Technology Review Q2 2023

What can we expect from tech?

The UK TMT sector continues to battle wider macroeconomic pressures. Base rates are now predicted to hit 6.5% into next year and remain high for a lot longer than expected. This negative sentiment is seeping into M&A deal volumes: 17% down on Q1 2023 and 40% down on the Q2 2022 comparator when the deal market was booming. This is the lowest quarter for M&A volume since the pandemic impacted Q3 2020, and at the halfway point in the year sees deal activity running a cumulative 30% behind 2022.

Total completed deal value in the sector painted an even gloomier picture, as we tracked £5.7 billion worth of deals in the quarter, a massive 83% down on Q2 2022. It's clear the large deal market has been most impacted by the cost of debt and the relative lack of liquidity to support transformational M&A. This is a market-wide reality, not just impacting TMT as Refinitiv reported global M&A deal value down by 36% in Q2 2023 to USD 732.8 billion.

Trend towards digital keeping TMT buoyant

The TMT sector remains best placed to weather this storm, however, as the underlying demand for digital transformation and technological advancement remains a key priority for company CEOs. There are also some exciting hotspots within the sector which continue to drive deal flow and investment, while the battleground for UK TMT M&A remains the mid-market where activity continues to be more resilient. Shortly after the April 2023 investment in intelligence platform provider Quantexa, AI-powered no-code app development platform builder.AI raised USD 250 million in a series D led by the Qatar Investment Authority. After a tough few years for the venture capital market we're seeing some signs of a resurgence, with chunky backing being drawn to the strongest prospects in the hottest areas of the market.

Technology share price performances have outperformed flatlining markets since the beginning of the year, particularly driven by tech stocks in the US where economic indicators have been more encouraging. The massive Biden investment plan continues to fuel expectations that inflation can be brought under control without the economy falling into a full-scale recession, and the technology market is one of the big beneficiaries as digital investment ramps up. TMT M&A deal volumes have lagged the cycle of public market valuations, only tracking downwards some six months after publicly listed tech stocks started to feel the heat of rising interest rates and a shift in sentiment away from growth stocks. So, the strong share price performance for tech stocks in the first half gives encouragement to the view that we could see a rebound in M&A activity in H2 2023 and into 2024.

While the overall picture for 2023 to date undoubtedly isn’t the most encouraging – and the sharpness of the drop off in UK deal volumes in Q2 is certainly a cause for concern – the combination of a pick up in large venture capital investment activity, stronger share price performance, and the continuing pace of digitisation of the economy gives us confidence that the sector is poised for a recovery. With a general election due to be called before 17 December 2024, we can expect this to be on the mind of owner-managers as they consider their options for the next year.

A closer look at deal activity

The total number of deals continued its downward trend since the peak in Q2 2022, dropping a further 17% against Q1 2023 and a more significant 40% below this time last year. The accelerating pace of the decline is a concern. With deal volumes in the half year now running a cumulative 30% behind 2023 isn't going to be a vintage year for UK TMT M&A.

However, it's worth reflecting on the extraordinary market we've seen over the last two years. This year's deal levels, even with the marked drop off, are still comparable with where we were in 2019, with the prospect of some recovery in the second half. The challenges of increased costs of capital and reduced liquidity are taking time to feed through into amended valuation expectations, and dealmaking is requiring creativity, commitment, and more time.

The bright spots in M&A activity over the quarter were within IT services, as consulting continues to be very active attracting increasing levels of PE-investment, and managed services consolidation continues apace as platform businesses look to move up the stack by bolstering their cyber and data capabilities

| Total | Software | IT services | Media | Telecoms | |

|---|---|---|---|---|---|

| No of deals | 243 | 112 | 80 | 35 | 16 |

| QoQ % change | -17.0 | -20.6 | +14.2 | -36.3 | -40.1 |

| YoY % change | -40.0 | -29.6 | -35.0 | -53.3 | -52.9 |

Depressed M&A market conditions countered by a strong half for share prices

Technology share price performances have continued their excellent run since the start of 2023 defying the somewhat depressed conditions within the TMT M&A market. The software, SaaS Cloud and NASDAQ indexes are now all up over 30% since the start of the year, spurred on by improved global confidence and a significant drop in inflation in the US. The media sector is also now receiving more investor attention after a tough couple of years post-pandemic, with the media index up almost 42% since the start of the year, albeit from a low base with the five-year growth only scraping in at 6.1%. This contrasts the muted performance we've seen across IT services, telecoms, and the UK-focused FTSE 250 index.

| Media | Software | SaaS Cloud | NASDAQ | FTSE 250 | IT services | Telecoms | |

|---|---|---|---|---|---|---|---|

| Quarterly change (%) | +10.9 | 16.5 | +13.2 | +13.1 | -2.5 | +4.2 | -7.3 |

| YTD change (%) | +41.7 | +37.4 | +34.0 | +32.7 | -3.8 | +4.7 |

-0.61 |

| Five-year change (%) | +6.1 | +16.8 | +20.1 | -9.3 | -34.1 | -22.1 | -11.7 |

Valuations in the public markets

The low point for valuation multiples in the market was at the end of May 2022 and we've seen a slow and steady recovery since then. We're not expecting any dramatic return to 2021 peaks any time soon. It'll need a robust period of stronger economic fundamentals and reductions in interest rates to kickstart markets. With risk-free returns on short dated government bonds now 4.6% (Ycharts), there's been a fundamental repricing and investors are struggling to see the potential for market premium over and above the perceived market risk. The areas of strongest share price performance in the year, such as media stocks, are reflective of a recovery from historic lows and a return to longer term averages rather than a sign of a significant return of investor confidence or step-up in valuation fundamentals.

| EV/Sales multiple | SaaS cloud | Software |

|---|---|---|

| Quarter-end valuation | 7.4 | 7.2 |

| Five-year average | 12.5 | 7.3 |

| Quarterly change | -0.9x | +0.7x |

| YoY change | +0.2x | +0.7x |

| EV/EBITDA multiple | Media | Telecoms | IT services |

|---|---|---|---|

| Quarterly end | 20.0x | 6.8x | 14x |

| Five-year average | 22.3x | 6.9x | 13.9x |

| Quarterly change | +2x | -0.2x | +1.2x |

| YoY change |

+7.3x |

0x | +0.3x |

Valuations in the private M&A market

Software and IT services deals within the private M&A market continue to converge towards their five-year averages. We're seeing an interesting divergence between software and IT services valuations in a similar manner to public markets at the moment. The average software multiple showed some recovery in Q2, increasing to 4.9xEV / Sales getting it back above its five-year average after quite a substantial drop from the 2021 peaks. Average IT services valuations exhibited a steeper decline, falling below its five-year average to 2x.

| EV/Sales multiple | Software | Services |

|---|---|---|

| Quarterly-end valuation | 4.9x | 1.5x |

| Five-year average | 4.8x | 2x |

| Quarterly change | +0.4x | -0.7x |

| YoY change | -0.9x | -0.4x |

Private equity

The environment is certainly a lot tougher for PE than it was 12 months ago. The days of cheap leverage are over and we're starting to see PE-hold periods extending. Many PE-assets are holding off going to market at the moment as they wait for M&A market conditions to improve. There were only two notable SBO deals in Q2 2023 compared with eight in Q1 2023 and nine in Q2 2022. PE-deal volumes overall are down 25% in H1 2023 compared with H2 2023. We saw 59% of deals completed in the quarter being from trade acquirers, the highest level we have seen for some time. Cash-rich trade acquirers are looking increasingly attractive to vendors relative to the execution risk that's often associated with a PE-transaction.

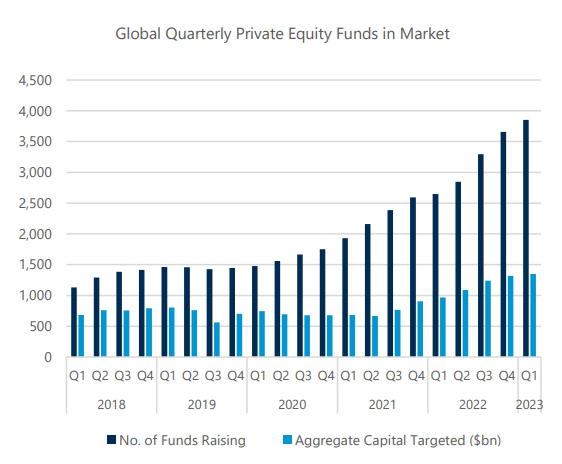

The fundraising environment for PE has become a lot tougher. While it continues to maintain its attractiveness as an asset-class, the challenges of capital allocation amid high levels of market volatility is making the journey to raising a new fund tortuous for many. There's some evidence of follow-on funds being raised to help with extending hold periods amid more challenging exit conditions. A huge amount of dry powder still remains, however, as seen in the chart here, and for those who have patient capital and an ability to invest across a broader range of transaction sizes and structures there remains an opportunity to capitalise.

View from a June 2023 Private Equity Wire survey

Most respondents (55%) said they expect fundraising to decline in 2023, far more than 6% in 2022, while the proportion of respondents who are unsure whether they will raise new funds increased to 30% in 2023 from 20% in 2022. As investing confidence deteriorates, the number of professionals who believe investment opportunities are increasing has declined substantially, to 41% from 67%.

Source: Paul Weiss

Top five PE investments in the quarter

AI talk isn’t going anywhere

AI continues to steal the headlines as businesses globally work out how to integrate it into products, as well as improving worker productivity. Mckinsey & Company estimate that AI could have a USD 7 trillion incremental economic impact through improved worker productivity. This is also backed up within the UK through the Google Economic Impact Report, which estimates that AI has the potential to drive a £400 billion boost to the UK’s economy by 2030 and could save the average UK worker more than 100 hours annually.

A recent study from techUK and Capital Economics showed that within the private sector, 90% of large organisations have already implemented AI or actively planned adoption against 49% for SMEs. In terms of sectors, in the UK, the telecommunications sector and legal sector have the highest adoptions rates, with hospitality, health and retail having the lowest. While there hasn’t been a huge amount of M&A in AI to talk about yet, we expect this to increase in the next 18 months as businesses face the battle to acquire AI capabilities as fast as possible. As use cases become more complex, it's often quicker and potentially cheaper to buy than build it yourself.

Spotlight on consulting

- Objectivity acquired by Accenture

- Leading Resolutions MBO by NVM Private Equity

- Hedgehog lab investment by BGF

The IT consulting sector continued its momentum from Q1 2023 as there were a number of large interesting deals in the sector from trade and PE-buyers. IT consulting-assets remain an interesting prospect for the high margins and growth opportunities among the continued digital transformation drivers. There's been particular interest around product-led consultancies, as ServiceNow partners Whyaye and CloudStratex were both acquired in the quarter. The ServiceNow eco-system is growing fast after we've seen strong growth over the years for other eco-systems, including Microsoft and SAP.

Spotlight on human capital management

- PSSG acquired Essential Payroll

- Ciphr acquired Marshall e-learning

- Veritone acquired Broadbean>

This quarter was a particularly active one for M&A deals in the human capital management sector, with over 15 deals recorded. The standout was Edenred acquiring Reward Gateway in a £1.15 billion deal bringing together employee benefits solutions and employee connectedness solutions under the Edenred banner. Another interesting deal was the carve out of Saville Assessment, a talent assessment platform, by Tenzing from Willis Towers Watson, showcasing PE increasing interest in this part of the market, following shortly after LDC's investments into Talos 360 and Horsefly earlier in the year.

Key TMT deals in Q2 2023

Grant Thornton deals in Q2 2023

- Advising BCN group on its acquisition of MSP and Microsoft solutions partner, CMI

- Advising GCP-backed digital transformation specialist HippoDigital on its acquisition of data consultancy The Data Shed

- Advising Toluna on its acquisition of global market research company MetrixLab B.V

- Advising Integrity360 on its acquisition of cyber security service provider Netsecure

- Advising Baird Capital on its investment into payments business FreemarketFX

For more insight and guidance, get in touch with Andy Morgan.

![]()