Retail review Q4 2022

What's the outlook for retail?

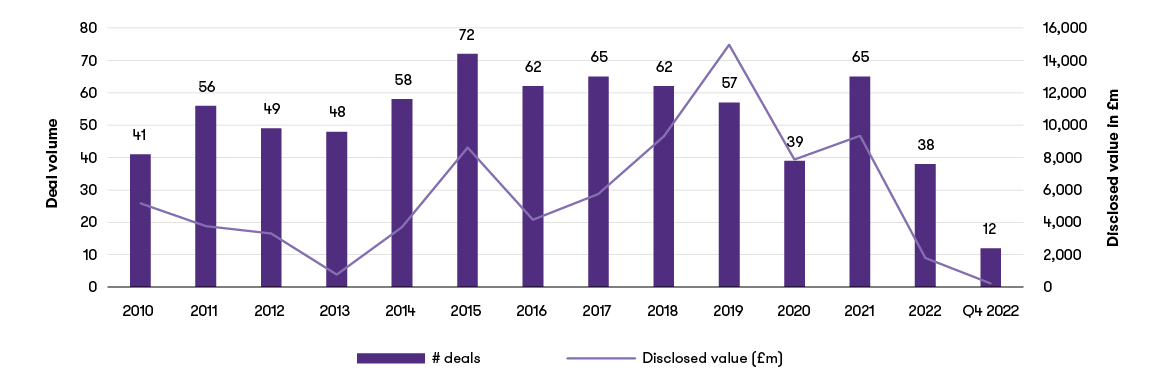

Businesses in the retail sector are still on a bumpy road. M&A activity in the final quarter of 2022 continued to fall short of expectations 12 months earlier - before the continued impact of post-pandemic issues and new difficulties caused by the war in Ukraine.

Q1 deal volumes continued 2021’s strong run as the desire to either exit or receive new growth investment continued for the many retailers that had traded well through the pandemic. Then the war in Ukraine and the knock-on effect on cost of living in the UK put everything on hold. Record food, fuel, and energy prices, and rising interest rates squeezed household spending, causing investors to shy away from consumer-facing deals.

There were 46 retail deals in 2022, though Q1 did most of the heavy lifting. Q4 deal volumes fell to just eight transactions – the lowest figure since Q3 2020.

UK retail M&A volume/value

Onwards and upwards: six reasons for retail optimism

Despite a drop in retail deal volumes towards the end of the year, there are six reasons to feel optimistic about retail M&A in 2023.

1 Trade renews appetite for consolidation and bolt-on deals

Trade isn't straying far from its core offering, but is increasing its existing market share either through geographical expansion or adding complementary brands.

2 ESG continues to attract investors

Last year notable deals in this high-growth area included Big Green Smile, Childs Farm, and childrenswear retailer, Jo Jo Maman Bebe.

3 Private equity unshaken on consumer-facing sectors

PE houses are determined to proceed if the asset is right. This could mean investing in a niche, such as safety equipment, or a defensive part of the market, such as luxury goods.

4 Consumers still spending...when the offer is right

Christmas trading updates show that people are buying what they want. Marks & Spencer reported a boost in like-for-like food sales (up 6.3%), with clothing and home up 8.6%. Tesco and Next also reported strong festive figures.

5 Retail services still moving forward

Though not strictly ‘retail’ (and not included in our data), there is momentum in retail services deals – particularly those that deliver cost savings or increase revenue for retailers. Example Q4 acquisitions include Appreciate Group’s acquisition of gift card business Paypoint for a reported £83 million.

6 Prime minister's pledge on inflation

Rishi Sunak has promised to reduce the inflation rate to around 5% by the end of 2023. While consumer prices will still be higher than in 2021, this may prevent a further interest rate increase, protecting household spending from further squeeze.

Key deals in retail

Round up of Q4 deal activity

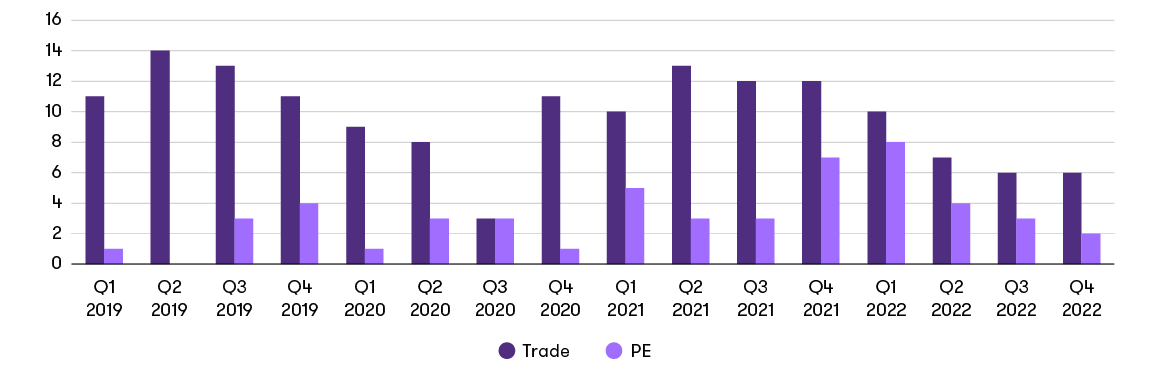

Trade vs private equity deals

Trade continues to dominate M&A activity in the retail space. In Q4, there were six trade and two private equity (PE) deals. A cooling in PE enthusiasm towards consumer-facing sectors will intensify this year until there is more economic stability. However, as with Ro&Zo, there are exceptions when deal fundamentals are strong.

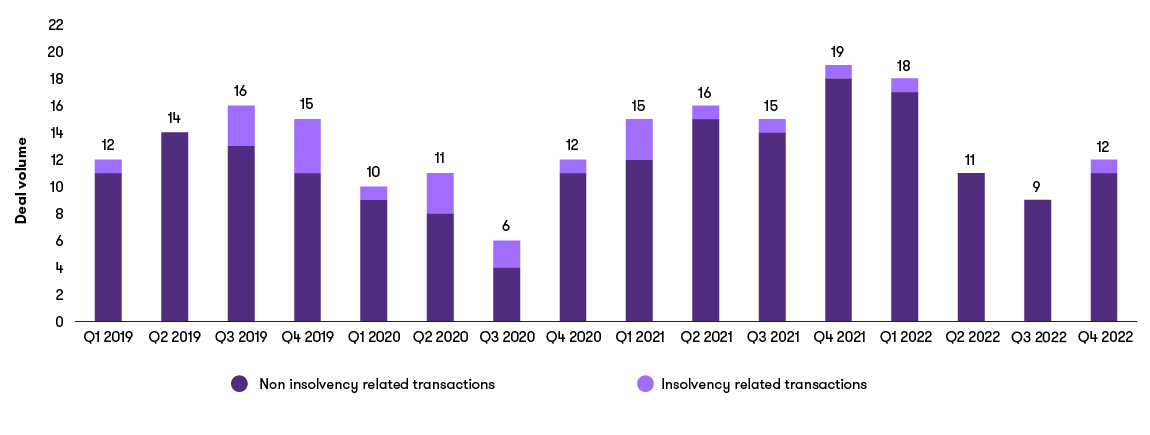

Restructuring and rescue deals

There was just one explicit rescue deal reported this quarter. Online mattress retailer Eve suffered from a downturn in online furniture sales and called in administrators in October. It blamed an “economic tsunami” that included the cost-of-living crisis. Bensons for Beds (backed by Alteri Investors) bought the brand, intellectual property, and website. The deal will give Bensons a new channel to reach a younger customer base.

Our data only counts insolvent retailers, so may not reflect the number of struggling retail businesses in the UK. In 2023, rescue deals will create opportunities for trade buyers to add new brands, geographies and customers.

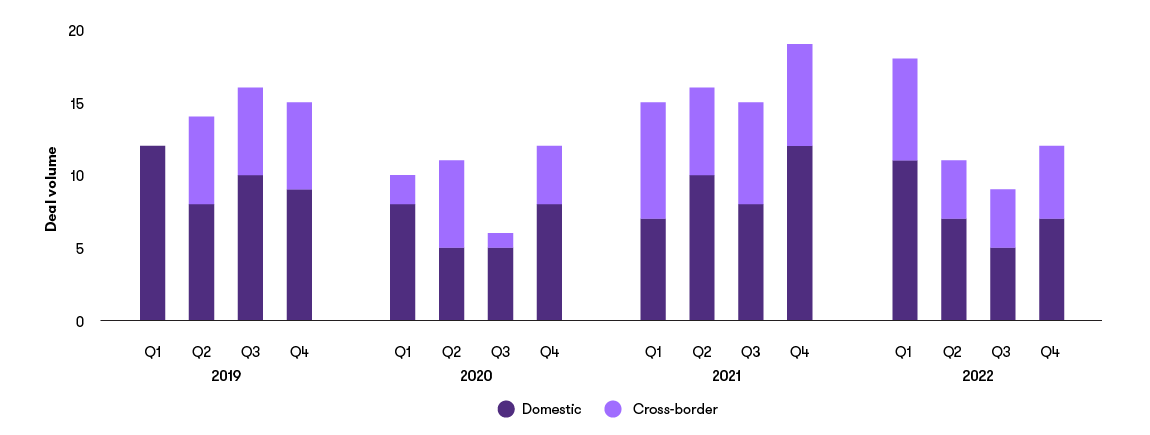

Overseas interest

Deals by acquiror domicile

There was a 50/50 split between domestic and overseas buyers in Q4. Two of the international deals involved Chinese buyers. One was Viva China’s acquisition of a 49% stake in Clarks Shoes owner LionRock Capital, adding to the 51% stake it already owned. The move complements Viva’s strategy to expand its apparel business.

Get in shape for 2023

Though deals will continue to get done in 2023, they just might be a bit harder (in the first half of the year, at least).

References:

- Internet sales as a percentage of total retail sales (ratio) (%), ONS, 2023

- UK spending on credit and debit cards, ONS, 2023

- COVID-19 Community Mobility Reports, Google, 2022

For more insight and guidance, get in touch with Nicola Sartori.

Retail volumes in Great Britain declined by 5.8% percent in December 2022, compared to the prior year, while the value of retail sales went up by 3.8%.

Lenders are being extra diligent in scrutinising top-line sales performance and margin performance. They're distinguishing between price and volume, and expect its borrowers or prospective borrowers to be able to produce high quality and timely data that shows the real underlying performance of the company.

Clear data improves credibility when approaching lenders for additional financing. However, given the divergent performance across the different sub-sectors of retail, and among companies themselves, not all requests for additional financing will be approved. In this scenario, companies have various options, ranging from self-help actions through to new equity.

In-between those two ends of the spectrum is the option of approaching new lenders. These might not be the traditional lenders with which many will be familiar. Deep liquidity is still available from a range of sources, such as asset-based lenders and hybrid capital providers.

While there's no guarantee of access to debt capital, many of these alternative lenders have different risk appetites to traditional lenders and can devise more creative funding solutions. Tangible assets and intangible assets, such as intellectual property, can all have value, and capital repayments can be better flexed to match the cash flow profile of the business.

Understanding options is important for those companies operating in the retail sector. The substantial difficulties that many have faced in Q4 2022 and continued uncertainties into 2023 means mapping out the different options and supporting conversations with new funders with clear and credible data will be critical for many operators over the next 12 months.

For more insight and guidance, get in touch with Christopher McLean.

While some retailers have made significant progress in reducing their internal carbon footprint related to greenhouse gas (GHG) scopes 1 and 2 emissions, others have fallen short of their commitments across all GHG scopes 1, 2 and 3 emissions, often due to a range of factors.

Limited visibility on supply chains

One of the key challenges facing retailers is the complexity of their supply chains. Most retailers today rely on a vast network of suppliers and vendors to produce and distribute their products, which makes it difficult to track emissions across the entire value chain. Even if a retailer can accurately measure the emissions associated with their own operations, they may have little visibility into the emissions generated by their suppliers, transport providers, or other partners.

High cost of sustainability measures

Another major hurdle for retailers is the high cost of implementing emissions reduction initiatives. Many companies lack the resources or expertise to develop and deploy effective sustainability strategies and may struggle to secure the necessary funding to support these efforts. Even if a company has the financial resources to invest in emissions reduction measures, they may face significant challenges in persuading their shareholders to prioritise sustainability over short-term profits.

Moreover, many retailers face fierce competition in the marketplace, which can make it challenging to invest in long-term sustainability initiatives. In an industry where margins are often thin and price is a major factor in purchasing decisions, retailers are hesitant to pass the costs of emissions reduction efforts onto consumers in the current economic climate. As a result, they may struggle to find the financial CAPEX necessary to invest in new technology or infrastructure that would help them achieve their emissions reduction goals.

Variable regulatory incentives

Finally, many retailers may lack the regulatory incentives necessary to motivate them to take bold action on emissions reduction. While some countries and regions have implemented strict regulations and standards around sustainability, others may have weaker or non-existent policies in place. This can create a situation where companies that operate in less-regulated areas have little motivation to prioritise emissions reduction, as they may not face any penalties.

Despite these challenges, many retailers recognise the urgency of addressing climate change and are taking steps to reduce their carbon footprint. Some are investing in renewable energy, while others are working with suppliers to reduce emissions throughout the supply chain. Still, there's much work to be done if the retail industry is to play its part in mitigating the impacts of climate change. By addressing the challenges facing the sector, retailers can move closer to achieving their emissions reduction targets and play a leading role in the transition to a more sustainable future. This can only be achieved by retailers collecting accurate baseline data across Scopes 1, 2, and 3. The data is critical in forming an informed net zero transition plan and strategy focused on emissions reduction across the value chain.

Get the latest insights, events and guidance about TMT straight to your inbox.

![]()