How we help our clients

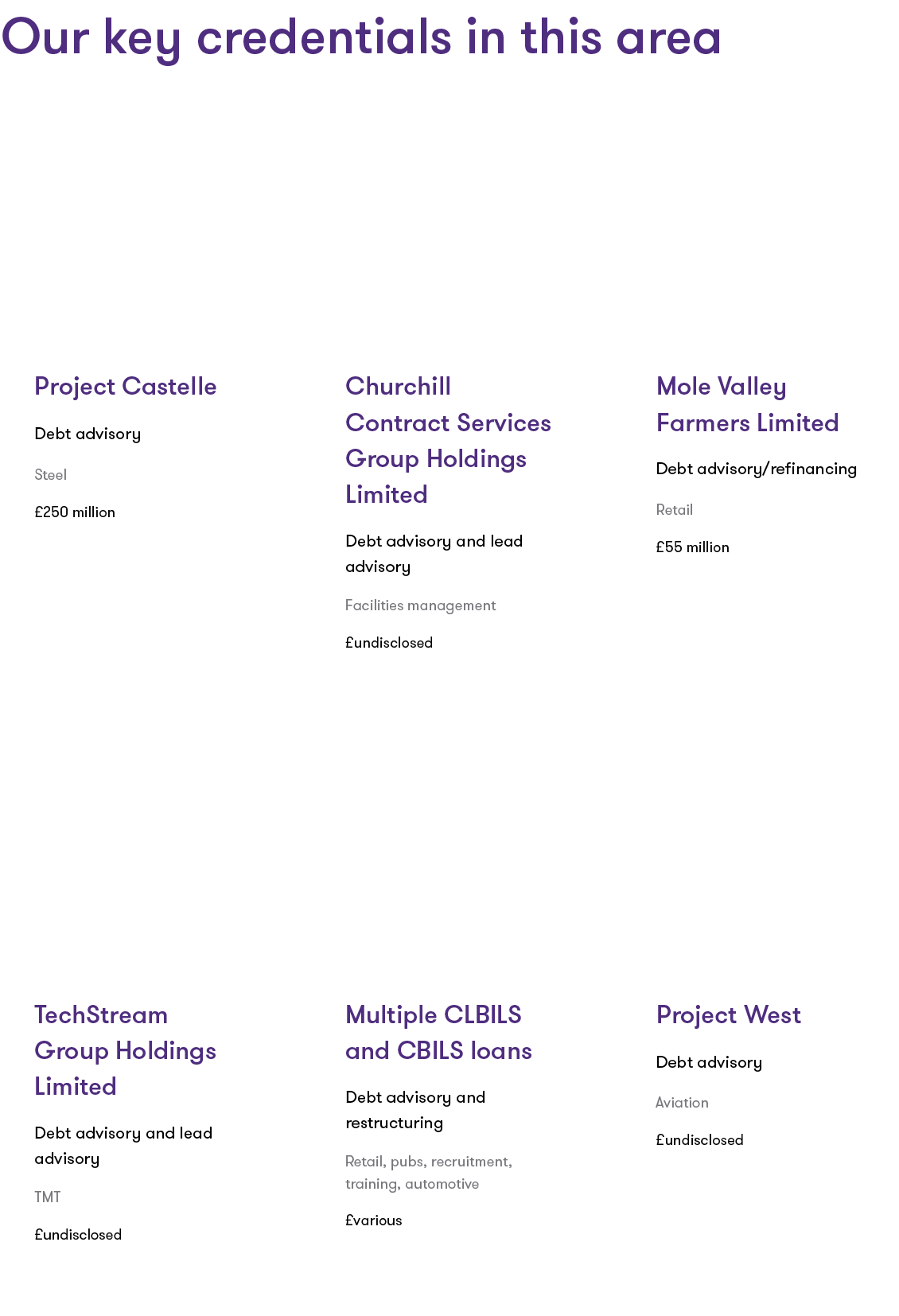

During this period of acute stress, we helped a number of our clients raise additional liquidity from CLBILS and CBILS across a range of sectors, including pubs, recruitment, leisure, travel, automotive and steel.

However, a large number of our clients were not able to access the CLBILS and CBILS programmes due to eligibility or credit profile issues and we worked with these clients to explore other avenues of finance.

We work with borrowers of all sizes and quality to access the right type of debt financing, ranging from bilateral loans with high-street banks, private equity-backed unitranche structures, asset-based lending across different asset classes and more esoteric special situations lending. This can be for refinancing, working capital, acquisition finance or dividend recapitalisations, amongst other uses.

Carefully constructing a detailed credit story, explaining the unwind of the balance sheet when government support is withdrawn, and stress testing forecasts for unforeseen scenarios are the key themes so far this year.

2021 has been extremely busy already for debt financing and refinancing and looks set to continue as more confidence and clarity returns to more sectors across the economy. We're confident that we can assist you with your financing requirements.

Find out more about how our debt advisory team can support you.