Technology insights: Winter 2023

What can we expect from tech?

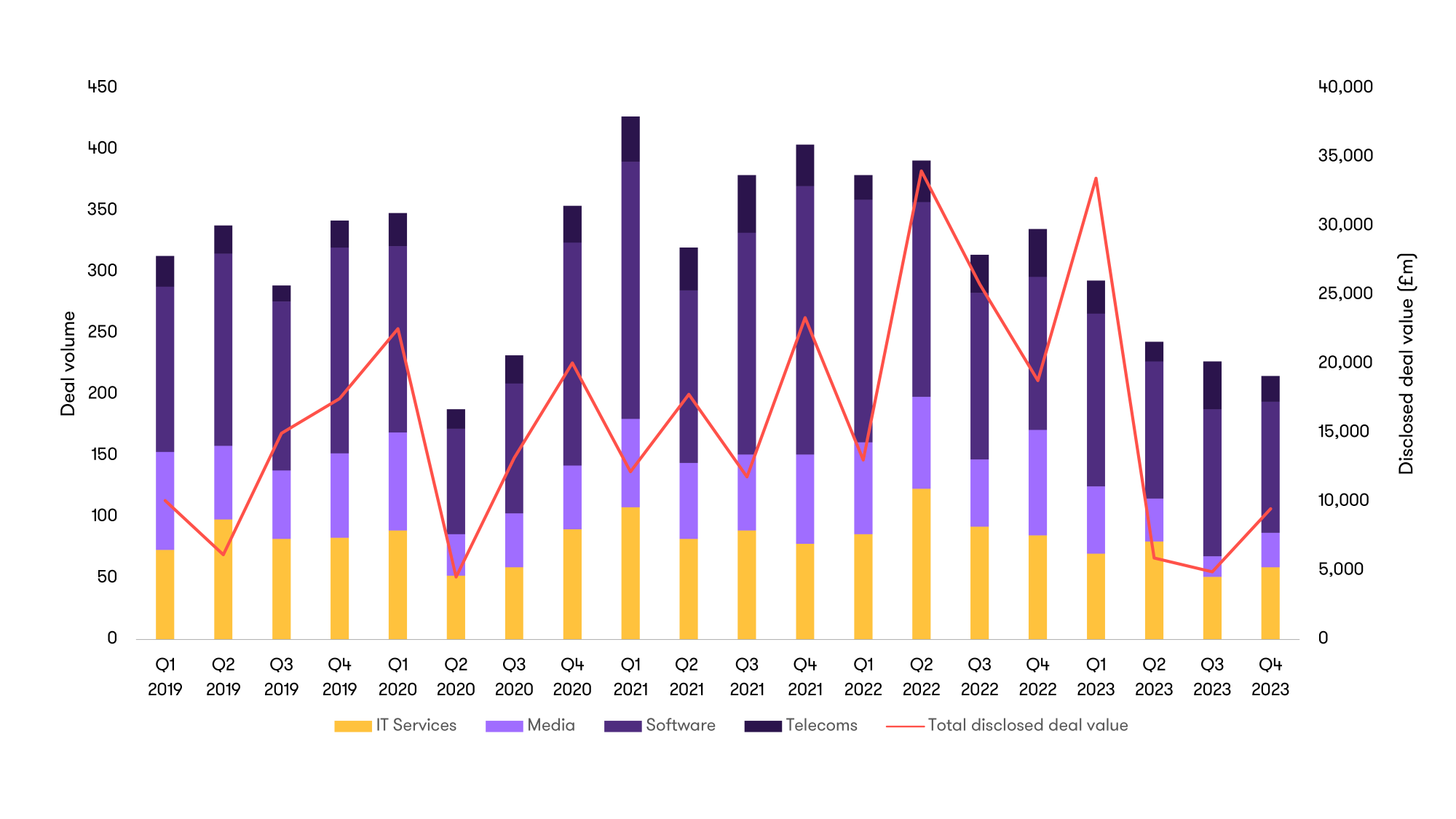

Compared to the previous quarter, the UK TMT M&A landscape in Q4 2023 showcased a more resilient performance. Deal volumes were still down, but only by 5.3%, with a notable surge in total deal value, which was up 93% (albeit somewhat skewed by Blackstone’s announced £2 billion acquisition of Civica). In the same period primary private equity (PE) activity subsided from 16% to 9% of total deals, while trade buyer activity also dropped from 61% to 53%, with a resurgence in PE-backed trade bolt-on deals making up the balance. These shifts underscore the prevailing market dynamics that distinctly favour cash-rich strategic trade or PE-backed trade, capable of executing swift transactions without reliance on the currently expensive debt markets.

Story of 2023 – deal activity bottoms out

2023 saw overall transaction momentum decelerate after two exceptionally strong years, accompanied by a material downturn in TMT deal activity as the cost of capital increased and growth became harder to find in a 'risk off' environment. Both deal values (-41%) and volumes (-30%) experienced a sharp drop, brought on by broader macroeconomic uncertainties and a shift towards a higher interest rate environment, making liquidity harder to come by as well as more costly. It's been a tough ride with deal volumes declining in five of the last six quarters, but it feels like we may have reached the bottom of the cycle. The latter half of the year hints at a potential confidence boost for deals with more positive sentiment as we transition into 2024.

2024 outlook – reason for optimism

The principal driver of optimism for the forthcoming 12 months has been the consensus that inflation is moving inexorably downwards, with an expectation of accompanying interest rate reductions commencing earlier in the year, and going deeper than previously anticipated. However, the macro-view is both fragile and volatile. The impact of elections in both the UK and US may well be poised to invigorate markets, drawing parallels with the positive trends seen in previous political campaign years. However, the persistent threat of geopolitical tensions looms large, and supply chain disruptions could rapidly unwind abating inflationary pressures, potentially hindering a full resurgence in cross-border M&A.

PE-investment activity is expected to rise, propelled by untapped funds and pent-up demand. We also anticipate a continued surge in PE-interest in pivotal subsectors, such as digital transformation, cybersecurity, and high-growth software, which are set to provide considerable investment opportunity over the medium to long term.

It remains to be seen if the IPO market will regain strength and reemerge as a more viable exit strategy for investors once again, offering companies the opportunity to raise capital in a potentially more favourable market environment. The challenges for UK public markets as a destination for technology stocks remain acute.

A closer look at the deal stats

Quarterly M&A deal activity

TMT M&A activity decelerated significantly in 2023 due to an environment predominantly characterised by heightened risk aversion and a shift towards more cautious corporate strategies in response to increased capital costs and economic uncertainty. Consequently, a greater proportion of potential acquirers tended to direct their attention towards organic growth and bolstering profitability, concentrating on consolidating current market positions rather than venturing into new markets. In addition to the decrease in deal volume, the overall value of transactions remained below recent historical averages, reinforcing the trend towards a more circumspect approach to M&A.

In Q4 2023 the total number of deals fell, down 5.3% versus Q3 2023, and a 36% fall versus Q4 2022. However, the rate of decrease in transactions began to plateau in the final quarter, which may be a sign of a turnaround, further supported by an increase in total deal value. The Blackstone / Civica deal and Leonard Green & Partners investment in Iris Software, a £3.15 billion deal announced just as the year drew to a close, provided a welcome re-affirmation that mega deals in software are beginning to return.

|

Total |

Total |

IT Services |

Media |

Software |

Telecoms |

|

No of deals |

215 |

59 |

28 |

107 |

21 |

|

QoQ % change |

-5.3 |

+15.7 |

+64.7 |

-10.8 |

-46.2 |

|

YoY % change |

-36.0 |

-30.6 |

-67.4 |

-14.4 |

-46.2 |

Looking across our key subsectors, media experienced the most significant increase in the quarterly number of deals (+64.7%), including Keywords Studio’s acquisition of The Multiplayer Group; followed by IT services with a more modest 15.7% increase: Wavenet’s acquisition of security services platform, Falanx Cyber, and Kick ICT’s acquisition of Microsoft Dynamics specialist, C2 Software. Conversely, the quarterly volume of deals in both telecoms (- 46.2%) and software (-10.8%) saw decreases. While all sectors were down across the year, much of this was a result of the drop off in activity over H1, and the flattening downward curve gives some cause for optimism in 2024.

Despite the softening of quarterly deal volume activity in telecoms, it should be noted that this came off a Q3 peak, driven by significant consolidation in the Altnet arena, as assets showing less financial strength (due to more expensive capex obligations) were consolidated. Examples of stronger performers include Gigaclear, which recently raised £1.5 billion from a banking consortium to support its substantial FTTP roll out plans and further bolt-on acquisitions. We anticipate that smaller, cash-strapped Altnets will continue to present acquisition opportunities for more scaled and better capitalised players in 2024.

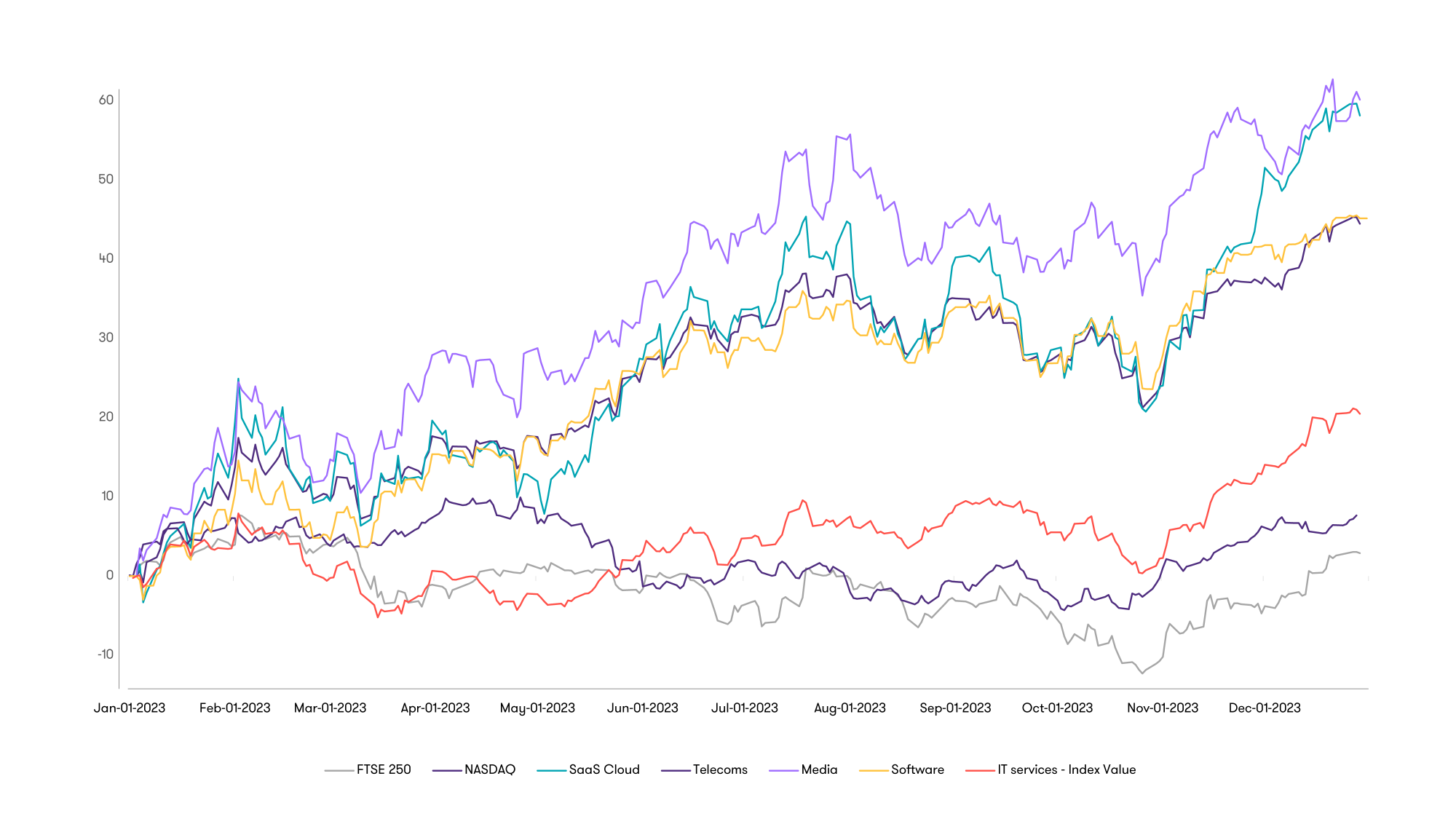

Public markets gaining momentum

Despite a slow start, Q4 saw an inflection point in November, with share prices across TMT stocks rapidly moving towards yearly highs. The SaaS Cloud index stood out, showing the sharpest uplift in share price with a 29.6% increase vs. Q3.

The most significant driver behind this resurgence is the hope that peak inflation, and thus interest rates, are behind us, with commodity prices now stabilised and the global supply chain beginning to flow along more efficiently (albeit the disruption in the Red Sea has now dampened some expectation and investors should stay vigilant). However, hopes on either side of the Atlantic are rising given both the Federal Reserve and the Bank of England have a higher expectation of being able to engineer a ‘soft landing’ scenario. This could lead to both continued economic strength as well as a more conducive labour market, giving buyers further impetus to start considering more transformative transactions again.

Listed company share price performance by sector: 2023

|

Total |

FTSE 250 |

NASDAQ |

SaaS Cloud |

Telecoms |

Media |

Software |

IT services |

|

|

QoQ % change |

+7.4 |

+17.3 |

+29.6 |

+9.7 |

+20.3 |

+18.3 |

+15.0 |

|

|

YoY % change |

+2.9 |

+44.5 |

+58.2 |

+7.7 |

+60.2 |

+45.2 |

+20.5 |

Q4 2023 saw a strong rally in public valuations across all indices. SaaS Cloud had the most significant quarterly increase (+29.6%), as investors and buyers gain comfort from highly visible and scalable revenue streams, followed by IT services (+15%) and software (+18.3%). Media also performed well over the quarter closing up 20.3%.

Looking at the broader picture in 2023, software and SaaS Cloud moved in tandem, showing consistent growth across the year. The media sector performed strongly, and although coming from a low base, closing 2023 up 60.2% overall. IT services had a slow start, but gained momentum towards the year end, making the most of the Santa Rally. Telecoms valuations were remarkably flat over the course of the year, showing very little change and epitomising stability in a year marked by bouts of volatility across other sectors.

Software listed-peer group performance

|

EV / Sales multiple |

SaaS Cloud |

Software |

|

Quarter end valuation |

8.1x |

8.0x |

|

5 year average |

12.4x |

8.15x |

|

QoQ % change |

+19.1 |

+11.6 |

|

YoY % change |

+37.1 |

+31.1 |

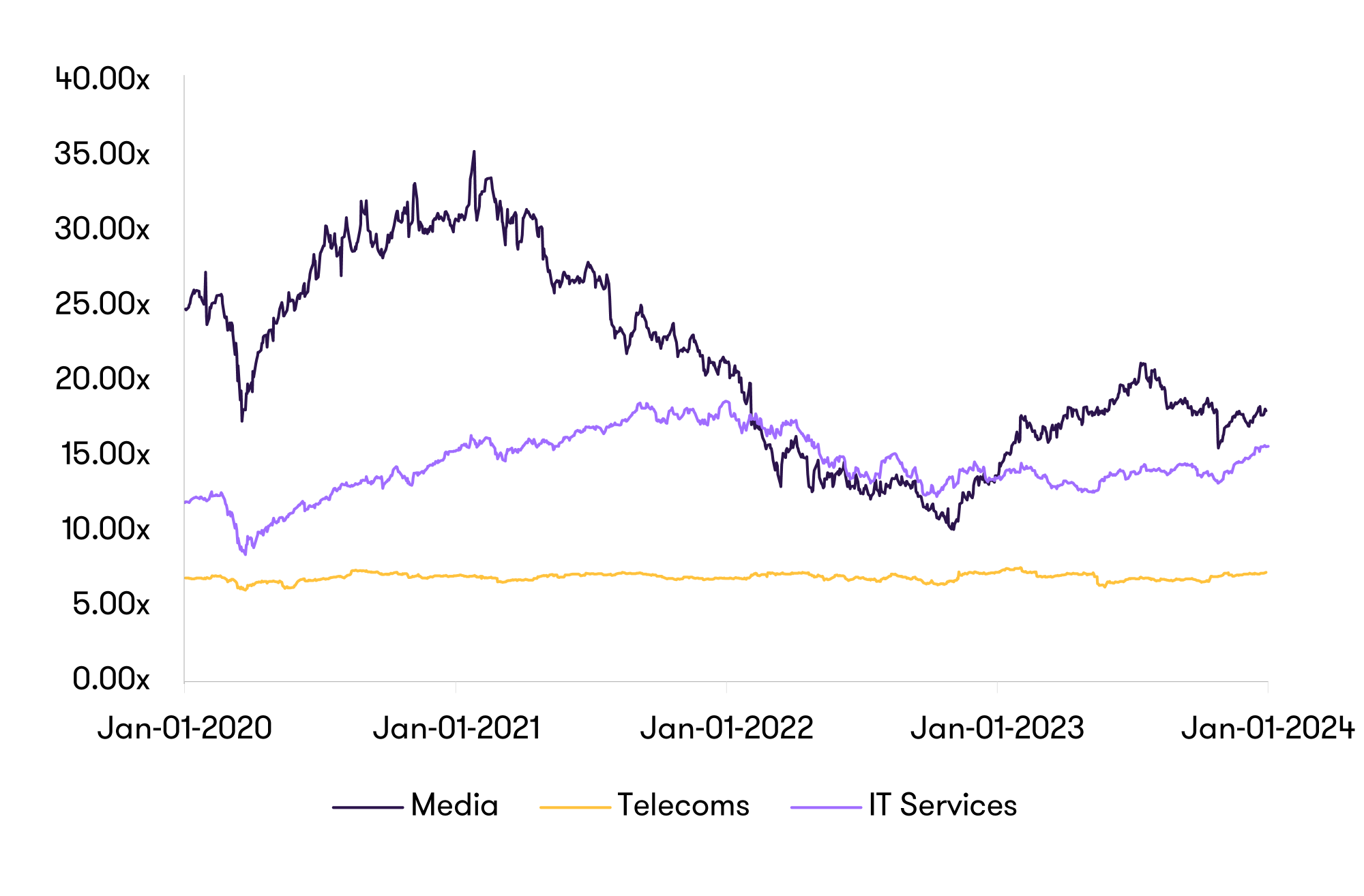

Media, telecoms, and IT services listed peer group performance

|

EV / EBITDA multiple |

IT Services |

Media |

Telecoms |

|

Quarter end valuation |

15.6x |

18.0x |

7.3x |

|

5 year average |

14.5x |

21.4x |

7.0x |

|

QoQ % change |

+13.6 |

+0.4 |

+8.2 |

|

YoY % change |

+15.5 |

+31.5 |

-0.1 |

Valuations in the private company M&A market

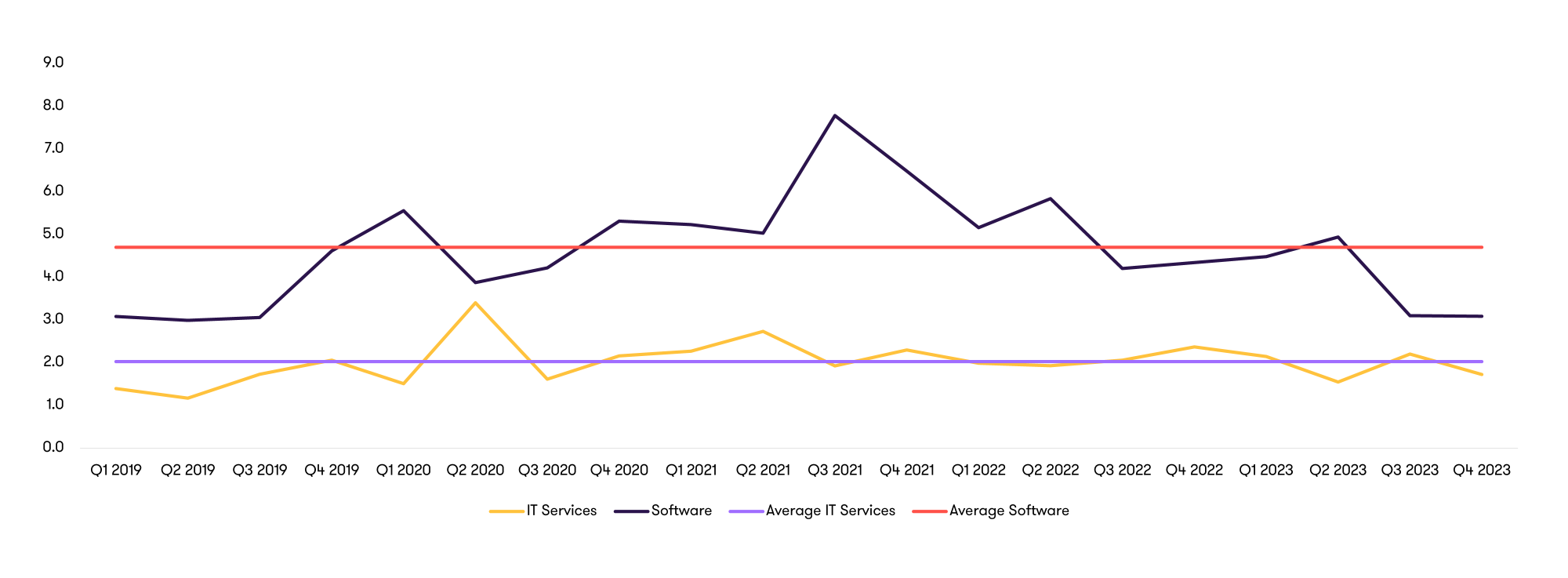

The picture for M&A valuations was more mixed in Q4 in the UK. The IT services sector experienced a decrease in average deal multiples, dropping from 2.2x to 1.7x EV/Revenue. In the software sector valuations remained steady at an average 3.1x EV/Revenue, still notably below the five-year average of 4.7x. The key question for investors is whether this is the new normal, or whether we'll see valuation multiples expand as interest rates fall. The current reality reflects a more disciplined approach to pricing by strategic acquirers across the sector, and while the premium valuations of 2021 and 2022 can still be found, these are for the very top tier assets with a fundamentally compelling strategic fit; growth profile; profitability and strong synergy potential.

EV/Sales multiples for software and IT services companies

|

EV/Sales multiple |

Software |

IT services |

|

Quarterly end valuation |

3.1x |

1.7x |

|

5 year average |

4.7x |

2.0x |

|

Quarterly change |

0.0x |

-0.5x |

|

YoY change |

-1.2x |

-0.7x |

Private equity

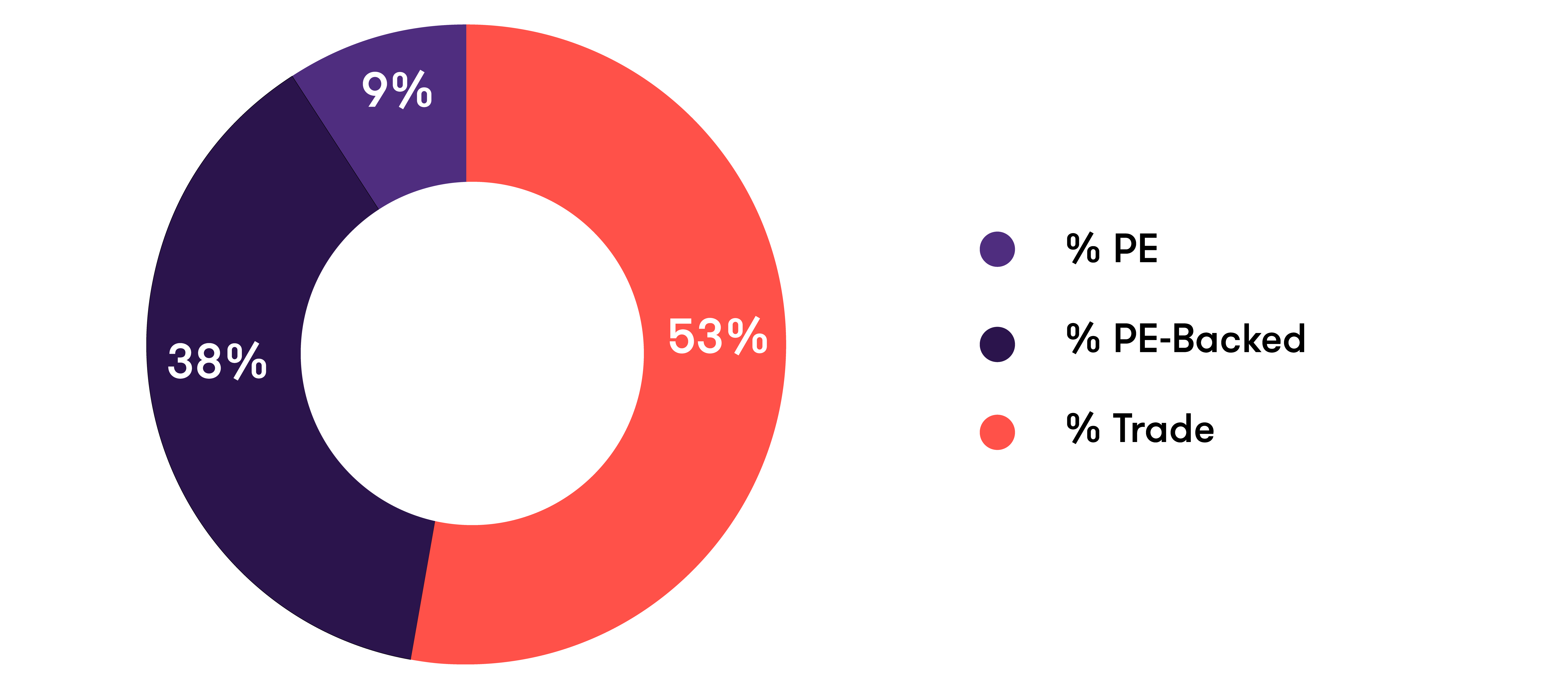

The split of deals by investor type saw new PE-deals experience a drop off from 16% to 9% of the overall mix in the quarter. Trade acquirers still remained the dominant deal channel, though declining from 61% of deals in Q3 to 53%. The real mover was PE-backed trade acquirers, which stepped up to represent 38% of total deal flow.

This reflects the focus on deal certainty and deliverability for vendors, and the more resilient nature of deals in the lower mid-market where bolt-on transactions and buy and build platforms are a dominant force. While bolt-on acquisitions for existing platforms are now more expensive as costs of debt have stepped up, it remains one of the most proven routes to value creation for PE. Investing further in a proven platform asset with a strong management team and track record of execution is a far easier investment case than a new deal in a more nervous and risk-averse PE market.

Top five PE-investments in Q4 2023

Spotlight on cybersecurity across 2023

Highlighted transactions

Nov 2023: MMC Ventures invested in a Series A round for security infrastructure software provider, Cloudsmith

Aug 2023: Francisco Partners undertake a public to private of Blancco Technology Group, a provider of mobile device diagnostics and secure data erasure solutions

Jun 2023: Security consulting vendor, Logiq Consulting received investment from Phoenix Equity Partners

The US continued to lead in the number of cybersecurity M&A deals, followed by the UK, with Sweden also emerging as a significant player in the first half of 2023, surpassing Canada and Germany. Despite the continued dominance of the US and Europe, there was also a noticeable uptick in deals involving companies from Israel, India, the UAE, and Singapore, truly underpinning the global nature of the cybersecurity arena.

PE firms continued to be proactive in this space, with significant deals, such as Thoma Bravo's acquisition of Magnet Forensics for USD 1.3 billion, Francisco Partners' acquisition of Sumo Logic for $1.7 billion, and Crosspoint Capital Partners' acquisition of Absolute Software for USD 870 million.

In addition to a prolific number of M&A deals, there were also a number of notable partnerships and investments in cybersecurity companies. For example, Siemens partnered with cybersecurity software company Awen Collective, to develop a new, accessible, and affordable managed IT security solution for SME manufacturers.

Key TMT deals in Q4 2023

How we helped

- Acquisition of recruitment software and services provider, Blue Octopus, by Iris Software

- Sale of sustainability certification solutions platform Planet Mark to Alcumus, backed by Apax Partners

- Sale of CareTech software platform Oysta Technologies, to the Access Group

- Acquisition of digital road management platform, One.Network from Bridgepoint Capital, by Causeway

- Acquisition of cyber security services platform, NetSecure, by Integrity 360

- Sale of field service management software provider, Joblogic, to Axiom Equity

- Acquisition of brand solutions specialist, Uncommon Creative Studio, by Havas

- Sale of Nowcomm, a Cisco managed services platform, to Palatine backed FourNet

- Sale of TigerTMS, a provider of core connectivity and management solutions trusted by the leading hotel brands, to Valsoft

- MBO of The Barrister Group, a legal solutions vendor enabling barristers to choose to work remotely, by Lloyds Development Capital

- Sale of Horsefly Analytics, a provider of labour market data and talent analytics also to Lloyds Development Capital, in an MBO

- Acquisition of IT managed services platform, Vital Technology Group, by Air IT

- Acquisition of assistive technology provider, Svensk Talteknologi AB, by Texthelp

- Acquisition of workload management software provider, Depotnet, by Everfield

- Acquisition of local authority software provider, Farthest Gate, by StarTraq, backed by August Equity

- Acquisition of digital engineering solutions provider, Nimble, by SCC

For more insight and guidance, get in touch with Andy Morgan.