In the acute depths of the COVID-19 impact, we worked with deeply distressed companies in the BSS sector. Christopher McLean explains how we helped our clients work through the uncertainties of 2020.

Business support services was a sector where in the acute depths of the COVID-19 impact, we worked with deeply distressed companies - yet also other companies that showed much resilience and actually saw the pandemic as an opportunity either for internal restructuring or an opportunity to benefit from dislocation in their peer set.

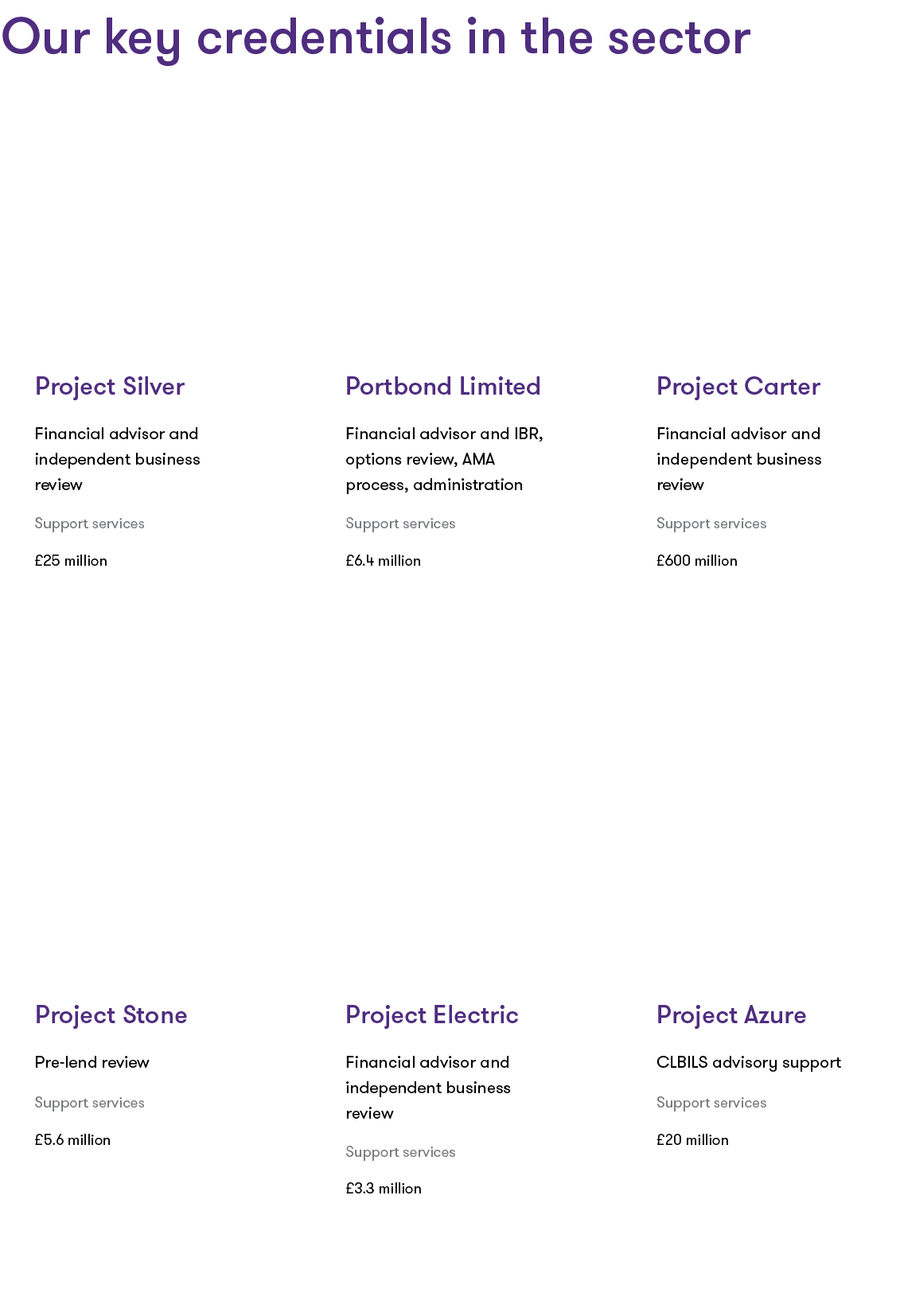

Our highlights in business support services

![Our highlights in business support services]()

Discover our key credentials in the sector

The state of the sector

In early 2020 and before the UK lockdowns commenced, we saw the construction, construction services and building materials sub-sector begin to experience stress within their supply chains. The impact on supply from the Far East and Europe was already being felt in January and February 2020 and then the impact was felt within their customer base. We helped several clients navigate their exposures and contingency planning during this initial period, including accessing CLBILS and CBILS facilities. Conversely, this sub-sector was one of the first to show signs of recovery, albeit cautious, as the government prioritised the reopening of certain areas of the economy ahead of others. We were able to work with some clients who were able to make smaller and opportunistic acquisitions of competitors. Looking ahead into 2021, the outlook is still uncertain and whilst there are encouraging signs from an expected focus on national infrastructure spending from governments, this is yet to materialise onto order books for many.

The recruitment and training sub-sector was more mixed. As organisations looked to quickly and sharply reduce costs, recruitment and training spending was a clear target. More generalist (temp and perm-driven) recruiters bore the brunt and we helped our clients access emergency liquidity from a range of sources. Some, but by no means all, of the more specialist recruiters showed more resilience, as there was still demand for expert positions, particularly across IT, programming and regulatory/compliance positions. The end of 2020 and into 2021 showed resumed M&A activity, partly driven by potential capital gains tax changes, but challenges remain for many and it will depend on these businesses’ exposures to their end markets. 2021 could be a busy year in the sector for both M&A and restructurings.

We saw and still are seeing a range of outcomes across the facilities management sub-sector. We worked with companies who had to access the capital markets through rescue rights issues and have difficult negotiations with lenders and shareholders as liquidity quickly drained with no visibility as to a recovery. Those with end exposure to commercial real-estate, offices, retail and leisure - whether soft or hard providers - were particularly impacted and there is still a long and uncertain road to recovery. Some of the softer elements of the sub-sector, such as cleaning and security, were able to perform very robustly and we helped these clients access new debt facilities on a stand-by basis, but this was borrower-specific and not across the board.