Technology insights autumn 2021 and M&A outlook in 2022

18 Oct 2021Q3 2021 M&A: an overview

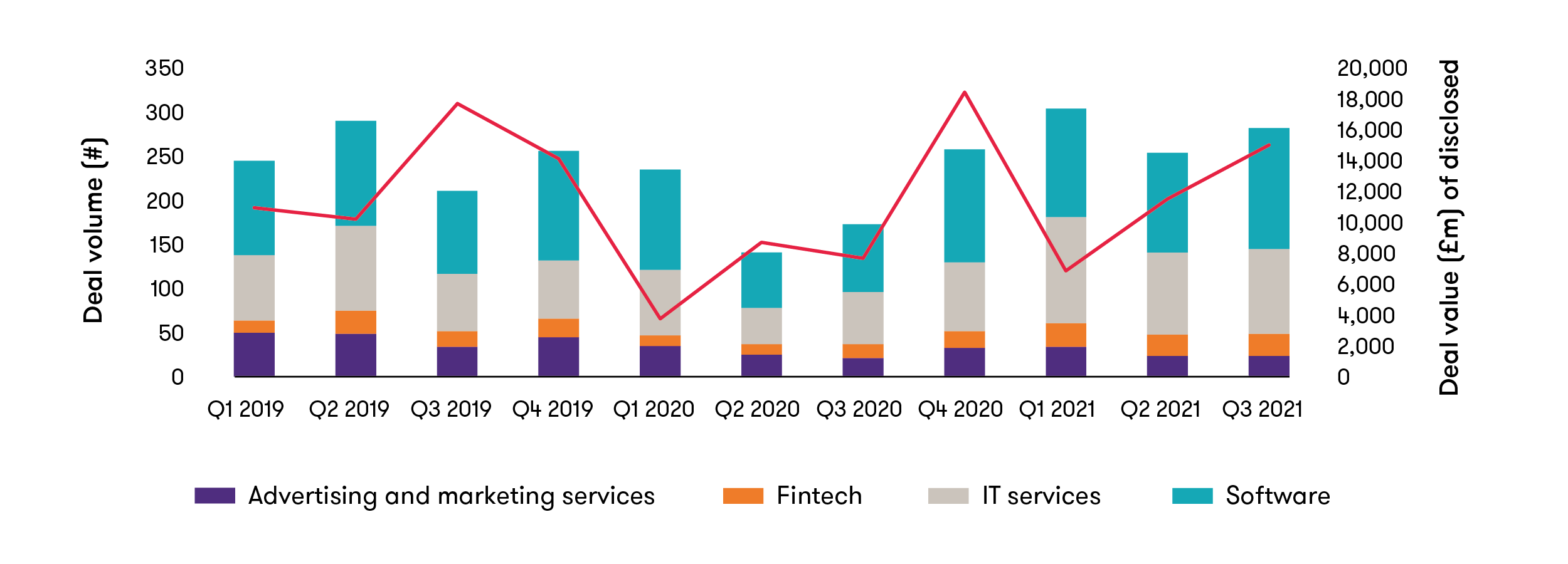

There were 282 announced1 transactions in Q3 2021, an increase of 11% from Q2 2021 and a (pandemic-affected) increase of 63% from Q2 2020. While Q1 2021 had a higher volume of deals, the very strong demand for technology acquisitions means that volume in Q3 was largely driven by brand new processes, rather than ‘catch up’ deals, ie, those just delayed due to the pandemic.

Software made up the majority of deals (137 transactions), followed by IT services (96 deals), fintech (25 deals) and advertising/marketing services (24 deals). Disclosed deal value reached just over £15 billion, largely driven by a handful of very large transactions – the highest figure since Q4 20202.(2) There were 20 deals in Q3 with an enterprise value larger than £100 million.

Graph 1: UK TMT M&A by sub-sector. Source: Mergermarket, Megabuyte, Grant Thornton Research, Capital IQ

Notable ‘mega deals’ in Q3

Vista Equity Partners agreed a take private offer for Blue Prism for an implied enterprise value of about £1 billion (or 6.4x last 12 months revenue / 5.4x forward revenue). Vista plans to combine Blue Prism with one of its existing businesses Tibco, providing significant cross-sell opportunities.

GTT completed the carve-out and sale of its predominantly European data centre and sub-sea cable assets to I Squared Capital. The transaction valued the new business (UK-based Exa Infrastructure) at about £1.5 billion.

US-listed NortonLifeLock agreed a take private offer for peer Avast, at an implied enterprise value of £5.5 billion (or about 8.2x trailing / 8.0x forward revenue). Avast is known for its freemium distribution of consumer antivirus product AVG. The new combined entity is expected to leverage its significant economies of scale to drive efficiencies in R&D and customer acquisition.

Looking at deals with an enterprise value (EV) larger than £100 million (with disclosed deal information) in Q3, eight were standalone private equity (PE) investments or platform PE deals. The influence of PE can especially be seen across the mid-market. In Q3, there were 35 direct PE transactions but 119 transactions involving PE-backed ‘platform’ businesses. These typically focus on a higher volume of smaller transactions to consolidate a marketplace, driving economies of scale to create greater combined value ahead of an exit.

The most active acquirers in the last quarter were: Access Group (an Hg/TA-backed enterprise software provider) with six deals; Livingbridge completing three direct investments (North, Venatus, RealVNC); Sophos (a Thomas Bravo-backed provider of endpoint security) with three deals; and Paysafe (a Nasdaq-listed but London-based payment processor) with three deals.

Graph 2: Q3 Deals by acquirer type. Source: Mergermarket, Megabuyte, Grant Thornton Research, Capital IQ.

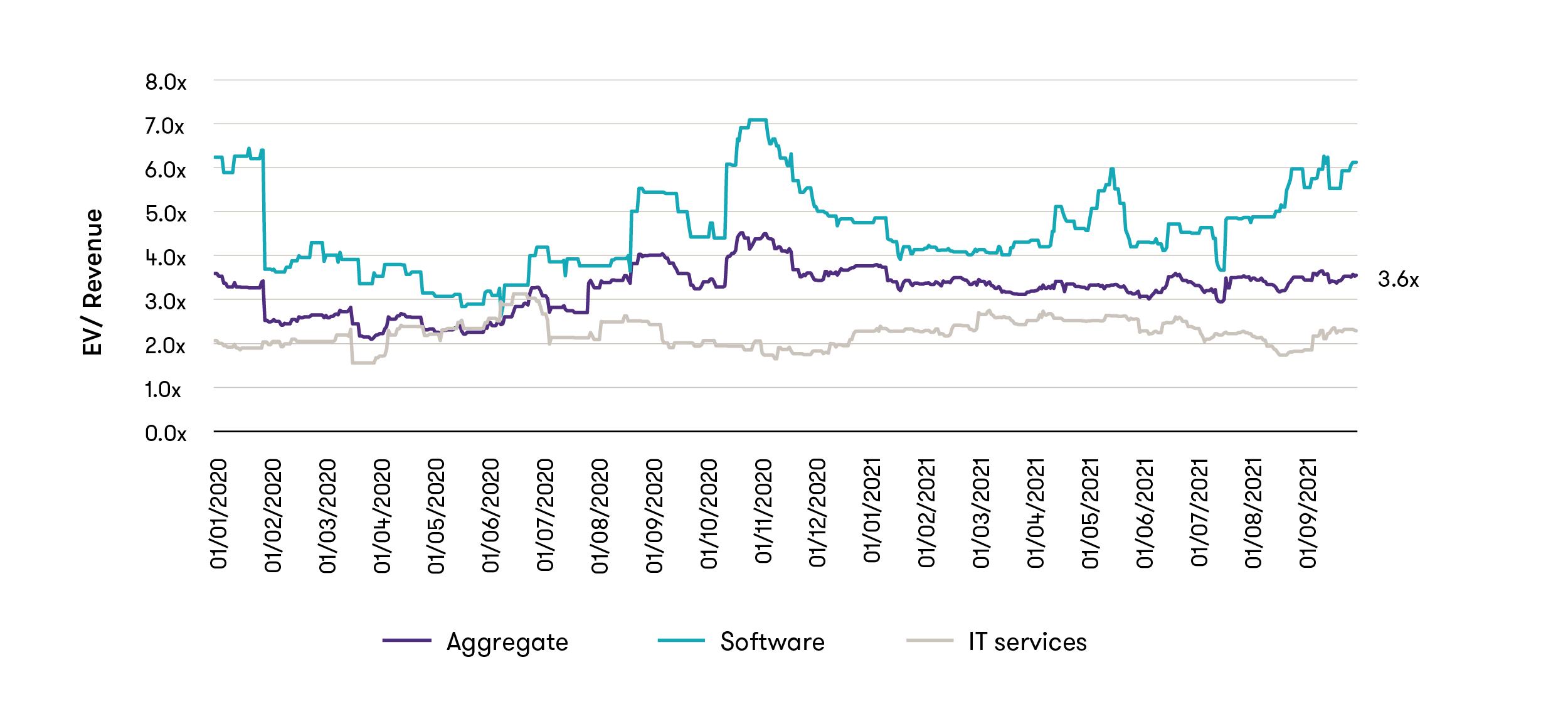

Looking at valuation, the mean enterprise value-to-revenue (EV/revenue) for our four key sectors in aggregate was 3.6x revenue in Q3 (up from 3.3x in Q2). Although this metric is variable quarter-to-quarter (as it depends on the timing of individual deals), we think this is representative of what’s happening in the M&A market: pricing expectations have sharply increased due to significant competition for deals, especially the highest quality opportunities. For example, looking purely at software deals – a sector characterised by high growth, recurring revenue and deep entanglement with customers – the rolling average reached 6.1x revenue.

While takeover activity on the public markets has continued apace, capital markets remain firmly open for business. Despite more recent weakening driven by macro concerns around inflation and supply chain challenges, the tech-heavy Nasdaq remains up 12.2% in the year and finished Q3 roughly where it started Q2.

Graph 3: TMT 90 days rolling average EV/revenue since Q1 2020.3 Source: Mergermarket, Megabuyte, Grant Thornton Research, Capital IQ.

Three trends affecting TMT M&A

Looking into Q4 and beyond we expect the TMT M&A market will be shaped by these three factors.

1 Elevated activity likely to continue

Q3 2021 was clearly an interesting quarter from a deals perspective, being characterised by a very high volume of transactions, intense competitive tension and higher valuations. The high levels of liquidity across all sources of capital means it is hard to see this easing off any time soon.

2 Rise of ESG

While environmental, social, and governance (ESG) has received significant attention in capital markets, it is still at a relatively nascent stage in its impact on the M&A market. There have been more financial sponsors this year with an ESG/impact specific focus and we expect to see more funds become active in this area. There has also been more ESG-related disclosure. Such disclosure can have a real impact on a deal: for example, some debt providers offer better pricing for ESG-related transactions.

These trends are likely to persist given wider societal concern about social justice and the climate. As a firm, we have advised on several ESG-related deals in recent weeks including Bambino Mio, Skills Training UK and Nkuku.

3 Greater non-core disposal activity

A strong valuation environment and high levels of private equity uncommitted capital (also known as ‘dry powder’) have reignited corporate interest in non-core disposals. We expect this to be sustained as boards look to maximise the value of their assets, and focus their capital resources on areas central to their post-COVID-19 strategy.

For further insight on TMT sector trends in M&A, get in touch with Andy Morgan.

Footnotes

1 All deal activity is based on announced date of the deal and includes deals with a UK target or deals with a UK domiciled acquirer. Deal activity excludes growth capital transactions.

2 Deal values are mainly sourced from corporate websites, however, if no press release is available they are sourced from deal databases including Capital IQ, Megabuyte and Mergermarket, or from press commentary released at the time of the deal. Deal values may subsequently be amended as further detail is released by the acquirer.

3 Figure shows the preceding 90 day rolling average EV/revenue, for transactions with deal information in the public domain; individual time series for fintech and advertising and marketing services not shown due to lower volume of transactions.