As COVID-19 support schemes wind down, restructuring and M&A activity is expected to increase further. Understanding and planning for the tax consequences will be crucial - this is precisely the worst time for an unexpected tax liability. Our team can help you manage this risk, so you can focus on your priorities.

Find out how we're helping our clients and how we can help you going forward.

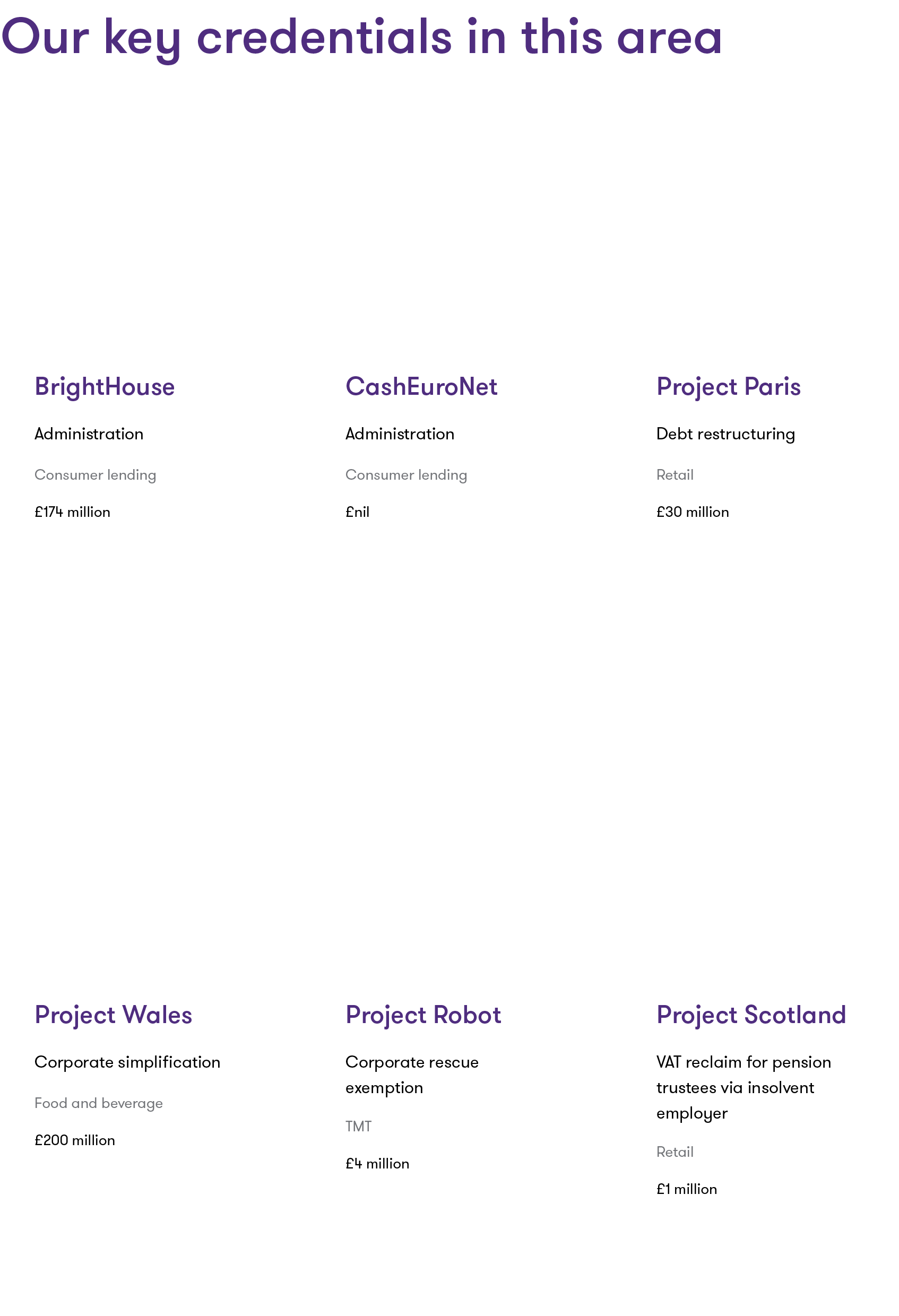

Discover our key credentials in this area

The state of restructuring tax

During 2020 the government introduced various support measures to stave off the worst of the impact of the coronavirus pandemic. Blanket VAT deferrals came in the spring, along with business rates waivers, short term deferrals for other taxes, a more informal approach to time to pay arrangements and several iterations of the coronavirus job retention scheme. Like other creditors, HMRC was prevented from issuing wind-up petitions.

For those able to use them, these measures were helpful, but they brought significant complexity, and in some cases only temporary respite. They have also resulted in many businesses carrying substantial levels of tax debt, which needs to be repaid. How the tax landscape is returned to normal will be the focus going forward.

There are three key issues to keep in mind as 2021 unfolds:

1 Liquidity risks

The re-introduction of HMRC’s preferential status from 1 December 2020, coupled with higher levels of tax debt, will particularly impact floating charge lenders. To minimise their risk, lenders need to better understand their borrowers’ tax status.

Sector-specific risks are also likely to feature heavily. For example, businesses in the construction industry are adapting to changes to the VAT regime from 1 March 2021, which could result in reduced cash flow and higher working capital requirements.

Similarly, restrictions on state aid may disproportionately affect businesses with Coronavirus Business Interruption Loan Scheme (CBILS) or Coronavirus Large Business Interruption Loan Scheme (CLBILS) loans who rely on R&D allowances and repayment credits.

2 Distressed transactions

After a brief hiatus, we are seeing the return of significant transactional activity, often involving distressed businesses. Any transaction involving a debt restructuring can result in tax liabilities, particularly in the context of distress.

There are various exemptions that may be available to prevent taxable credits arising on debt restructuring, but care is needed to ensure the relevant conditions are met. If an exemption is not available, the restriction in the use of brought forward losses could result in tax being payable even though the business has accumulated losses in excess of the profit.

Speaking to our team early is advisable, as well as ensuring any acquisition structure continues to work throughout the life of the investment and, where relevant, upon any ultimate exit.

3 Entity elimination

Current trading conditions and Brexit are highlighting accumulated inefficiencies and risks within a group, and many businesses are taking stock of their structure. With increased compliance costs and personal risks for directors, we are already seeing large multinational groups looking to eliminate surplus UK entities.

For entities that have recently ceased trading, or still have assets or liabilities on their balance sheet, this process can present tax risks that can cause unexpected tax leakage or delays, if not given due consideration.