Technology insights Q4 2021

Do you have the skills and resources you need to keep moving forward? The technology sector is starting 2022 with strong momentum, but talent attraction, development and retention are going to be key challenges for 2022.

Q4 2021 topped a strong year of M&A for the TMT sector: lofty valuations and record amounts of liquidity across private equity, debt and public equity markets are also fuelling predictions that the sector will be at the forefront of any post-COVID economic bounce. But, it's apparent that the widening digital skills gap is a potential threat to businesses capacity to capitalise fully on the market opportunities.

In our final edition of 2021 technology insights our experts share their insight on Q4 and what to expect in the first few months of this year.

A busy Q4 meant that there were 1,106 deals (an increase of 37% on 2020) in our sectors of interest, beating 2019 pre-pandemic volumes of 1,002.

Tech M&A heads into 2022 with similar momentum, powered by strong valuations and record amounts of liquidity across private equity, debt and public equity markets. There is also an expectation of a continued technology and digital-led economic bounce post-COVID-19 which supports earnings growth expectations.

The pandemic has forced companies to hone their strategies. Coupled with the expansion in valuation multiples for recurring revenue technology stocks, this will bring more deals to the table this year.

All deal activity outline below is based on the announced date of the deal and includes deals with a UK target or deals with a UK domiciled acquirer. Deal activity excludes growth capital transactions.

M&A in Q4 2021: an overview

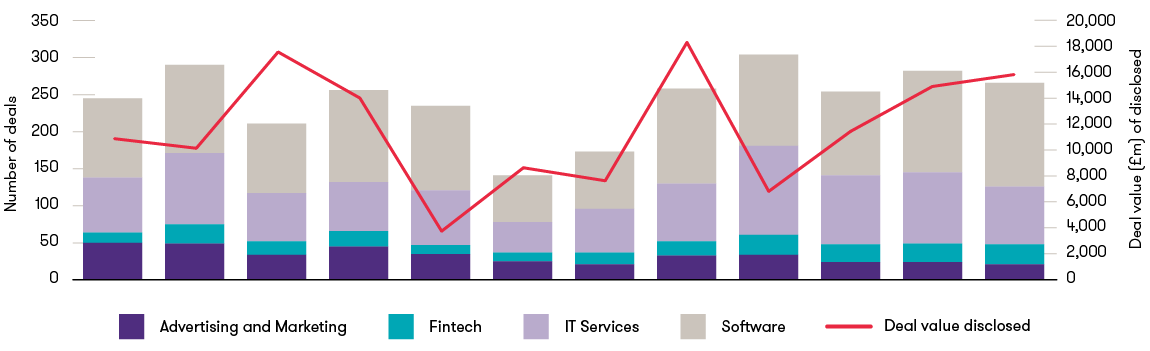

Graph 1: Deal value and volume per technology sub-sector

Deal volumes

The strong appetite for technology deals throughout 2021 continued into Q4. Some 266 deals were announced, a slightly lower figure than for Q3 (282) but marginally up on the same quarter last year (258).

Software deals continued to dominate, accounting for 52% (140) of Q4 transactions, followed by IT services (78), fintech (27) and advertising (21).

Reported deal values

Deal values that were announced during Q4 totalled £15.9 billion compared with £15.0 billion in Q3 and £18.0 billion in the same quarter last year. In 2021 overall, deal value totalled £49 billion, up 28% on pandemic-impacted 2020 levels.

Big ticket deals included two take-privates. The first was Permira’s c.£4.4 billion acquisition of NASDAQ-listed internet security firm Mimecast, reflecting the growing importance of cyber security as the business world adapts to hybrid home-working models.

The second was SS&C Technologies outbidding of private equity with a £1.2 billion recommended offer for AIM-listed British robotic process automation software vendor Blue Prism. This reflects the market opportunity in automation of manual back-office processes in key markets like financial services and healthcare.

These deal values are mainly sourced from corporate websites. However, if no press release is available they are sourced from deal databases including Capital IQ, Megabuyte and Mergermarket, or from press commentary released at the time of the deal, deal values may subsequently be amended as further detail is released by the acquirer.

Notable deals

Private equity’s march continues

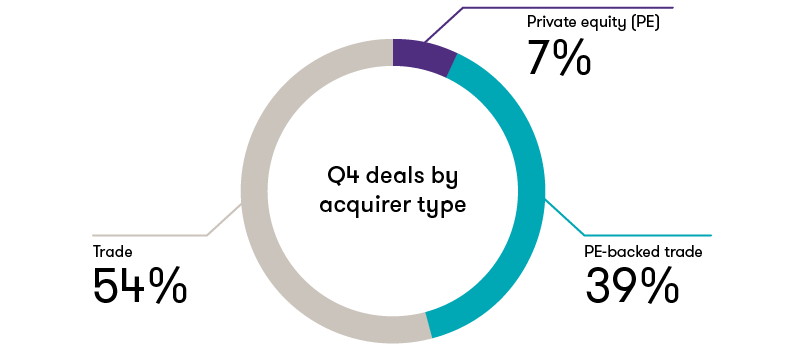

Graph 2: Q4 deals by acquirer type

Private equity continued to flex its muscles in Q4, responsible for 46% of transactions. Powered by record amounts of dry powder, it is outbidding trade buyers and driving up valuations, a theme we discussed in more detail in our autumn 2021 update.

Last year was also the year of the SPAC (special purpose acquisition companies), at least in the US. Recent relaxations in UK listing rules make this a more feasible route now in the UK, however it is unlikely that we will see a rush of so-called ‘blank cheque companies’ to the London market in 2022.

More relevant to UK technology companies will be how SPACs already on the market look to deploy their significant capital within the specified time limits they have to invest (typically up to two years). How many UK players will follow Cazoo, for example, which raised $1 billion in August via a SPAC to continue its push to transform the car-buying experience in the UK and internationally?

Capital markets view

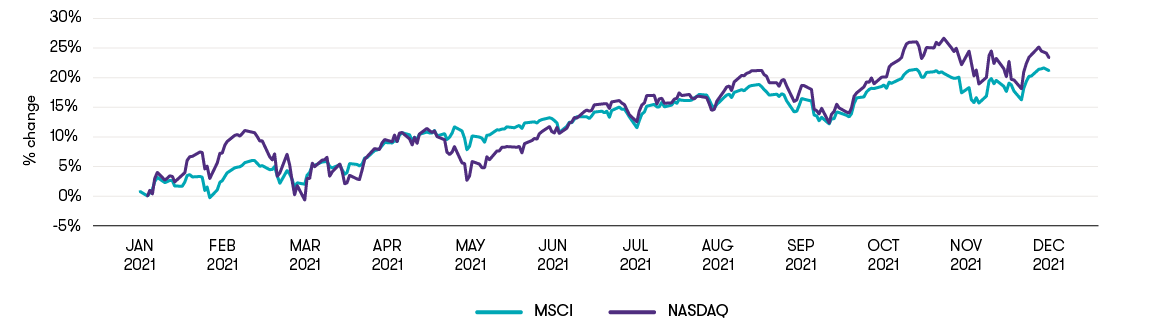

Listed businesses enable us to keep a finger on the pulse of tech sentiment. In Q4, the tech-focused Nasdaq and the more broadly focused MSCI followed a similar pattern, up 21% and 23% respectively.

Graph 3: Equity market indices

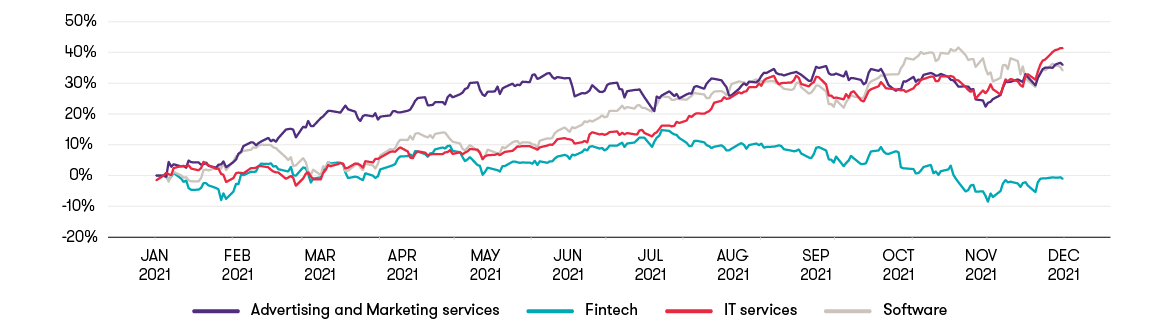

In terms of comparative peer group performance, advertising and marketing services, IT services and software outperformed fintech, which was very much the laggard in Q4. This divergence reflects both the relatively rapid rise of these sectors and the chequered experience of the consumer-exposed B2C payment providers that fall within fintech. It also reflects more challenging market sentiment for the sector as the Omicron variant hit.

Graph 4: 2021 peer group performance

Three trends to watch in 2022

1 Will IPOs mount a more significant challenge to PE for growth technology stocks?

Last year saw a flurry of tech IPOs on the London stock market, bolstered by the successful float of UK artificial intelligence firm Darktrace in April. A number of computer games companies also looked to London to raise capital.

There are two key questions: will more large technology companies return to the listed market in 2022, or continue to cycle through different private equity ownership structures at ever-increasing valuations?

Secondly, can the main London market more consistently attract European technology companies that are lured to the US market by the perception of higher valuation potential and greater depth of coverage?

2 A rise in infrastructure deals

As demand for tech increases, the supporting digital infrastructure must keep pace. Infrastructure funds are moving aggressively into the sector. As well as seeing significant investments from established infrastructure funds into areas such as data centres and fibre roll out, 2021 also saw the creation of investment companies specialising in digital infrastructure. One example is Digital 9, which raised a reported £300 million in a March IPO.

3 Health and wellbeing

Vertical market software is a hot area for M&A and PE activity. While there was a huge amount of activity in edtech in 2021, this year we predict health and wellbeing tech will be a key vertical.

This is not just a consequence of the pandemic but an ongoing need for modernisation of healthcare services, particularly the NHS. In February 2021, CVC Capital Partners acquired patient records specialist System C Healthcare. Over in the US, Oracle acquired healthcare software specialist Cerner in Q4. In an increasingly health-focused world, we also expect to see more investment in consumer health apps and devices.

For further insight on TMT sector trends in M&A, get in touch with Andy Morgan.

In the UK there are currently estimated to be 178,000 to 234,000 open vacancies in data science. Research conducted by Burning Glass in the United States and Australia has found a similar trend in these countries, suggesting the shortfall in data specialists is global.

According to popular job site Reed, the number of unfilled vacancies for the IT & telecoms sector is higher than any other sector at over 25,000 – that is more unfilled vacancies than even social care or transport and logistics.

There’s an urgent need to intensify efforts to boost the number of data-skilled workers through greater collaboration between government, industry, and academia. True transformation involves developing specialist data skills, as well as improving confidence and familiarity with data throughout each level of your organisation. As UK Government’s 2021 research notes, not every worker needs to become a data scientist, but everyone will need a basic level of data literacy to operate and thrive in increasingly ‘data-rich’ environments.

What type of specialist roles and skills are organisations recruiting?

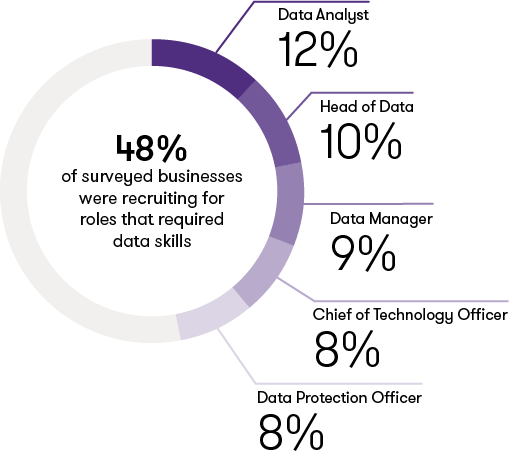

According to the government research, 48% of the businesses surveyed were recruiting for roles that required data skills. The most common type of data role sought by businesses was data analyst, with 12% of businesses recruiting for this role.

After this, the most common roles being sought were fairly senior positions: one in ten (10%) were recruiting for a head of data position, with similar proportions recruiting for a data manager (9%), a chief technology officer (8%) and a data protection officer (8%). Highlighting the importance of creating entry-level roles can free up management capacity, with alignment to management development and career pathways to further support business growth.

For high-growth technology businesses, or those struggling to recruit and retain talent more generally, demand for these vacancies is only amplified.

We recently teamed up with BPP to understand the skills organisations are looking for in junior technical roles to make the most out of their data; identifying three development drivers:

1 Technical (hard) data skills

Working with complex data architectures: including programming for data analytics, big data architectures, and big data analytics in addition to AI, machine learning and robotic process automation.

2 Generalist (softer) skills for business awareness and professionalism

Understanding the types of decisions and problems that data can help solve – a strong commercial mindset and collaboration skills to gather meaningful data and transform this into insight that drives change. Data ‘storytellers’ can use critical thinking and communication skills to present findings through stories.

3 Data literacy and confidence using data

The final key development driver is general confidence in handling data. The overflow of data spills into all our experiences, in work and out. The major shift that is taking place right now is not just an ad hoc investment to develop subject matter expertise, but an uplift across organisations and society to build fundamental data skills so that people are empowered within their own job.

Where can TMT get the data skills it needs?

To access talent with degree-level data skills, businesses in the TMT sector should consider the advantages of junior roles at level 3, 5 and 6 with degree apprenticeships. Learners attain enhanced education with professional and part-time undergraduate studies while working and contributing to your organisation.

These programmes can be fully funded by the apprenticeship levy. Employers can also receive further financial incentives of up to £6,000 for hiring 16–24-year-old employees and use apprenticeship programmes to upskill existing employees or retrain within the organisation.

Data is born in the business and therefore everyone can get real value by using the data and tools they have available to them, in a way that saves you time and creates better decisions.

For more insight and practical guidance on leveraging degree apprenticeships to benefit your organisation, get in touch with our talent solutions team.

![]()