026.

Additionally, non-EU companies with turnovers above 150 million euros and their EU branches with turnovers above 40 million euros will only need to comply with general reporting obligations from 2028. The EU Parliament believe that implementing the reporting standards in 2026 will still afford these companies adequate time for preparation.

For more insight and guidance, get in touch with Laura Tibbetts or Rashim Arora (Financial Services). ![]()