UK utility investment trends

In collaboration with Inframation, we looked at two main factors of infrastructure investment trends in the sector.

Average share premiums

The first factor we considered was UK listed utilities companies’ average share prices relative to their average book values per share. We did this to identify a proxy for the premium an investor is willing to pay over and above its reported NAV per share.

Private sector deal data

After that, we analysed private sector deal data as provided by Inframation to ascertain whether the (more accessible) listed market sentiment is mirrored in the private sector, and to understand the investment trends inferred by it. The periodicity of reporting means that there are limitations to this approach, so our inferred premium to NAV should only be used as an informal guide.

Getting defensive

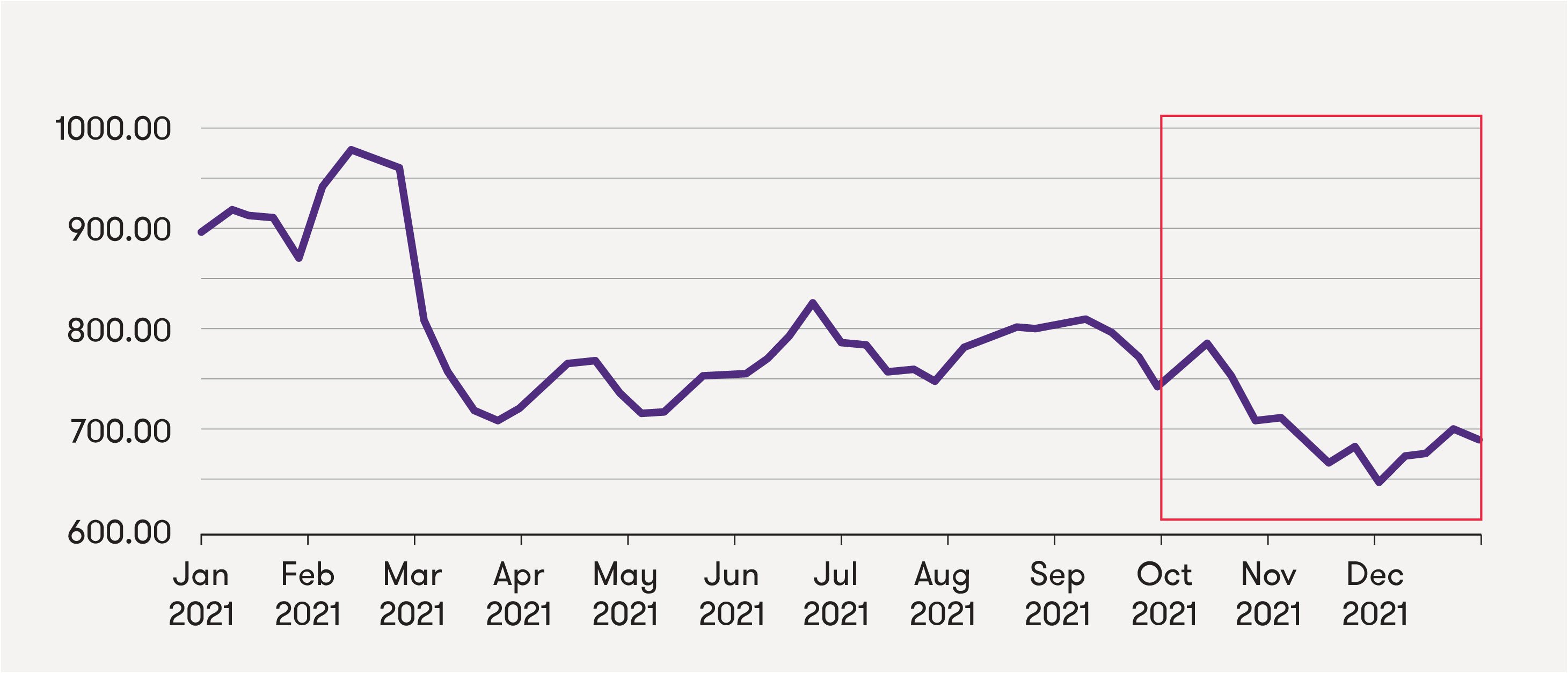

Given recent market volatility, it is expected that investors will look to readjust portfolios towards defensive stocks. Since the arrival of Covid-19, the listed UK utility sector has remained relatively unscathed with premiums to NAV largely stable. At the end of 2021, we saw stock markets globally fall with the London Stock Exchange (LSE) dropping around 7% in price from 7,450 on 30 September 2021 to 6,930 on 31 December 2021 reaching a low of 6,502 mid-way on 30 November 2021.

UK utilities: premium to NAV

LSE Group share price

While premiums have stayed relatively flat for unregulated utility stocks, the premiums ticked upwards for regulated utilities from the start of November to December 2021 over the same period where the LSE was in decline.

Utilities provide essential services to society and are associated with low income elasticity which means they transcend economic cycles of bust and boom. While the returns are typically regulated, these are at a level which allows for the regulated asset to earn an adequate and reasonable return and thus they're considered comparatively more attractive than unregulated utilities. When looking at the above, we note that regulated utilities attract a significantly higher premium than diversified utilities like Centrica and SSE, with regulated asset premiums to NAV rising to over 240% by the end of 2021 versus unregulated asset premiums to NAV sitting at around 50%. Utilities are particularly attractive to investors like pension funds which liability-match their portfolios with long-dated investments.

A sharp rise in premiums for regulated assets in July 2021 followed the release of half-year results which showed reduced book values, particularly for Pennon Group plc (Pennon), which paid out a sizeable dividend of 355p in mid-July, while share values held steady or gradually improved (with the exception of Pennon’s ex-dividend shares). This evidences the notion that whilst investors were anticipating a fall in book value post COVID-19, they remain confident that regulated businesses would be resilient in the long-term.

According to Inframation's data platform, Infralogic, 2021 saw a bumper year for private sector deals in water, waste, and electricity distribution, with nine UK deals closing - the largest number of deals closed in a year since 2018. This is in conjunction with a record reported deal value of c. £12 billion, exceeding the last five years combined.

Closed transactions by year

While the largest reported deal by value relates to the agreed sale of Western Power Distribution to National Grid for £7.8 billion in June 2021 (which is expected to close in early 2022), the water sector dominated 2021 deal volume with four out of nine transactions closing in the year - the most recent being the sale of an 8.77% stake in Thames Water to USS from Wren House Infrastructure in December 2021.

Water way to start the year

The UK listed stock utility universe is dominated by regulated water utilities. The Regulator, Ofwat, issues a Price Review (PR) every five years setting out the price, investment and service package that customers received. The next PR is planned for 2024 (PR24) which will determine the wholesale price controls for water and sewerage companies from 2025 to 2030. The draft methodology is expected in July 2022 and anticipated to be finalised between Q4 2022 and Q1 2023, which will set out Ofwat’s views on the allowable weighted average cost of capital (WACC) returns for regulated utilities.

The most recent PR24 documentation issued in May 2021, outlined initial views intending to streamline the price review process without compromising sophistication. Three key concerns are expected to be addressed are:

1 Climate change

Predicted net reductions in annual rainfall and increasing probability of drought.

2 Customers’ interests and expectations

Growing concerns surrounding Environmental, Social and Governance (ESG) disclosure and a consumer desire for enhanced service.

3 Affordability

Household financial struggles amplified by Covid-19 and inflation, while Ofwat’s scope for bill reductions is reduced due to falling costs compared to PR14 and PR19.

Overall, the consultation aims to improve clarity and transparency across PR24 with Ofwat considering publishing models, controls and incentive plans ahead of business plan submissions.

Additionally, we understand that there is an intention to review the risk allocation framework to maintain or improve companies’ assets health resilience whilst not compromising on cost of capital. This will be important to maintain confidence in the sector and may be a contributing factor to the significant premiums regulated companies exhibit versus unregulated companies we’ve observed in the graph above.

2021 saw a number of notable deals in the UK water utility sector with USS most recently acquiring an 8.77% stake in Thames Water from Wren House increasing its total stake to around 20% in December 2021. This follows a number of pension funds eyeing up opportunities in the sector with Inframation reporting that Ontario Teacher’s Pension Plan (OTPP) appointed Evercore to help assess deals in the space.

According to Inframation “the potential move into UK water comes after investors were given greater clarity on the sector in March 2021 when four water companies successfully appealed against Ofwat’s plans to sharply reduce their returns from 2020 to 2025. The Competition and Markets Authority (CMA) ruled that Anglian Water, Bristol Water, Northumbrian Water and Yorkshire Water should receive slightly higher returns than expected over the period."

This ruling has had an observable impact on valuations in the sector with Pennon Group acquiring Bristol Water Group (Bristol) from iCON Infrastructure and Itochu Corporation for £425 million implying a total enterprise value of £814 million. This deal represented a 44% premium to Bristol’s regulatory capital value (RCV). The implied EV/EBITDA multiple for this deal in 2021 was 17.2x up from 9.8x reported in 2016 when iCON Infrastructure acquired a 30% stake in Bristol from Suez, according to Inframation.

Inframation also notes “the takeover will increase Pennon’s own RCV by 16%, adding to its core subsidiary South West Water, which has an RCV of GBP 3.4bn and supplies 2.3 million people in Devon and Cornwall and parts of Dorset and Somerset."

We can see from the graph below that this has likely contributed to the significant spike in Pennon’s premium-NAV in June 2021. Whilst this premium-NAV spike has somewhat reverted it has remained stable since its September 2021 results were issued at c.150% up from c.50% at the start of 2021.

Water: premium to NAV

Outlook for UK regulated water companies

With significant economic uncertainty, we expect to see further spotlight on the regulated utility sector in the UK as investors look for stability. However, we consider there to be three notable trends to watch out for that could change the current market sentiment:

Inflation

Inflation is a key driver of growth in RCV and the amounts billed by UK water companies to their consumers. UK regulated water companies are relatively resilient to increases in inflation due to the underlying nature of their regulation. The regulatory return is determined on real terms along with the RCV, operational expenditure and capital expenditure, which are indexed annually and therefore increases in inflation allow for revenue increases that reflect increases in costs. Outturn variations can be corrected for in future regulatory periods.

RCV indexation and cost of capital estimate currently use a combination of RPI and CPIH, with a more comprehensive switch to CPIH-based RCV indexation considered in the next (PR24) price control period. CPIH inflation has risen sharply since the most recent regulatory decisions, and is expected to remain elevated over, although returning towards long-term levels average levels in the medium term.

CPIH (YOY%)

Diversification

Under the Direct Procurement for Customers (DPC), Ofwat permits water companies to competitively tender services in relation to the delivery of certain large infrastructure projects with the aim of enhancing benefits for customers. Under this arrangement, we’ve observed several water companies; Anglian Water, United Utilities and Welsh Water, diversifying their holdings by procuring renewable energy corporate power purchase agreements (PPAs) to provide direct power to their project sites.

While the DPC does provide a procurement framework, water companies are not bound to it. Yorkshire Water, for example, estimate that its proposed anaerobic digestion plants could generate additional revenues for the company and is tendering for the design, build, finance, operation and maintenance of the plants under a 15-year agreement.

Diversification like this could provide additional returns to investors while also providing attractive counterparty PPAs to the market. Investments into generation assets like these by water companies provides a way for the utilities to manage costs and volatility in the current market while accelerating decarbonisation and providing potential upside to consumers.

Debt structuring

Given the high levels of leverage utility companies have historically taken on, its unsurprising that it’s been a cause for concern in our current rising interest rate environment. It’s been recently reported by Inframation that S&P Global could lower its ratings on some of Thames Water’s junior debt to junk status if they do not “take strong remedial measures” to improve its leverage position in the short term – with leverage of over 82% it’s considered the most leveraged water company in the UK.

We expect that more utility companies will follow the likes of Southern Water and Anglian Water to issue new debt outside of their regulatory ringfence, in turn reducing their debt at operating level. Through introducing new financial structures Anglian has managed to reduce its ratio of net debt to RCV from c. 82% to below 70% by separating its regulated and unregulated operations. When considering that Ofwat has historically indicated that it will require water companies with high gearing to share the benefits of any increased equity returns with customers (resulting from increased leverage), we expect this kind of financial structuring to come under scrutiny as interest rates rise.

For more information and guidance on utilities valuations, get in touch with Jade Palmer.