Financial pain to reach £65 billion as cost of living crisis expected to last 10 more months

The typical UK household will be £2,300 worse off by the time the cost of living crisis comes to an end.

As interest rates sharply rise to combat sticky inflation, new research from Grant Thornton UK LLP and Retail Economics shows the true cost of the financial burden faced by UK households. Into its second year, the Cut Back Economy shows little sign of easing as consumers continue to search for ways to reduce their non-essential spending and alleviate pressure on personal finances.

£65 billion hit to household spending power

The UK’s cost of living crunch is far from over. Our research shows that we’re only three quarters of the way through the financial squeeze, with 10 months of spending power erosion still to come.

But with inflation remaining stubbornly persistent, sharply rising interest rates has widened the scope of households impacted by the cost of living crisis, with many middle and higher income households bracing for significant increases in mortgage repayments over the year ahead.

UK households have already experienced the biggest squeeze in generations. The spiralling cost of food, energy and other daily expenses – and the failure of wages to keep pace – has cost UK households £50 billion in lost disposable income so far (Oct 2021 to May 2023).

However, UK households face a further £15 billion of spending power erosion before growth in spending power returns.

Based on current projections, the cost of living crisis is expected to last for 31 months overall (Oct 2021 to May 2024), with the typical household left over £2,300 worse off over that period. In total, the cost of living crisis is forecast to wipe out £65 billion from household spending power, based on economic modelling within the report.

Graph 1: £15 billion of household spending power erosion still to come, as the cost-of-living crisis persists longer than expected

Source: Grant Thornton, Retail Economics

Consumers’ cut back intentions remain high. Our research shows almost nine in ten (88%) households plan to cut back their spending (i.e. spend less, delay or cancel purchases), over the current financial year (to April 2024). This proportion remains broadly consistent with last year’s survey (86% - May 2022), as ongoing financial pressures and economic uncertainty continue to take their toll on consumers.

Graph 2: Almost two thirds (65%) of households intend to cut back across the majority of their spending this financial year

Source: Grant Thornton, Retail Economics

What’s more, the scale of cut back has intensified. Nearly two thirds (65%) of consumers intend to cut back across most, if not all, areas of their spending, up from a little over half (52%) a year ago.

The increase on last year is being driven by a step change in the proportion of middle and higher income households planning to cut back. Peak inflation may have passed, but the impact of higher interest rates on their personal finances, alongside lower levels of savings compared to a year ago, is weighing heavily on consumer behaviour and spending intentions.

Almost two in five households are ‘financially distressed’

Cut back intentions vary by household, depending on their age, income and individual persona.

The report found the proportion of ‘Financially Distressed’ households has increased slightly compared to last year, rising from 36% to 38% of households. These households plan to cut back across most (if not all) of their non-essential spending – a decision taken out of necessity, as low incomes and/or high debt levels leave little room for these households to manage higher bills and rising interest rates.

Graph 3: Cut back consumer cohorts

Source: Grant Thornton, Retail Economics

More than one in four (28%) households are ‘Squeezed Spenders’, who recognise the need to cut back across some of their spending but generally prefer to borrow, dip into savings or use buy now pay later schemes than let money worries get in the way of their desires.

‘Comfortable Cautious’ consumers make up just over a fifth (22%) of households. These households are financially secure but still worry about the cost-of-living crisis, choosing to cut back across some of their spending out of precaution.

Only 12% of households are ‘Financially Immune’ with no plans to cut back their spending, down from 14% a year ago.

Recessionary behaviours persist

Although the UK economy has managed to avoid a technical recession, many consumers are adopting ‘recessionary’ behaviours as they operate with diminished spending power.

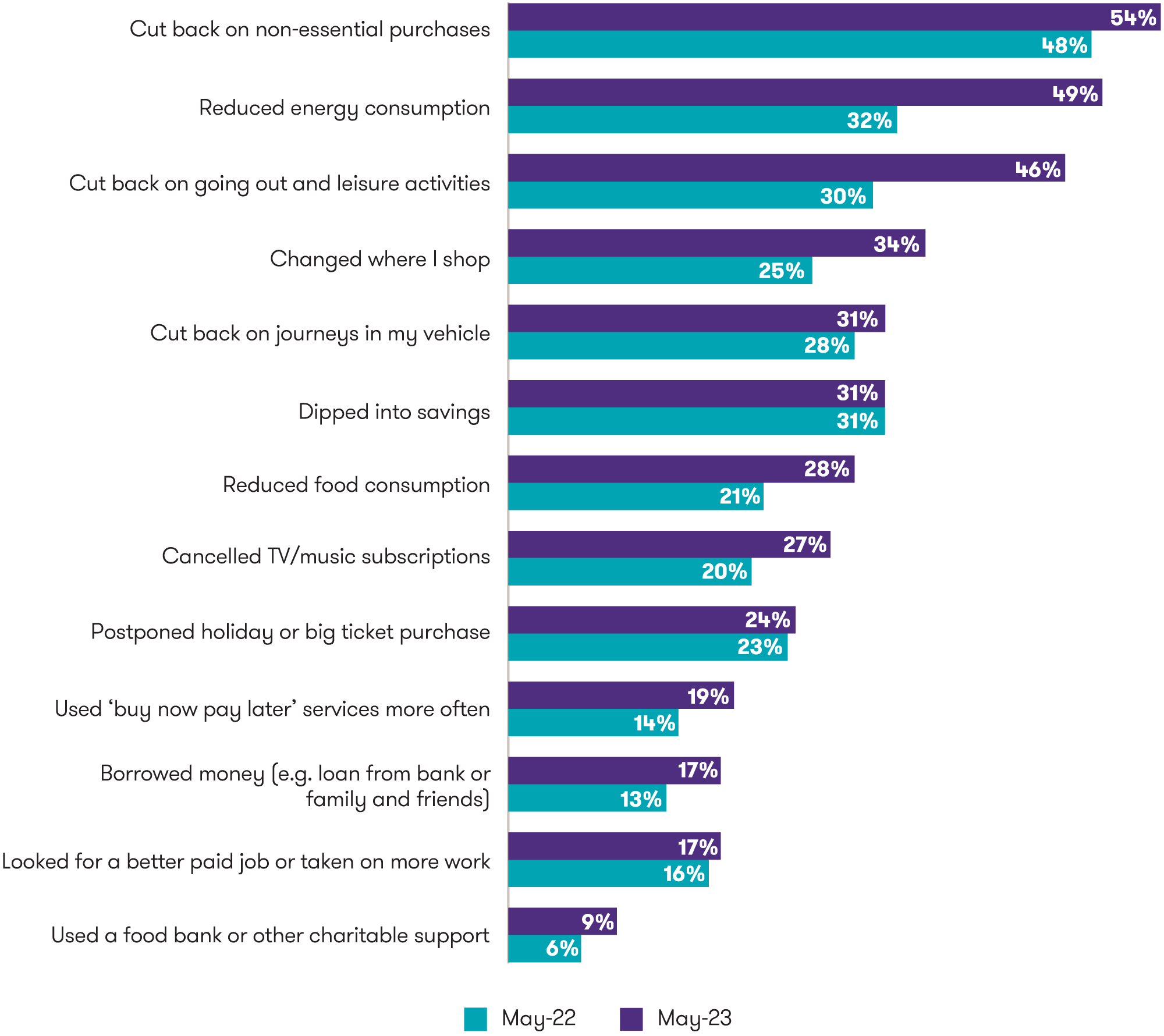

Over half (54%) of UK consumers are cutting back on non-essential shopping, while one in three (34%) have changed where they usually shop, including switching to cheaper brands or retailers.

Meanwhile, almost half of all consumers (46%) have made the decision to cut back on ‘going out’ to a pub, restaurant or other leisure venue, a notable increase from last year (30%).

Graph 4: Many consumers continue to adopt recessionary behaviours

Source: Grant Thornton, Retail Economics

However, the research shows clear polarisation by income. The most affluent are five times less likely to adopt cut back behaviours, with only around one in ten high income households dining out less often, cutting back on luxuries, or switching to own-label products, versus around 60% for the least affluent.

Spending priorities: hospitality the focus of cut back intentions

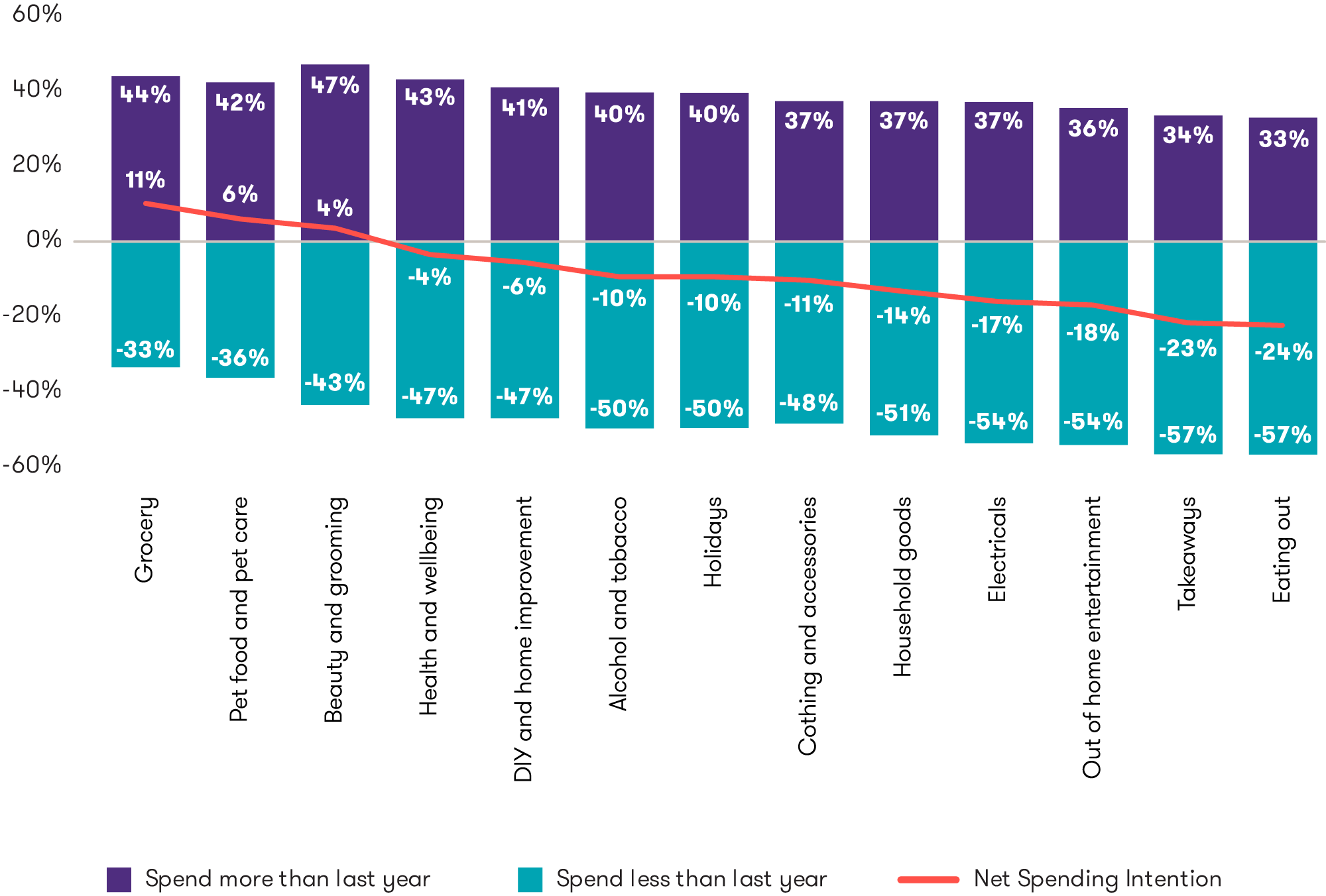

Grocery, pets and personal care are the only categories to forecast positive net spending intention this financial year (to April 2024), as consumers continue to prioritise essentials (Graph 5).

Hospitality stands out as the primary area where consumers will cut back over the remainder of the cost of living crisis, with eating out and takeaways showing the weakest/lowest spending intention.

Following an initial surge in spending after pandemic restrictions, restaurant and hospitality demand has softened as operators pass on significant increases in food and energy bills to customers, making going out more expensive.

Graph 5: Consumer spending intentions by category: How do you intend to spend on the following categories over the next 12 months?

![Bar chart showing consumer spending intentions by category for the next 12 months: Survey question - How do you plan to allocate your budget among the following categories?]() Bar chart showing consumer spending intentions by category for the next 12 months: Survey question - How do you plan to allocate your budget among the following categories?Download Image

Bar chart showing consumer spending intentions by category for the next 12 months: Survey question - How do you plan to allocate your budget among the following categories?Download Image

Source: Grant Thornton, Retail Economics. Note: Net spending intention = spend more minus spend less. Note “Spend the same as last year” was also an option for respondents.

Consumers are more reluctant to cut back on holidays. Indeed, holidays emerge as a top priority among discretionary spending categories, prioritised above clothing, electricals, and household goods.

Once seen as a ‘luxury’, holidays are now seen almost as a must-have for households, driven by continued pent-up demand for travel post-pandemic, but also desires to ‘take a break’ amidst prolonged economic instability.

Given the choice, consumers of all ages prefer to cut back on non-essential shopping trips and big-ticket retail purchases, ahead of sacrificing plans for a holiday or trips away (Graph 6).

Rather than cancel or postpone holidays, consumers are embracing clever spending strategies such as travelling off-peak, booking shorter stays, and switching to cheaper destinations.

Graph 6: Holidays prioritised over shopping trips: Do you plan to do any of the following this year in response to the increased cost of living?

Source: Grant Thornton, Retail Economics.

Expert views

Nicola Sartori, Head of M&A Retail and Consumer at Grant Thornton UK LLP, said:

“The 'Cut Back Economy' continues to exert its unyielding influence on consumer behaviour, presenting formidable challenges for retail, leisure, and hospitality businesses. Consumer confidence remains fragile, as the intention to cut back on non-essential purchases continues.

“The £54 billion online sales boost during the pandemic can now be viewed as temporary as people are starting to prefer shopping in stores again, seeking value for money and in-person shopping experiences. However, the way that customers research and decide how to buy has become more complex, and people are still prioritising online to find good deals and manage spending. To navigate this uncertainty, it is crucial for businesses to build this changing consumer behaviour into their long-term strategies.”

Richard Lim, CEO at Retail Economics says:

“The relentless rise in interest rates has completely changed the narrative around the cost of living crisis. What started as a crisis among the least affluent households has evolved to capture a much wider array of income groups as housing affordability comes under enormous pressure.

As pandemic savings have been whittled away, the squeeze on finances has become a war of attrition for many households. While peak inflation may have passed, households still have around 10 months of pain to come where cutting back spending will intensify for many households.”

About the report

The Cut Back Economy 2023 report, produced by Grant Thornton in partnership with Retail Economics, assesses the impact of the cost-of-living crisis on retail & consumer industries. Analysis covers the key drivers and trends underpinning shifts in consumer behaviour in response to high inflation and the potential impacts for businesses as households cut back their spending.

Full report is available for download here.

Research methodology

The research contains behavioural insights based on findings from a nationally representative consumer panel of UK households. The sample comprised more than 2,000 adults with survey data collected in May 2023. Economic modelling of the impact of the cost-of-living crisis on UK households is based on the latest Bank of England forecasts and Retail Economics estimates. Data refers to the financial year April 2023 to April 2024 unless otherwise stated.