Low-cost government support has been an essential lifeline for many businesses through the last twelve months, providing the headroom between continued trade and failure. As we emerge from the trading restrictions resulting from the pandemic, managing liquidity through ongoing economic uncertainty will be the key to success.

However, the funding landscape is set to become increasingly more complex and challenging. Understanding your options and managing the risks will be crucial to obtaining the optimum funding solution. Find out how our dedicated ABL team can support you, whether you are looking for a turnaround solution or facilities to enable your business to take advantage of the opportunities that lie ahead.

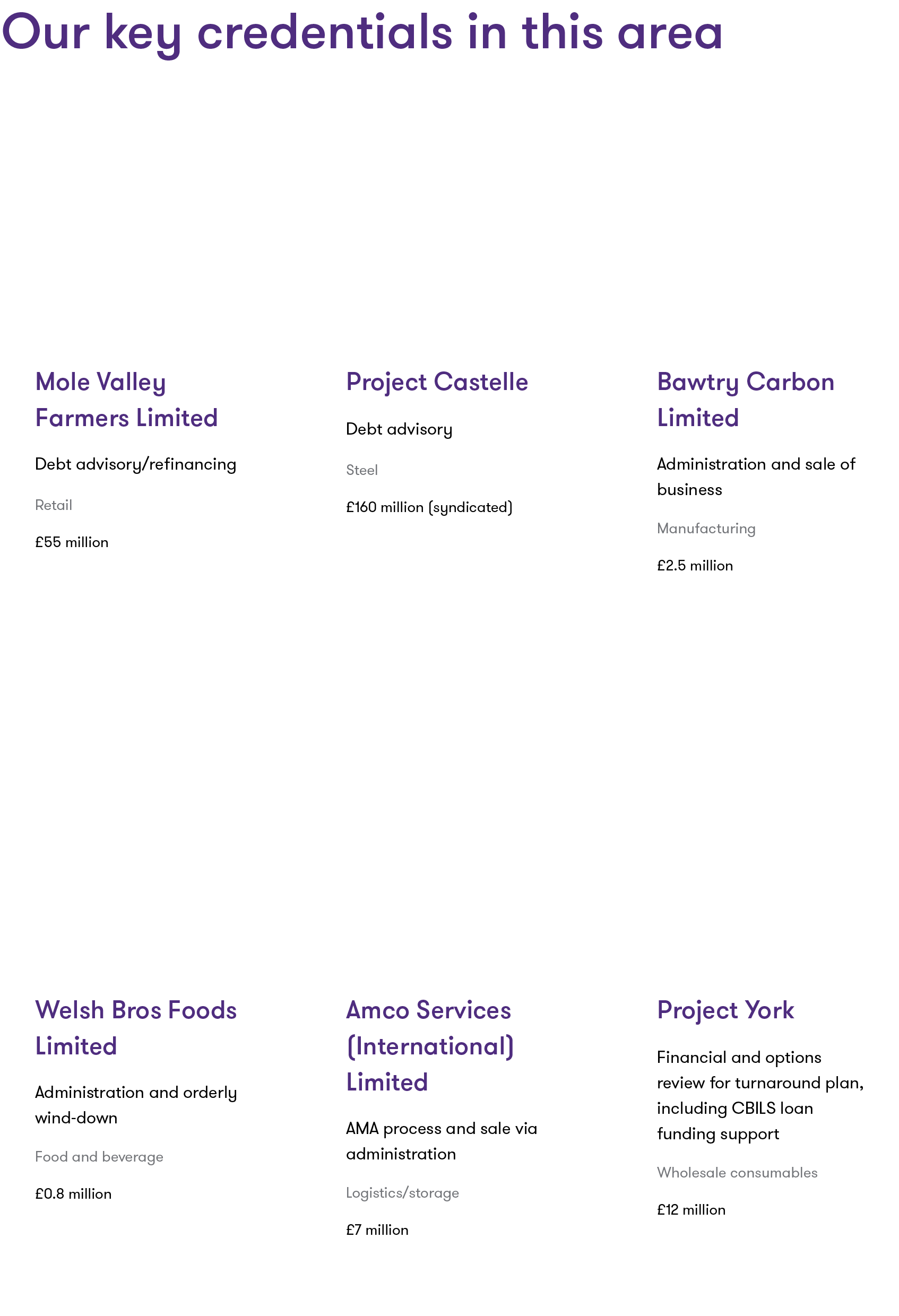

Discover our key credentials in this area

The state of asset-based lending

In the early part of 2020, the UK economy encountering a period of volatility, characterised by political and economic uncertainty with limited growth.

This challenging environment was exacerbated by the impact of COVID-19, affecting businesses across most sectors, and leading business owners, management teams, lenders and advisers into uncharted territory.

Access to government-backed low-cost finance, and other financial support schemes, has played a significant part in reducing requirements from existing commercial finance facilities, but this will not go on forever.

Meanwhile, fallout from the US election and Brexit will undoubtedly lead to continued social, political and economic uncertainty well into 2021.

Despite this uncertainty, ABL is uniquely placed to support businesses, as the flexibility of the products offered allows funders to react and respond to the ever-changing economic landscape.

In addition, with many corporates experiencing low LTM EBITDA results in 2020, there are increasing challenges in the traditional leveraged lending space as we enter 2021.

ABL is able to offer a solution here that more efficiently leverages assets. This can be as an alternative to, or in partnership with, leveraged finance or revolving unitranche facilities provided by credit funds.

While 2021 will present a significant opportunity for asset-based lending, opportunity in times of uncertainty presents risk, which must be managed carefully.