Business support services sector diverges

15 Mar 2021In the acute depths of the COVID-19 impact, we worked with deeply distressed companies in the BSS sector. Christopher McLean explains how we helped our clients work through the uncertainties of 2020.

Business support services was a sector where in the acute depths of the COVID-19 impact, we worked with deeply distressed companies - yet also other companies that showed much resilience and actually saw the pandemic as an opportunity either for internal restructuring or an opportunity to benefit from dislocation in their peer set.

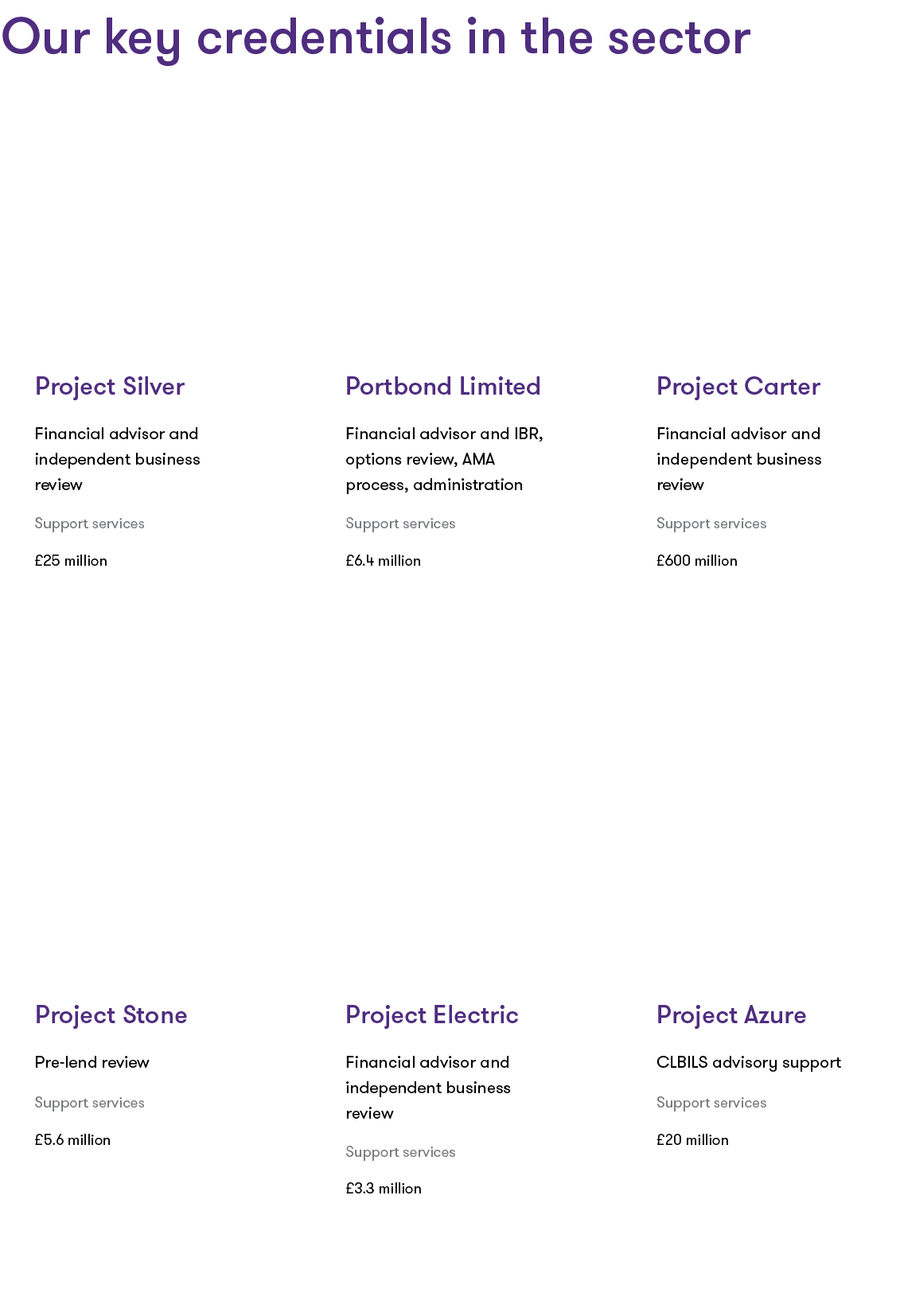

Our highlights in business support services

Discover our key credentials in the sector

The state of the sector

In early 2020 and before the UK lockdowns commenced, we saw the construction, construction services and building materials sub-sector begin to experience stress within their supply chains. The impact on supply from the Far East and Europe was already being felt in January and February 2020 and then the impact was felt within their customer base. We helped several clients navigate their exposures and contingency planning during this initial period, including accessing CLBILS and CBILS facilities. Conversely, this sub-sector was one of the first to show signs of recovery, albeit cautious, as the government prioritised the reopening of certain areas of the economy ahead of others. We were able to work with some clients who were able to make smaller and opportunistic acquisitions of competitors. Looking ahead into 2021, the outlook is still uncertain and whilst there are encouraging signs from an expected focus on national infrastructure spending from governments, this is yet to materialise onto order books for many.

The recruitment and training sub-sector was more mixed. As organisations looked to quickly and sharply reduce costs, recruitment and training spending was a clear target. More generalist (temp and perm-driven) recruiters bore the brunt and we helped our clients access emergency liquidity from a range of sources. Some, but by no means all, of the more specialist recruiters showed more resilience, as there was still demand for expert positions, particularly across IT, programming and regulatory/compliance positions. The end of 2020 and into 2021 showed resumed M&A activity, partly driven by potential capital gains tax changes, but challenges remain for many and it will depend on these businesses’ exposures to their end markets. 2021 could be a busy year in the sector for both M&A and restructurings.

We saw and still are seeing a range of outcomes across the facilities management sub-sector. We worked with companies who had to access the capital markets through rescue rights issues and have difficult negotiations with lenders and shareholders as liquidity quickly drained with no visibility as to a recovery. Those with end exposure to commercial real-estate, offices, retail and leisure - whether soft or hard providers - were particularly impacted and there is still a long and uncertain road to recovery. Some of the softer elements of the sub-sector, such as cleaning and security, were able to perform very robustly and we helped these clients access new debt facilities on a stand-by basis, but this was borrower-specific and not across the board.

Case study

Listed facilities management company

![]() During the first lockdown periods, we worked with prospective investors and lenders to diligence the adjusted business plan and calculate enterprise value and assess a sustainable capital structure.

During the first lockdown periods, we worked with prospective investors and lenders to diligence the adjusted business plan and calculate enterprise value and assess a sustainable capital structure.

A key part of our work was understanding the different divisions within the company given the scale and scope of their operations. In turn, we focussed on assessing the quantum and source of the monthly cash burn rate and how that matched against available liquidity. This was a large employer and understanding the impact on their people was crucial to really understanding the condition of the company and ability to execute its business plan.

The crisis and emergency nature of the situation meant we deployed a multi-disciplinary team with deep technical and sector expertise, drawing from our restructuring, debt advisory, transaction services, business consulting, M&A and valuations teams to assemble a dedicated project team who were fully focussed on helping our clients navigate this situation.

How we help our clients

Through the last year, we've ensured that all our clients in the business support services sector received help tailored to the requirements and circumstances of their particular subsector and situation.

The nature of this sector means its recovery or continued distress is, to an extent, a function of its end-customer exposure. We see some sectors recover faster than others, yet others like travel and hospitality have a difficult journey in 2021 and there will continue to be a direct impact on those that support such sectors.

Carefully understanding the end-customer and the true diversification of revenues, and stress-testing for further downturns and the compact of liquidity will be key themes for the sector in 2021 from a restructuring perspective.

The end of government support schemes, such as furlough will bring further problems for the sector to confront, together with the unwind of accrued liabilities and elevated financial debt on balance sheets.

Maintaining the confidence of lenders, shareholders and other important stakeholders will be vital in the next 12 months. Taking the initiative and leading from the front will be important to engender that confidence and we look forward to continue helping our clients in this sector as they navigate 2021.

![]()