UK borrowers currently reporting under FRS 102 need to thoroughly prepare for the implementation of new changes to the Financial Reporting Standards, which come into effect for accounting periods beginning on or after 1 January 2026.

The Financial Reporting Council (FRC) published amendments to FRS 102 on 27 March 2024, with the intention of aligning it more closely to UK-adopted international financial reporting standards (IFRS). Most notably, these include important changes to both revenue recognition and lease accounting:

Section 23 Revenue

- There will be a new five-step revenue recognition model which could potentially alter how and when revenue is recognised

- Many companies, particularly those in technology, media and communications (TMT), construction, and professional services sectors, could recognise revenue and profits later under the new rules

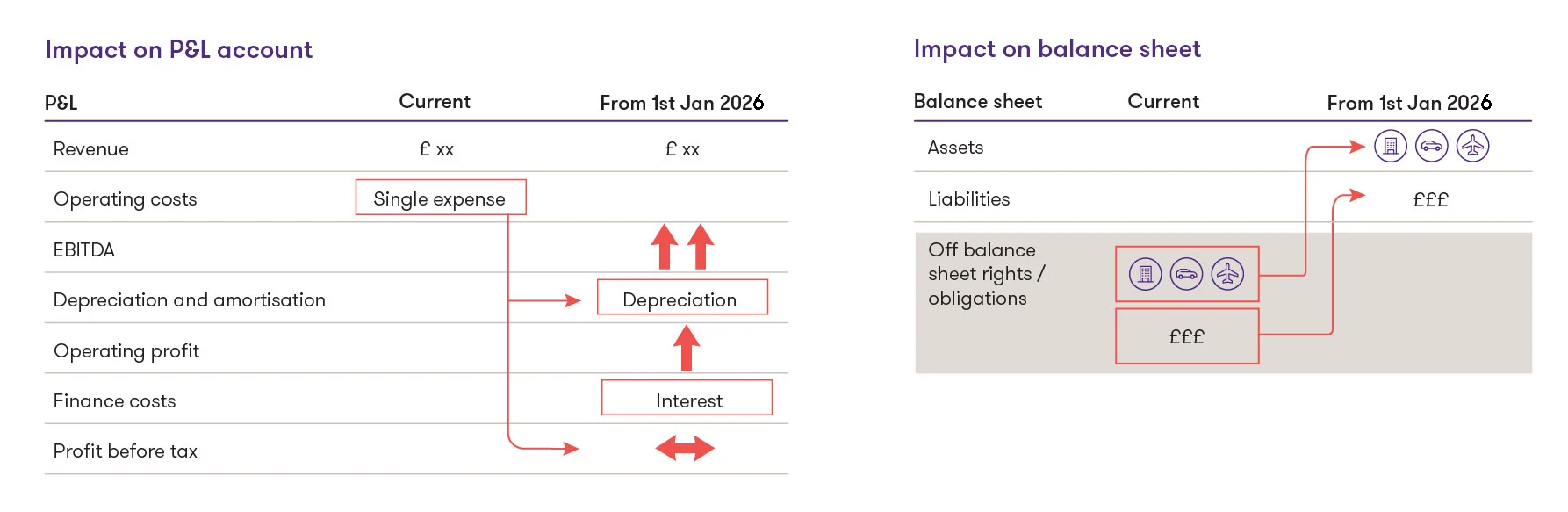

Section 20 Leases

- Leases will need to be capitalised and brought onto the balance sheet, recognising a right-of-use (ROU) asset and a corresponding lease liability. There are exceptions for short-term leases of 12 months or less and for leases of low-value items

- This accounting change will impact both the profit and loss and balance sheet - EBITDA and operating profit will increase and liabilities (and therefore leverage) will also increase

- The impact of these changes to lease accounting is illustrated below:

![]()

Technical details and further information about the FRS 102 amendments can be found here [ 4944 kb ].

Which businesses will see the greatest impact?

The amendments are relevant for companies reporting under FRS 102, and broadly reflect changes implemented by IFRS 15 and IFRS 16 back in 2018 and 2019 respectively. The new accounting guidelines are expected to affect 1.6 million reporting entities in the UK.

The changes required by Section 23 Revenue are expected to have greater impact on firms providing services or have long-term contracts, for example firms in the TMT sector, professional services and construction companies.

The changes required by Section 20 Leases are expected to have a greater impact on firms who lease large quantities of retail stores, offices, cars, aircraft, or other big-ticket items.

While some investors and stakeholders may have already adjusted, and mid-market listed companies already have to report under IFRS at a plc level, underlying group accounts and financial covenants may be entirely FRS 102-based.

Impact on financial ratios and covenant compliance

While these accounting changes don't change underlying cash flows, management need to be aware that the impact on financial reporting, the perception of indebtedness and covenant compliance could be substantial:

- Financial ratios and performance metrics will be impacted, including interest cover, EBITDA and operating profit

- Leverage may increase and capital ratios may decrease

- ‘Permitted baskets’ in restrictive covenants may also be breached due to the different treatment of operating leases

These changes may therefore affect a company’s ability to meet financial covenants and comply with existing loan documentation.

Some loan agreements may contain ‘frozen GAAP’ clauses, allowing borrowers to continue to calculate covenants for the duration of the loan under the accounting principles in place at the loan agreement date. However, while it might be possible to reverse out the new lease accounting rules which will apply from 1 January 2026, frozen GAAP which will be much more challenging for the revenue recognition changes required under Section 23.

How can companies approach their lenders?

Firms should seek to give existing lenders comfort that their underlying business is still the same, and that management is fully prepared for these accounting changes:

- Management should model how these changes will affect the profit and loss statement and balance sheet, seeking advice if necessary

- The complexity involved in changes to revenue recognition makes it even more critical that impacted firms produce detailed modelling, showing the impact on revenues – which will also impact EBITDA and operating profit

- Once the impact on key metrics such as EBITDA, operating profit and net debt has been ascertained, financial covenants and other key performance indicators can be recalculated considering FRS 102 changes

- Borrowers should speak to their lenders as soon as possible if they have covenants which may be affected by these accounting changes as financial and restrictive covenant levels may need to be amended

- As well as discussions with an existing lender base, these considerations will be relevant for borrowers seeking new financing as well

What are the wider implications for the business and other stakeholders?

Firms should also consider the impact of changes on other stakeholders such as equity investors, credit insurers, customer and employees.

- Where the timing of revenue recognition changes, there may be an impact on profit and therefore distributable reserves, affecting dividend payouts. Early communication with investors is key to maintaining financial stability

- FRS 102 accounting changes may also affect the valuation of a business in any M&A activity

- Will customer contracts need to be revised? The wording on contracts can have implications on revenue recognition under the new FRS 102 amendments

- Bonus / remuneration / share option schemes that are linked to financial performance could also be affected

- Consider the impact on taxable profits or losses so that lenders and other stakeholders are confident there won't be any unexpected tax liabilities arising from these changes

- Will internal KPIs remain relevant and useful, or do they need to be amended?

- There will be additional data collection and analysis required to implement these changes, and the cost of upgrading or implementing new systems and controls could be significant

- Management should understand the magnitude of this cost and communicate to relevant stakeholders

- Engage with your auditor in good time to address the risk that they disagree with expected impacts

How can you be prepared?

Companies should start preparing now to be ready for the implementation date of 1 January 2026. Taking the initiative to engage in early discussions with lenders and conducting thorough modelling of expected changes will ensure that you approach these conversations well prepared. This proactive approach will reassure lenders and stakeholders that business fundamentals remain intact, boost confidence in management and ultimately strengthen these key relationships.

Our experienced team can help with all aspects of accounting and advisory services. For more information or advice, contact Jon Bramwell, Pinkesh Patel or Richard Olney