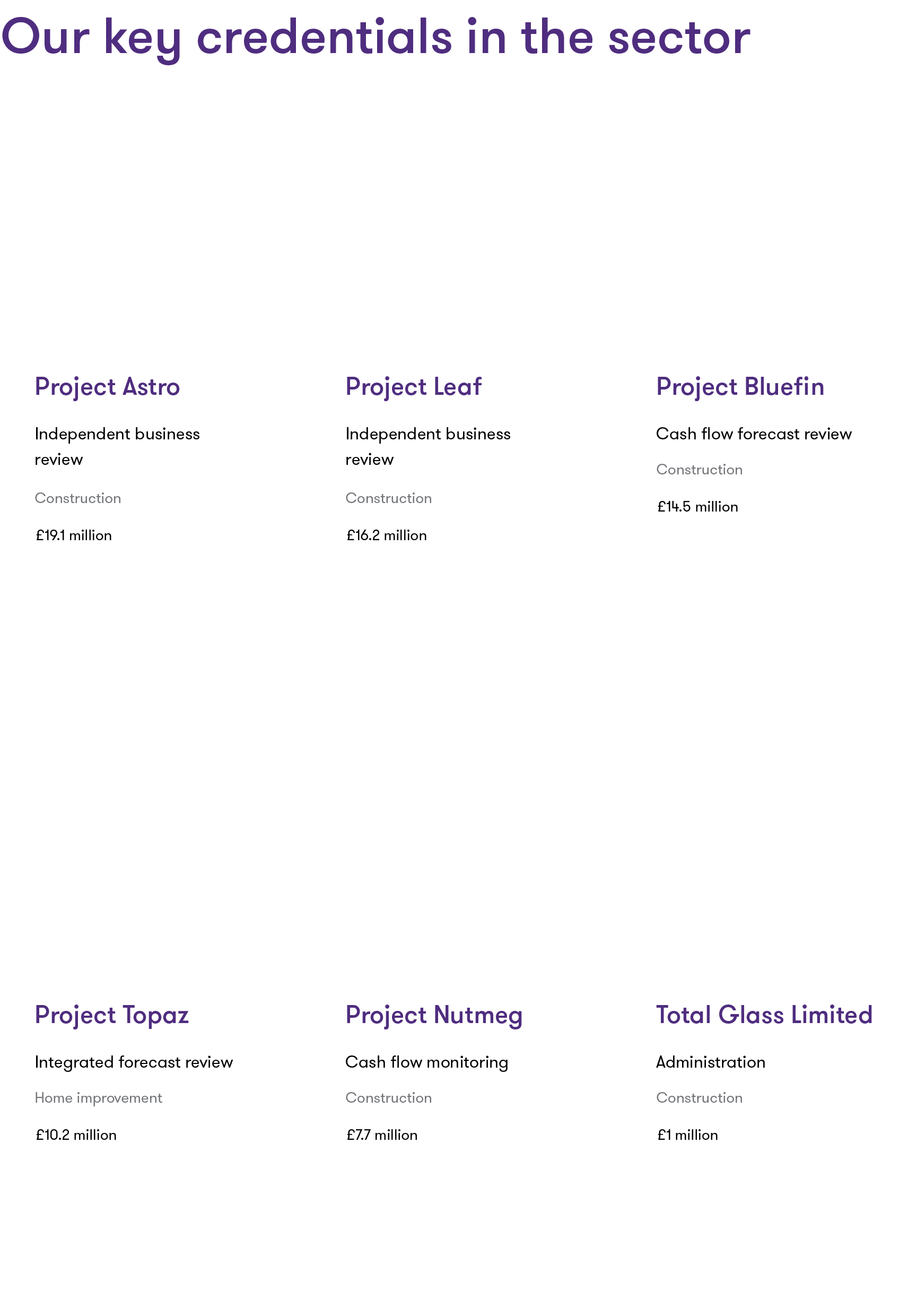

The state of the construction sector

Through our work with construction businesses, we are seeing some common themes coming through. Here are five key issues facing the sector at present:

1 Disruption in supply chain and operations

The initial UK-wide lockdown forced sites to close and workforces to remain at home or be socially distanced.

Construction businesses were then hit by changing restrictions, the uncertainty of future working patterns and the impact of a recession, with the situation more acute for those working in office or retail construction.

Lockdown has also highlighted flaws in the resilience of the sector’s supply chain, which businesses are looking to resolve, as well as enhancing their systems.

2 Continued government support

The construction industry is a significant contributor to the UK economy, typically accounting for 6% of economic output, according to a 2019 government briefing report.

The National Infrastructure Strategy has promised £600 billion across the UK over the next five years. Funding, and access to finance, will be key in rebuilding the economy.

3 Managing cash and working capital

The construction industry is notoriously intensive with working capital, often combined with high levels of capital expenditure.

Any business that has had to pause operations through the coronavirus situation will face working capital challenges, and this will be compounded by the shortened timeframe for completion of projects and the use of stage payments.

Robust cash management procedures and timely reporting processes will be vital for monitoring cash and working capital, particularly as-and-when government support schemes are amended or come to an end.

Businesses also need to understand the cash flow implications of the domestic VAT reverse charge, which must be used for most supplies and construction services from 1 March 2021. Although the effect should be minimal for contractors, sub-contractors and suppliers may experience increased working capital requirements, which could have knock-on effects.

4 Skills shortage versus too many employees

Businesses continue to look closely at costs, including employee numbers. Of the UK workforce, 7% work in construction1.

The sector continues to face a skills shortage, however, and many anticipate this will deepen due to Brexit, as the industry relies on 10% of the UK workforce being non-UK citizens (in London this figure increases to 35%).

Having control over the workforce to ensure continuity of skills, yet flexibility in light of unpredictable periods of downtime, will become an important challenge to the industry.

5 A greater focus on the environment

As the world returns to normal after the coronavirus situation has passed, attention will increasingly turn towards decarbonisation and the impact the sector is having on the environment. This will inevitably add a further layer of disclosure and cost to businesses.

Who will be construction's winners and losers?

Ongoing uncertainty is likely to impact the trading performance of construction companies for the next few years. The effects may be more short term for companies in the healthcare, infrastructure, residential and warehousing sectors but as the government’s support schemes unwind, pressure on working capital will mount. The role of credit insurers in the supply chain is often overlooked but is a key element of the working capital cycle of many businesses. For companies in the office and commercial retail sub-sectors, we expect the impact will be much more pronounced and may necessitate a change in focus.