Healthcare review Q1 2023

What's happening in healthcare?

The start of the year showcased the resilience of the healthcare sector, with strong M&A across the market and significant investment in emerging companies. One key trend is the growth of investor interest in pharma services – reflecting the sector's increasing complex needs.

This is a good reminder that companies across the sector should take stock of how well they're leveraging research and development tax relief. As current schemes undergo significant reform, its especially important for claimants to understand options and expectations.

You can find out everything you need to know in our latest quarterly review.

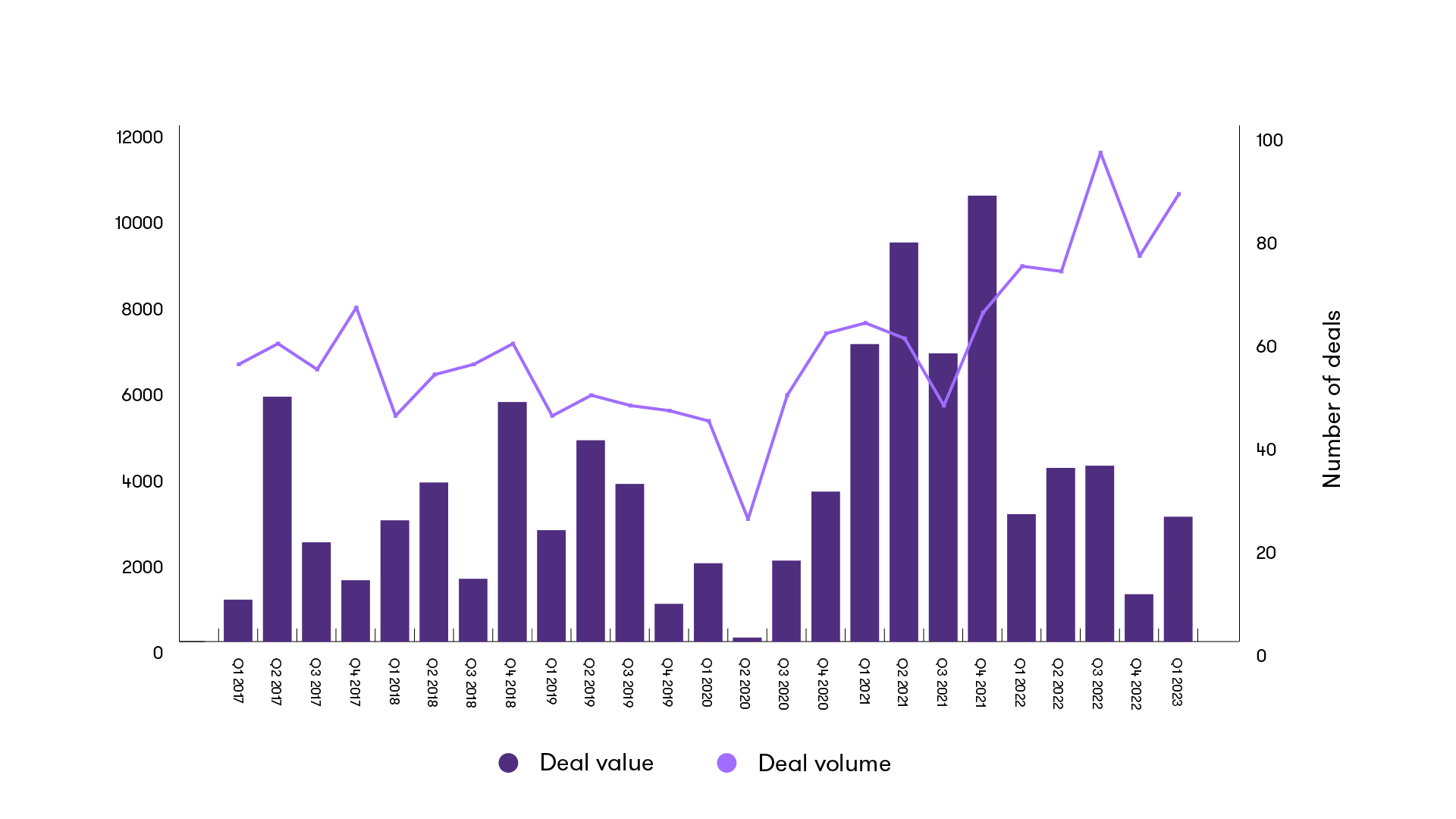

The first quarter of 2023 saw 87 private healthcare deals. This is a 17% increase on Q4 2022 and shows an active start and a recovery from the reduced levels of Q4 2022, but the wider M&A environment remains challenging.

The increase in activity in the private healthcare market has shown the robust nature of the sector in all areas, considering the economic climate and its attractiveness to investors. We've seen continued investment from private equity (PE) and private buyers from both the UK and abroad.

Announced M&A activity in Healthcare - quarterly

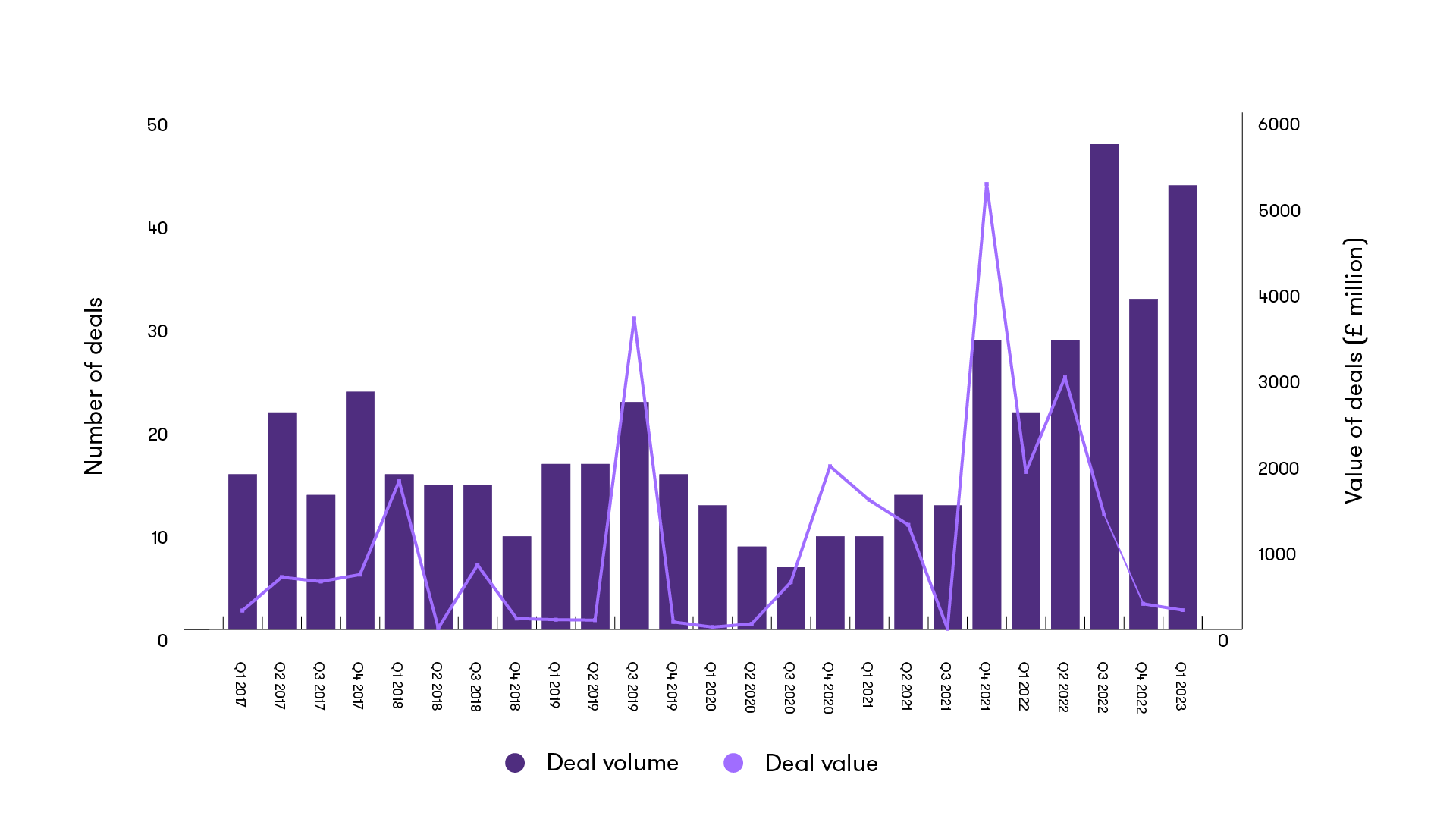

Once again, this quarter has seen investor interest across many private healthcare subsectors. PE/venture capital-activity has increased this quarter by volume, with 49% of deals involving PE/VC compared to the 42% last quarter. This reduction in deal value over a 12-month period indicates a high level of follow-on and further series funding.

Announced PE/VC activity in Healthcare - quarterly

Social care

Social care activity has retained a steady pace, with interest from private investors and PE. At the start of the quarter Impact Healthcare REIT acquired six homes form Morris Care for £56 million. Impact have also sold a home this quarter in Yorkshire that didn't fit its long-term strategic plans. This quarter also saw a couple of other exits from the market, with Target REIT exiting its presence in Northern Ireland by selling the four care homes it had there, and August Equity selling its two Sonnet Care Homes Essex two Gold Care. BGF have exited A Wilderness Way: a provider of specialised residential care, education, therapy, and outdoor adventure activities for vulnerable young people with complex needs. Sovereign Capital Partners LLP have acquired the asset.

Puma Property Finance have provided new funding to LNT Care Developments group, who are continuing to build and develop care homes across the country. BGF have also invested in BN Care this quarter, allowing them to grow from four to five care homes.

Homecare has also seen activity, with Cera Care acquiring Green Square Accords homecare asset, on which we advised.

Optimo continued their acquisition spree with the acquisition of Stepping Stones following three acquisitions in 2022.

Medical devices

The medical devices market remains attractive to all investor types.

BGF have invested in IQ Endoscopes Ltd, an early stage medical device manufacturers. Smith and Nephew have acquired Additive Instruments Ltd, a local developer and manufacturer of orthopedic surgical equipment for £10 million. CalibreScientific Inc acquired two UK businesses this quarter: TechniVal Group Ltd, a life-sciences laboratory equipment and services provider, and SciQuip Ltd, a Coalville, UK-based scientific equipment and laboratory supplier, seeing them grow their presence in the country.

The diagnostic testing market is still proving strong. Sherlock Biosciences Inc. has acquired Sense Biodetection Ltd, a molecular user-centered diagnostic tests manufacturer. Eurofins Food Testing UK Ltd has acquired Express Microbiology Ltd and EDX Medical Group plc has acquired Torax Biosciences Ltd, a Belfast, UK-based pilot scale fabrication of immune-assays and diagnostic testing-solution provider.

Digital health

The digital healthcare market has stayed strong as we’ve entered 2023, with interest from investors and overseas buyers. Octopus VCT plc has led two groups of investors this quarter, one to invest in HelloSelf Ltd, the local provider of digital therapy service platform, and the other to invest in Get Inflow Ltd, the science-based app designed specifically for people with ADHD. Mental health and wellbeing has attracted strong investor focus with wellbeing technology business Raiys acquiring The Healthy Employee. Unmind Ltd has acquired Floe Interactive Ltd.

USA-based Maven Clinic, a virtual clinic for women’s and family health has acquired the London based Naytal Ltd, a company that offers online pregnancy and postnatal support service, seeing a continued rise in women's health-support products.

Retail and multi-site healthcare

There's been progressive activity in the retail healthcare market. Fortius London Ltd (Fortius Clinic) has agreed to acquire Schoen Clinic London Ltd. Outside of London New Foscote Hospital Ltd, the provider of medical services, has acquired Royal Buckinghamshire Hospital Ltd, another local provider of medical services. Sano Physiotherapy Ltd backed by Solingen PE have acquired Back in Action Physiotherapy Ltd. Medigold, backed by BGF, acquired workplace health company Health Management. This acquisition has seen Medigold’s workforce increase to over 1,100, and gives them the ability to support UK businesses by making services more accessible.

Pharma services

Pharma services remain attractive to overseas and PE-buyers in the private healthcare space. Kester Capital made their fifth acquisition in the space, acquiring Map Patient Access, a deal on which we advised. Sciris (previously IMC Medical Communications) started the year with the acquisition of Source Market Access, giving them a wider market reach in the space. US PE Partners Group Holding AG have acquired Sterling Pharma Solutions Ltd, and Jounce Therapeutics Inc, the US-based clinical stage immunotherapy company acquired RedX plc. Open Health Communications LLP, a portfolio company of Astorg Partners SAS, has acquired Acsel Health LLC, a New York City based-life science strategy and advisory company.

Key Deals

Cera Care acquires Green Square Accords-homecare portfolio

Formed from the merger of Green Square Group and Accord Housing Association, Green Square Accord provides affordable housing and care to thousands of people across England, supporting some of the most vulnerable people in society.

The homecare portfolio which formed part of the sale consisted of seven registered branches located across the East Midlands and North of England, together employing around 600 care staff.

Founded in 2016, Cera Care is one of the UK’s largest domiciliary care providers and one of the fastest growing businesses in Europe. Cera represented a strong fit for the portfolio due to its reputation for innovation and care quality.

MAP Patient Access sale to Kester Capital

MAP is a leading provider of market access-consulting services to the pharmaceutical and biotech sectors, with expertise in rare and orphan diseases and cell and gene therapies. MAP’s integrated approach blends best-in-class consulting with membership, including its proprietary digital platform, MAP Online, which provides market-access intelligence to its customers. The founders sought a strategic investment partner to help deliver the next stage of the company’s growth. Kester Capital’s life sciences credentials made it the ideal partner to support MAP’s growth aspirations.

Fortius Clinic acquired Schoen Clinic London

Fortius Clinic, who are owned by the Netherlands-based Affidea have entered into an agreement to acquire Schoen Clinic London. Affidea Group is one of Europe's largest medical providers, operating over 330 clinics and leading outpatient and diagnostic centres.

Fortius have also created a centre of excellence for orthopedics and sports medicine in central London, with the acquisition of the Schoen Clinic London, a cutting-edge hospital that has 39 en-suite inpatient rooms, as well as onsite diagnostic imaging, outpatient consulting facilities, conservative treatments, surgical treatment, inpatient care, and physiotherapy. The acquisition will enable Fortius to expand their range of services and offer a more comprehensive service to their patients.

Healthcare M&A outlook

2023 started firmly for M&A in the private healthcare space, seeing an increase in deal activity compared to last quarter. All sectors remain active with medical devices, medical technology, and pharma services continuing to grow in the space, and social care continuing post-pandemic growth.

We're still seeing continued investments from private equity and commercial firms, showing UK private healthcare as a strong place for investment. There have been many smaller growth investments into emerging companies, which is very positive for the sector, and this will continue with the drive to digital innovation in the private healthcare space.

For more insight and guidance, get in touch with Peter Jennings, Jessica Sandercock, and Daniel Smith![]() .

.

The £40.8 billion UK pharma services faces several challenges, not least the prospect of over 70 global medicines going off patent by 2030. To fight back, large pharma services manufacturers are increasingly relying upon third parties to extend capabilities, discover new drugs, and reduce overheads.

As well as the revenue-sapping patent cliff, UK pharma services companies face the same challenges as other sectors: a rising cost base, political volatility, supply-chain disruption, and wage inflation. In addition, they must overcome sector-specific obstacles: regulatory compliance, and pricing and reimbursement. The cost and risks associated with investing in rapidly advancing (and often niche) technology are another barrier to profitability.

There are opportunities for pharma services service providers and suppliers to step in at all stages of the vast value chain – from contract research organisations (CROs) to specialist communication firms. They have become coveted acquisition targets for trade buyers and private equity, and Q1 2023 has already seen several deals in the sector.

Key deals in Q1 pharma services

Lucid Group creates end-to-end service

We advised Lucid Group on its January acquisition of Synetic Life Sciences.

Lucid is a consultancy specialising in healthcare communication strategy. By adding Synetic’s expertise in research, development and commercialisation, Lucid can advise on the entire lifecycle of medical innovations. Lucid is backed by Intermediate Capital Group, a global alternative asset manager.

Kester makes fifth life science acquisition

In March, our corporate finance team advised MAP Patient Access on its sale to Kester Capital. MAP provides market-access consulting services for pharmaceutical and biotech companies. The investment represents Kester’s fifth investment in the life sciences sector. Kester and management will also target acquisitions to accelerate the growth of the MAP platform.

Sygnature Discovery continues to buy and build

In January, Sygnature Discovery acquired drug discovery-research provider SB Drug Discovery. The deal is Sygnature’s second acquisition in the last year, following the integration of Peak Proteins in April 2022. Previous acquisitions included RenaSci in 2018 and Alderley Oncology and XenoGesis in 2020. It's backed by Five Arrows, the alternative assets arm of Rothschild & Co.

SCIRIS continues acquisition spree in UK

In January, Global healthcare communications company SCIRIS announced the acquisition of UK-based Source Health Economics – an agency specialising in health economics and outcomes research. This is SCIRIS’ sixth deal since Dutch private equity group Waterland invested in the firm in 2020.

The opportunities for investors

Investors are targeting pharma services service providers and suppliers for several reasons, including solid sales growth and government support.

Services growth outpaces core industry

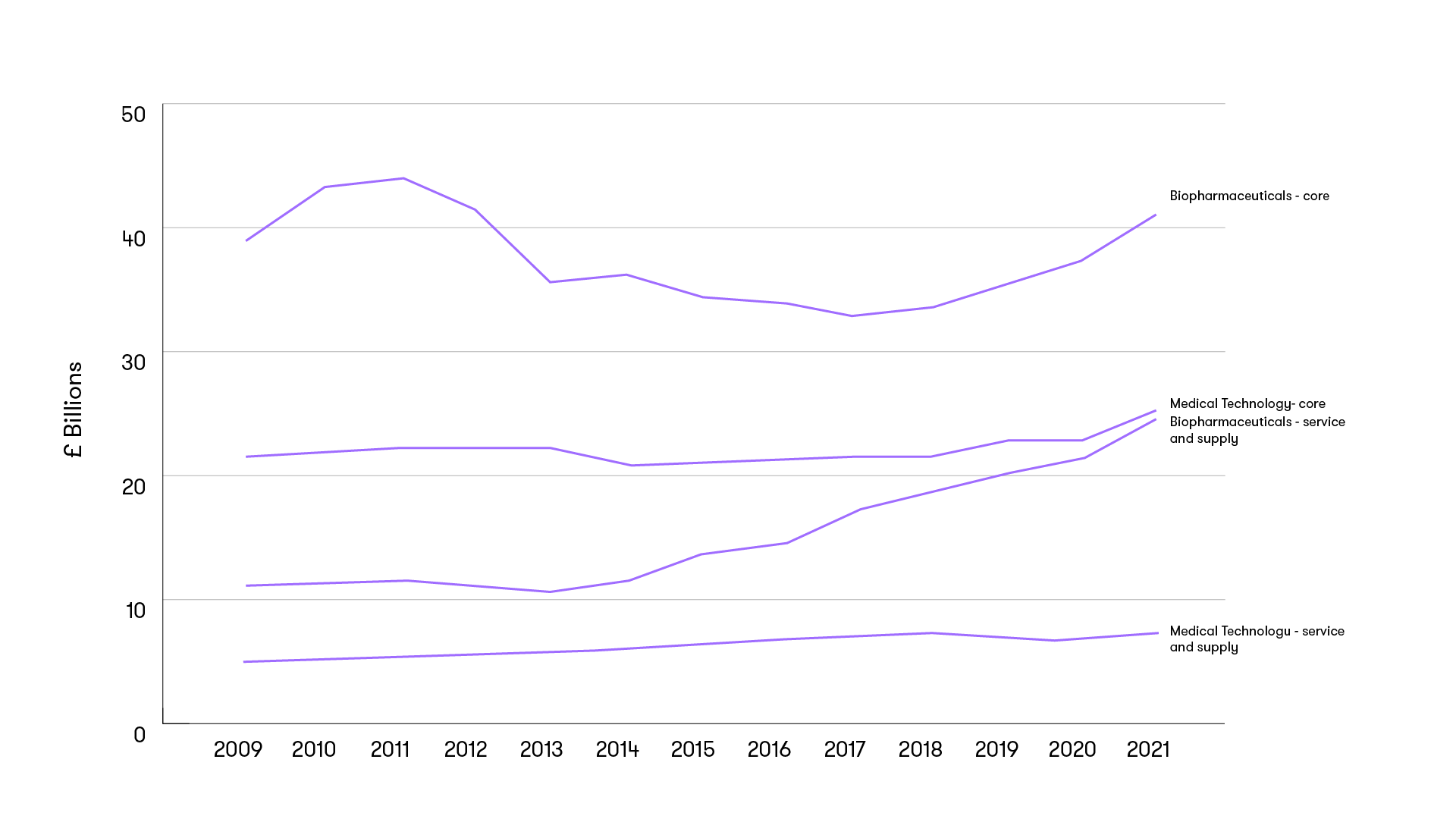

Service companies are growing faster than pharmaceutical companies. The core biopharmaceutical sector contributed £40.8 billion to the UK life science industry in 2020, an increase of 7% on the prior year, according to the most recently available government data. At the same time, the biopharmaceutical service and supply sector increased by 13% to £23.5 billion.

Turnover generated by the life sciences industry b sector

UK government backs science and innovation

In March, the government revealed its plans to transform the UK into a science and technology superpower by 2030. The plan is backed by over £370 million in new government funding to boost infrastructure, investment, and skills for growing technologies. The UK research and development tax regime is also undergoing significant reform designed to ignite innovation.

Growing interest from private-equity houses

UK private equity and lower mid-market US private equity recognises the attractiveness of the pharmaceutical sector, with several firms developing life sciences portfolios.

The middle market specialist

Limerston Capital has over £300 million assets under management and targets UK businesses valued at £20-£200 million. In March 2023, it acquired Concept Life Sciences, a UK-based contract research organisation (CRO) providing research and development services to global pharma services and biotechnology clients. This marked Limerston’s fourth life sciences investment.

The global player

Bridgepoint Group is a quoted private assets growth investor focussed on the middle market with over €37 billion assets under management. Its healthcare portfolio includes pharma services ingredients specialist Axplora, medical device firm Balt, and PharmaReview, which helps large pharma services groups with the medical review process.

The buy-and-builder

Sovereign Capital Partners is a buy-and-build specialist with several healthcare and pharma services investments. In 2021 it acquired the medical communication and regulatory writing agency Bioscript. Since then, it has added three acquisitions to Bioscript Group, including Fortis Pharma Consulting, market access firm Valid Insight and Meridian HealthComms.

The opportunities for business owners

To take advantage of the lively interest in pharma services and supply companies, those looking to sell must ensure their business fundamentals are in place.

For more insight and guidance, get in touch with Peter Jennings, and Daniel Smith.

Two UK R&D tax incentives are available to companies undertaking qualifying R&D activities: the SME scheme (for small and medium-sized enterprises) or the R&D expenditure credit (RDEC) scheme (for large companies or those with funded projects). Both can result in a cash benefit and are particularly valuable for businesses in the healthcare sector where R&D activity is typically high. In 2020-2021, the professional, scientific, and technical industry received the third highest amount of R&D tax credits (c. £1.7 billion) highlighting the government’s commitment to investing in R&D activities within this sector.

Spring Budget updates

At March’s Spring Budget, delivered just weeks ahead of some previously announced legislative changes becoming effective on 1 April 2023, the Chancellor made clear his intention to make the UK a science and technology superpower. The reforms reflect the government’s ongoing commitment to supporting R&D in the UK but there's also concern over the number of fraudulent R&D claims. To combat this, companies will have to meet additional compliance measures, which will affect how they prepare and submit claims.

R&D tax relief falls for SMEs

One of the key reforms is the change in rates of relief (see table). The rate of relief has increased for large companies who, from 1 April 2023, can benefit from relief of up to 15% of qualifying spend (10.5% previously). But the rate of relief for SMEs has decreased, with profit making SMEs now only able to claim relief of up to 21.5% of qualifying spend (24.7% previously) and loss making SMEs now only able to claim relief of up to 18.6% (33.3% previously).

The reductions in SME relief were met with criticism, particularly as many early-stage and research-intensive SMEs rely on these incentives to support growth and innovation. There was some respite offered in the Spring Budget, with certain ‘high intensity’ SMEs able to claim relief of up to 27% of qualifying spend. But it’s worth noting that this higher rate will only be available to loss-making SMEs with an R&D intensity ratio of 40% and above – our Spring Budget: R&D tax regime update has more detail. So while early-stage startups and deep research companies may meet the criteria, as companies grow and overheads increase, many may lose this additional support.

| RDEC | Pre 1 April 2023 | Post 1 April 2023 |

|---|---|---|

| Gross RDEC rate | 13% | 20% |

| Net RDEC (post CT*) | 10.5% | 15% |

*Corporation tax (CT) at either 19% or 25%

| SME | Pre 1 April 2023 | Post 1 April 2023 |

|---|---|---|

| Additional deduction | 130% | 86% |

| Profit-making company’s tax benefit | 24.7% | 21.5% |

| Loss-making company’s tax benefit | 33.3% | 18.6% |

| R&D-intensive loss-making company’s tax benefit | 33.3% | 27% |

Additional compliance rules to help tackle fraud

As part of the initiative to tackle fraudulent claims, the government had intended to introduce an Additional Information Form (AIF) for accounting periods beginning on or after 1 April 2023, requiring further information in a prescriptive format and outside of the usual corporation tax return. However, at the Spring Budget, it was announced that the AIF commencement date has been brought forward to all claims made on or after 1 August 2023, meaning that any claims submitted on or after this date won't be valid without this additional information. Companies that may be submitting claims on or after 1 August 2023 need to plan what work they need to do to ensure compliance.

HMRC has now released the AIF with details of the new information requirements.

A key requirement is the need to prepare and submit a prescribed number of technical narratives to support the claim, with HMRC requiring a minimum expenditure coverage of 50%. This could result in significant additional work for businesses in the healthcare sector, for example pharmaceutical and life sciences companies, who undertake hundreds, if not thousands, of projects in any given year.

The government is also moving forward with a controversial claim notification requirement. It requires first-time claimants, or companies who haven't made a claim in the preceding three years, to inform HMRC if they plan to make a claim. This needs to be done digitally and within six months of the end of the accounting period to which the claim relates.

Other key changes to R&D tax regime

From 1 April 2023, there are changes to the categories of cost companies can claim. Data licence and cloud computing service costs are now eligible, and pure mathematics is now considered a field of science that may benefit sectors such as artificial intelligence and robotics. Previously announced restrictions on overseas expenditure, for example on subcontractors and externally provided workers, have been delayed until accounting periods beginning on or after 1 April 2024.

And it's worth noting HMRC's ongoing consultation on merging the RDEC and SME schemes, with the intention of simplifying the regimes. Expect an update this summer.

Qualifying R&D activities in healthcare

While this is a period of significant reform, the government has expressed an ongoing commitment to supporting R&D in the UK and to ensuring the UK’s R&D tax relief regimes are globally competitive and fit for purpose. Healthcare providers should ensure claims are robust and compliant, and that all areas of R&D are being captured and explored.

As well as more traditional drug development activities, qualifying activities can also include:

- development of digitalised solutions to improve patient care

- advancing medical devices to improve performance

- research into how to tailor treatments to an individual’s genetic makeup

- adaptation of artificial intelligence and machine learning techniques to assist with drug discovery and development.

For more insight and guidance, get in touch with Ian Rowland , Peter Jennings, Daniel Smith, and Sophie Edwards.