Syndie: How My Audit Background Shapes My Work in Inclusion

Syndie shares how her career journey from audit and tax to Inclusion and Diversity helps her drive practical, evidence‑based inclusion across Grant Thornton.

By: Jade Palmer, Tristan Rawcliffe

28 May 2024 7 min read

According to the International Energy Agency, the share of electricity in global total final energy consumption in 2022 was around 20%. This demonstrates that electricity generated from renewable energy sources such as wind and solar will be grossly insufficient to decarbonise the global energy system.

Green hydrogen – when renewable energy is used to power electrolysis – offers a potential solution. It can lower emissions in hard-to-abate, energy-intensive sectors, such as steel, cement and fertiliser production, and shipping and aviation.

With numerous projects in the UK and elsewhere in Europe seeking to secure government subsidies and progress to final investment decision (FID), we anticipate growth in the sector. However, the nascency of the industry presents challenges in how to approach the valuation of green hydrogen projects. Despite sharing some characteristics with other more mature technologies in the renewable energy sector, there are also substantial differences which contribute to a divergence in valuation approach.

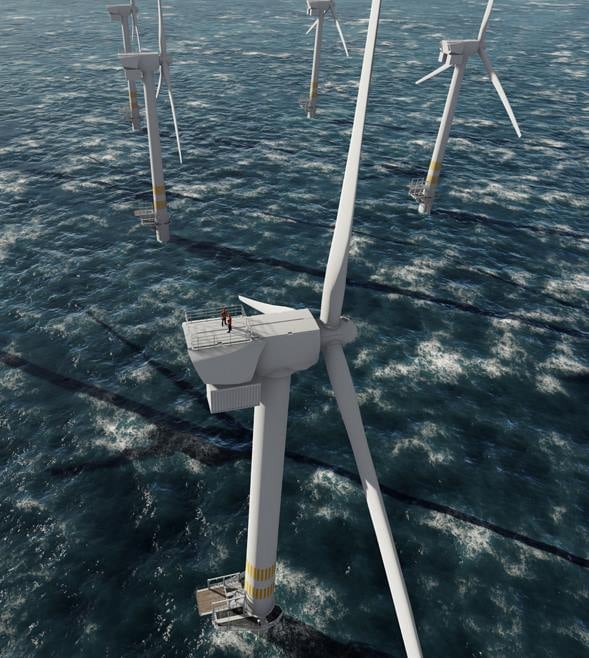

When referring to renewable energy projects here, we're focusing on solar photovoltaic, onshore wind and offshore wind. In our approach to valuing operational or construction stage renewable energy projects, we typically use the discounted cash flow (DCF) as the primary methodology. Revenue, through power purchase agreements (PPAs) or government subsidies, and operating costs, via long term contracts, can often be reliably determined for renewable energy projects, which commonly have finite useful lives of around 25 to 40 years. The DCF approach helps ensure that value is accurately captured over the whole useful life of a project.

Given the emerging state of the green hydrogen industry, obtaining subsidies and securing contracted offtake, often in the form of PPAs, is vital to ensure profitability of a project. Within this article, offtake refers to the purchase by customers of electricity produced by either renewable energy or green hydrogen plants. We've observed forecast useful lives for green hydrogen projects of 20 to 30 years. At a first glance, the DCF may seem the most appropriate approach but the stage of development of many green hydrogen projects and the reliability of cash flows presents challenges.

When valuing pre-construction renewable energy projects, we typically use a market approach, and use an enterprise value/megawatt (MW) multiple determined by reference to transactions for comparable projects. While in theory this approach is also useful for green hydrogen projects, the industry's nascency limits the available comparable transactions from which reliable benchmarks can be drawn.

A key criterion for using the DCF approach is that a project has reasonably accurate and reliable forecast cash flows. Forecast cash flows for green hydrogen projects may be exposed to greater volatility, however, compared with other renewable energy projects. As the industry develops, there's an expectation that the cost to produce green hydrogen will fall – as was the case for solar and wind over the past decade. However, recent macroeconomic headwinds, such as rising inflation, higher power prices and cost of equity, and supply chain challenges in both the renewable energy sector and electrolyser production, have prevented costs from falling as quickly as predicted. Numerous forecasts predicting green hydrogen production costs at the end of this decade have been revised upwards as a result. For pre-FID green hydrogen projects, the potential for fluctuations in capital expenditure (CAPEX), production costs and offtake arrangements limits the predictability of cash flow forecasts.

The largest element involved in the cost of green hydrogen is the price of renewable electricity. This causes merchant risk, affecting both cost inputs and offtake, which requires mitigation. Subsidies and contractual arrangements therefore play an important role in ensuring that green hydrogen projects are profitable. Current volatility in the cost of green hydrogen can reduce the willingness of offtakers to commit to long-term contracts, especially if they're locked in at a high price. Without a long-term offtake agreement secured, a green hydrogen project is exposed to the merchant green hydrogen market. Even with a 10- or 15-year secured offtake agreement, the remaining useful life of a project is exposed to merchant risk, which is difficult to reliably forecast given the lack of established merchant markets for the sale of green hydrogen today.

A further issue is the lack of existing transport and distribution infrastructure. Hydrogen is particularly volatile to store and transport, and as such it is often stored in the form of derivatives, such as ammonia, before being converted back to hydrogen at the point of use.

As developers seek to find the most appropriate solutions for storing and transporting green hydrogen, this can result in fluctuations in cost as well as delays in securing reliable offtake, with offtakers being reluctant to commit to supply until a solution is found. We've observed clients in the industry attempting to navigate these challenges by developing interests throughout the green hydrogen supply chain from generation until the point of use.

Governments in Europe have begun to introduce green hydrogen subsidy regimes, giving projects the potential to progress to FID with security of offtake and thus allowing for fixed price contracts for the supply of renewable electricity to be negotiated. In the UK, the first iteration of the hydrogen allocation round (HAR1) closed in December 2023.

Subsidies such as these are essential to the development of the industry, enabling projects to proceed with certainty and progress beyond FID. Without subsidies or secured offtake agreements, there is a consensus today that green hydrogen projects will struggle to be profitable on a fully merchant basis.

Given green hydrogen's emergent state and the hurdles that still need to be overcome, the most common valuation approaches are those typically used for valuations of early-stage and venture capital companies. These include milestone analysis and the probability-weighted expected returns approach, which consider the unique nature of the businesses and the significant uncertainty associated with their future development

For green hydrogen projects which haven't yet reached FID or secured contractual arrangements for offtake, renewable electricity supply, storage, and distribution, typically we’d consider an early-stage valuations approach – given the lack of certainty regarding forecast cash flows.

Significant uncertainty remains regarding the speed and the scale of growth in green hydrogen. While it has the potential to make significant contributions to achieving net-zero targets, there's continued debate over the profitability of projects and whether the necessary infrastructure, expansion and innovation can occur to drive down costs.

However, there's evidence that governments across Europe are working to stimulate growth in the industry. The UK aims to award support to 875 MW of projects by the end of 2025 through HAR2, while the European Commission recently confirmed that EUR 720 million was allocated to around 1.5GW of projects in the European Hydrogen Bank’s pilot auction. Steps such as these can stimulate investment throughout the green hydrogen value chain and encourage offtakers to enter the market. Should a growing consensus emerge between governments and private capital regarding the necessity of green hydrogen to decarbonise hard-to-abate sectors, the industry could rapidly mature and solve some of the challenges outlined.

Ultimately, any approach to valuing a green hydrogen project should principally consider the underlying project-specific factors and risk of the cash flows. Securing long-term offtake through subsidies or PPAs, securing fixed renewable electricity prices, and managing distribution and storage arrangements will be key to enabling reliability and confidence in cash flows.

Until cash flows can become more reliably forecast, using early-stage company valuation techniques to triangulate valuation analyses will stay relevant. But as the industry establishes itself, we expect to find more meaningful analysis in the income and market approaches.

For further insight and guidance, get in touch with Tristan Rawcliffe, Jade Palmer or Adam Sutton.

![]()

Syndie shares how her career journey from audit and tax to Inclusion and Diversity helps her drive practical, evidence‑based inclusion across Grant Thornton.

Our annual report outlines how not-for-profit organisations can manage risks during ongoing uncertainty.

Decarbonising the UK’s energy system and wider economy will require rapid electrification of heat, transport and industry, leading to a sharp rise in electricity demand. The National Energy System Operator’s (NESO) analysis suggests electricity demand could increase by 25-40% by the early 2030s and almost triple by 2050, reaching up to 700-785 TWh per year, compared with around 290 TWh today