Businesses adapting to changes in consumer behaviour

15 Mar 2021From social distancing to full lockdown, retailers and other consumer markets businesses had to constantly adapt to the changing circumstances of the last 12 months. Kevin Coates explains how we've helped our clients explore and embrace new options.

In some cases, the COVID-19 lockdown has accelerated retail and consumer trends that we were already seeing in the market. Online shopping and exercising at home, for example. These new trends have pushed businesses with challenged business models and financing structures into financial distress.

On the other hand, an end to international leisure travel was completely unexpected and left many travel firms reconsidering their strategies.

The companies that have navigated through lockdown and are likely to succeed in the post-lockdown new normal are the ones that adapted rapidly and decisively, to take advantage of how consumers have adapted their behaviour. Look below for how we supported our clients through the uncertainty of 2020.

Our highlights in consumer markets

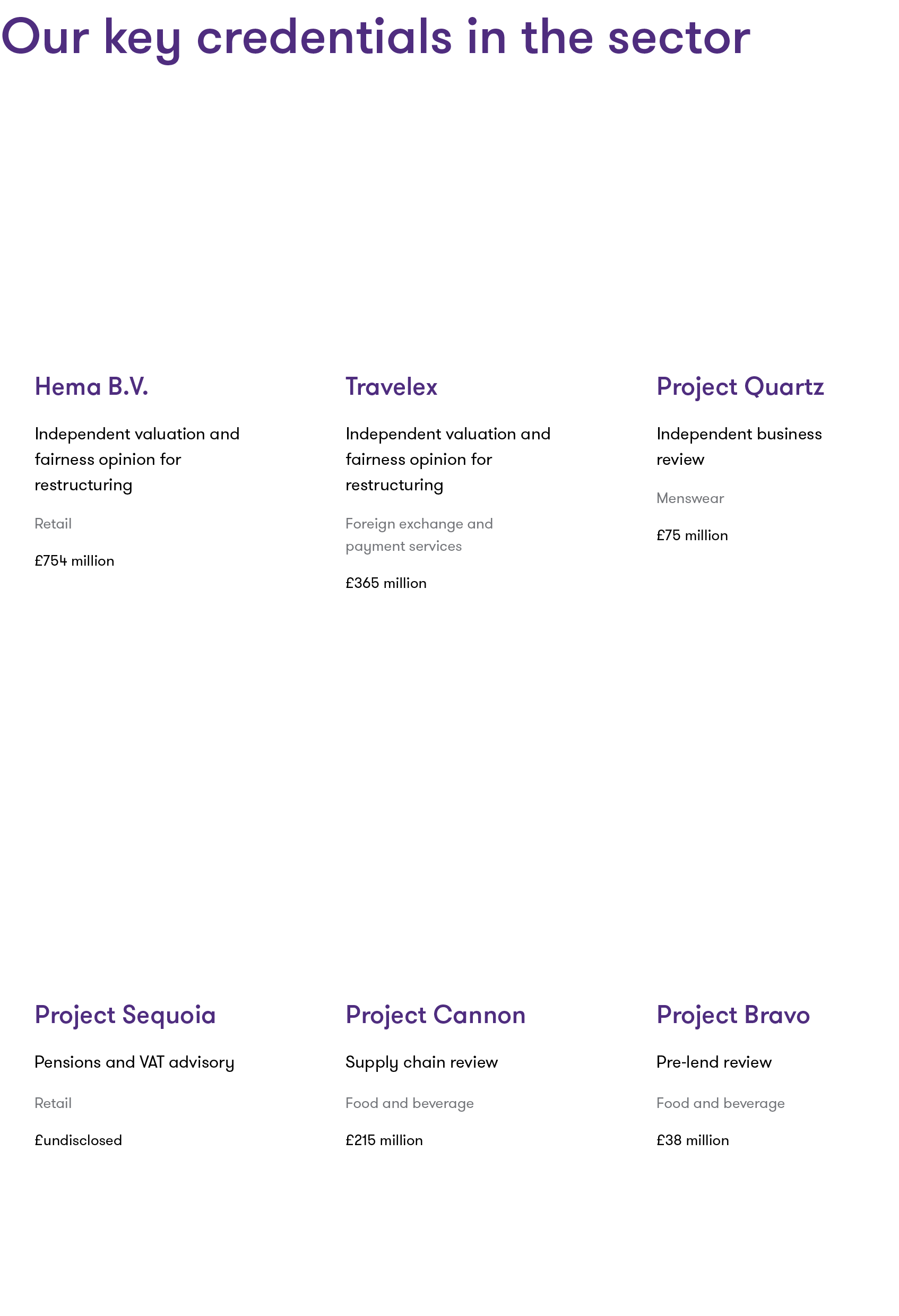

Discover our key credentials in the sector

The state of the consumer markets sector

During 2020, we've seen changes in consumer behaviours in:

- how they interact - video conferencing

- leisure activities - outdoor exercise

- holidays - 'staycations'

- how they work - remote working

- how they shop - online retail

- how they eat - takeaway.

Once the world returns to normality, businesses will still have to adjust to these changes, and do so rapidly. For many consumer-facing companies, the impact of these changes will be immediate and potentially permanent.

Rapid changes in consumer behaviour necessitate rapid changes in your business model. Thankfully, the options available for restructuring businesses are broader than ever, from Company Voluntary Arrangements (CVAs) and Restructuring Plans to ‘light touch’ administrations, which are more likely to be accepted by stakeholders and be successful, if well thought through and managed.

We're supporting businesses in identifying and implementing the most-appropriate solvent restructuring or insolvency option to enable the business model transition and maximise stakeholder outcomes.

Retail sector

Despite gloomy headlines, total retail sales grew very slightly in 2020, by around 0.2% on 2019. While this is well below the long-term growth trend of the past decade, it is better than many would have expected.

A key component in this was the rise in online sales: from a base of around 20% penetration of all retail sales before the March 2020 lockdown, online sales penetration rose to around 30% by December 2020. This is an acceleration of a decade-long channel shift from physical to online shopping, some of which will be permanent, even once we're all vaccinated and safely visiting shops.

The biggest beneficiaries in terms of this sales transfer have actually been traditional retailers. Successful multi-channel businesses like Next have shown that a mix of well-located stores, complemented by a seamless online proposition, is a resilient and profitable model.

Next, however, has had four decades to hone its business model, a strong balance sheet, and the benefit of far-sighted senior management to implement the plans and investments required to achieve its current success. The relative success of some traditional retailers doesn’t mean that consumers will rediscover a love for shopping in drab, poorly executed stores after lockdown.

The demise of groups such as Arcadia has as much to do with a lack of development of core brands such as Evans and Wallis (in their day two of the most successful retailers in their sectors) as it does to the ongoing march of ecommerce.

Evidence that these brands retain some value is shown by the recent sale of the Debenhams brand and online business to BooHoo, and the Evans brand to City Chic, which we advised on.

However, many retailers are still confronted by operating models and capital structures that are not relevant to a post-coronavirus world:

- Too much space in the wrong condition and the wrong places

- A cost base that is misaligned with sales

- Insufficient funding for the investments needed to make their businesses fit for the future

Hospitality, leisure and travel

Leisure and hospitality suffered badly during 2020, particularly the travel industry. Our recent travel barometer survey shows that demand in sectors like cruises may remain subdued, while outdoors activities or experiential holidays might see a sharp rise in demand.

Many in the travel sector are expecting a slow return to flying, with international tourism not expected to recover back to 2019 levels until 2024.

Many businesses in the hospitality and leisure sector have sought to re-imagine their physical unit space, or diversify their offering to take-aways. However, even those actions have been hindered by the different restrictions during lockdown.

Pent-up consumer demand for these sectors holds promise for a spending-led recovery when restrictions are lifted. However, a viable future will require business models to have adapted to consumer behaviour changes and financing structures to be sustainable.

Case study

IBR and FA role in relation to UK travel agency group

![]() On behalf of the Revolving Credit Facility (RCF) and unitranche lenders, we undertook an independent business review and advised the lenders in relation to a private equity-owned travel group.

On behalf of the Revolving Credit Facility (RCF) and unitranche lenders, we undertook an independent business review and advised the lenders in relation to a private equity-owned travel group.

Due to lockdown, the group suffered a severe shortfall in booking and revenue, leading to a liquidity crisis. The group presented lenders with an urgent proposal for a new money funding, rescheduling of existing debt repayments and adjustments to cash pay interest servicing.

We reviewed the group’s short-term cash flow forecast, medium-term business recovery plan and financial forecasts, as well as assessing the options for the lenders.

Our review of the business plan and forecasts included consideration of revenue and booking recovery, refunding of customers for bookings disrupted by coronavirus cancellations and postponements, as well as the group’s cost savings and liquidity enhancement initiatives.

In addition, we performed sensitivity analysis against the various scenarios for revenue recovery trajectories and the deliverability of management’s self-help measures.

Our advice and support for the lenders enabled them to consider credit implications of the group’s proposal appropriately and provide support for the group through the disruption to trading.

How we help our clients

We have been advising management teams on how to identify and implement the most-appropriate solvent restructuring or insolvency option to enable the business model transition and maximise stakeholder outcomes.

Your data is your biggest resource and we offer a practical, supportive and personalised approach to analysing and interpreting it. We combine your information with consumer and market analytics to deliver powerful insights to help you manage risk, reduce costs and identify investment opportunities to strengthen revenue and enhance value.

![]()