Technology insights Q1 2023

What can we expect from tech?

It never seems to be an uneventful quarter in the world of TMT M&A. After weathering the extreme gyrations of UK politics and economic policy in Q4 2022, the first quarter of 2023 saw UK tech wrestling with the fallout from the failure of Silicon Valley Bank. This put a lot of UK tech businesses at risk, particularly in the early-stage and high-growth segments. But after a highly charged and nervous few days, a deal was brokered with HSBC, bringing huge sighs of relief all round. The long-term implications for UK tech financing remain to be seen, but it has focused many on reassessing their funding and investment strategy in the context of ongoing uncertainty in the macroeconomic environment, and the impact of prolonged inflation and interest rate rises.

Are we at a turning point?

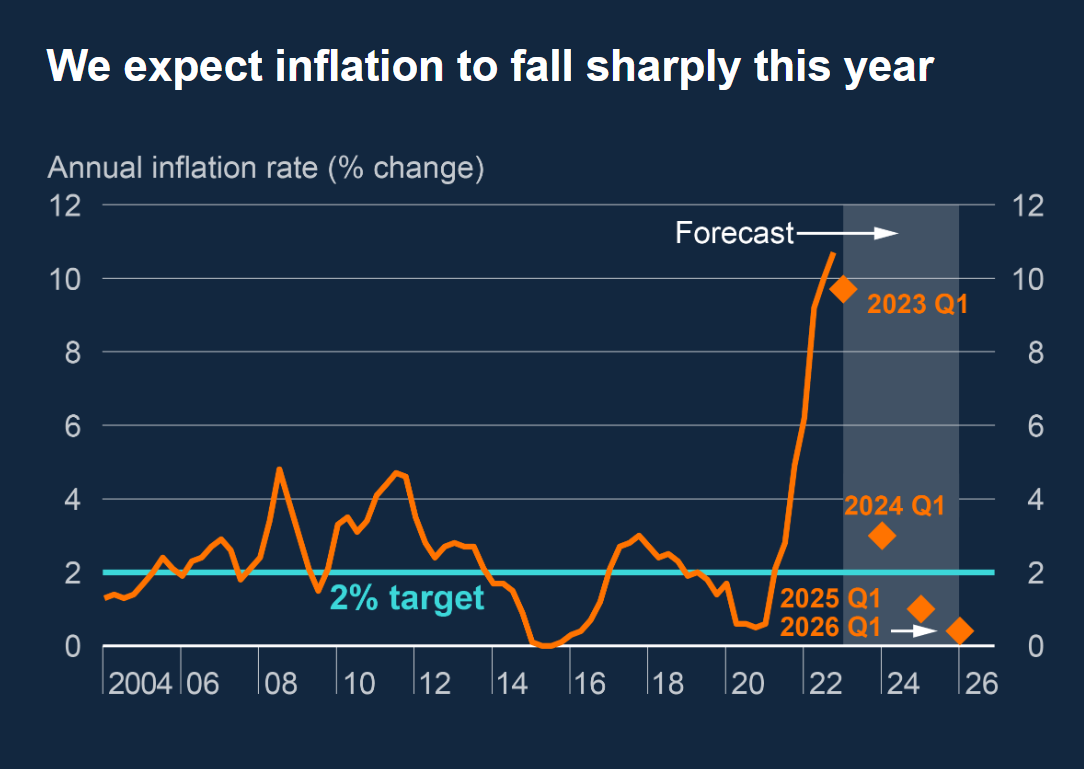

This uncertainty and volatility has started to seep into financial performance. Growth is harder to come by and early warning signs, in the form of profit warnings, are becoming more frequent in the listed tech market as cost pressures, project delays and credit tightening start to bite. It feels like an inflection point, but the direction of travel isn't clear cut. Signs of increasing business confidence, backed by forecasts of inflation falling sharply at the back end of the year and the potential to avoid a technical economic recession, are set against a continued tight labour market and skills shortages in key areas.

While the bar is increasingly high for corporate and consumer technology spending, the underlying drivers for digital transformation are robust and immediate. The UK TMT M&A market is predominantly mid-market in nature, and this continues to remain resilient with strong deal flow and plenty of private equity (PE) money still being invested into quality tech businesses. The UK remains at the heart of European unicorn creation, with the recent £104 million raise by AI and data analytics specialist Quantexa at a £1.5 billion valuation being the latest and first of 2023. The ability of the UK tech sector to deliver long-term returns remains robust.

Dealmaking motivation remains high

The data still paints a slightly gloomy but improving picture in the public markets, with valuations a way off their post-pandemic averages. But there's been a notable uptick across the quarter with nearly all market segments up, some materially, from their end-of-year lows. Deal volumes got off to a slow start with levels 8% off the 'Trussonomics'-impacted Q4 2022 and 19% off Q1 2022.

However, share prices have started 2023 in a positive manner and the TMT UK mid-market has remained shielded from a lot of the global macroeconomic events with private valuations still strong. PE is also still as prominent as ever with high levels of dry powder still to deploy, but the focus on margin expansion, cash generation and a clear route to profitability is increasingly key rather than pure revenue growth.

We expect an improving picture for deal volumes as we head into H2 2023, as confidence levels in both public and private markets improve, inflationary pressures start to taper off, and liquidity in debt markets settles down. With a general election due to be called before 17 December 2024, the motivation for deals from entrepreneurs and owner-managers will remain high and provide a strong underpin to levels of activity.

Improving macroeconomic drivers for deals in H2?

The Bank of England (BoE) still anticipate an increasing degree of economic slack – alongside falling external pressures – to lead CPI inflation to decline to below the 2% target in the medium term. While inflation appears to have peaked, the CPI index is so far remaining stubbornly high with headline rates only easing from 11.1% in October 2022 to 10.1% in March 2023 – materially ahead of levels being experienced by most developed economies. A clearer trend line tracking the BoE forecasts will undoubtedly be helpful in limiting the potential for further interest rate increases, and boost confidence for dealmaking in the sector.

Source: Bank of England, February 2023

More challenging demand conditions have brought an increasing number of profit warnings in the US and the UK. Increasing costs, project deferrals, sales shortfalls, credit tightening and weak consumer confidence are now starting to feed through into financial performance. This has been felt across the economy, but the technology sector has not been immune. The UK has seen warnings from a handful of leading sector players, including NCC Group and GBG in the quarter.

US profit warnings by sector Q1 2023

Source: Factset

Deal statistics

The total number of deals was down on the previous quarter and is nearly 20% off a strong Q1 2022 comparative. While that is a step back from the heady heights of 2021 activity levels, the market is progressively improving following the marked slow down at the turn of the year. The real bright spot in the deal stats has been in software, where deal activity increased 19% after four consecutive quarterly falls. We tracked £25 billion of corporate activity across the four sub-sectors – still the third highest quarter by value since 2019.

| Key stats | Total | Software | IT Services | Media | Telecoms |

|---|---|---|---|---|---|

| No of deals | 320 | 150 | 74 | 53 | 43 |

| QoQ % change | -8% | +19% | -19% | -39% | 0% |

| YoY % change | -19% | -25% | -18% | +32% | +79% |

Share price performance

The markets were tough for technology investors in 2022, with the SaaS cloud and software indexes both down 29% as the impact of increasing interest rates and the switch in sentiment away from high growth potential stocks took hold. However, Q1 2023 paints an improving story with all the indices apart from the FTSE 250 in positive territory, and with material gains in the SaaS cloud index (+20%) and Media index (+27%).

| FTSE 250 | SaaS cloud | Nasdaq | Software | Media | IT services | Telecoms | Telecoms | |

|---|---|---|---|---|---|---|---|---|

| Quarterly change | -1% | +20% | +18% | +15% | +27% | +1% | +7% | 43 |

| YoY change | -11% | +29% | -14% | -29% | -5% | -21% | -8% | 0% |

| 5 year change | -3% | +67% | +69% | +98% | +3% | +33% | -10% | 79% |

Valuations

Valuations appear to have bottomed out in public markets. The SaaS cloud index, software index and media index had relatively strong quarters with valuation multiples rising across the board by around one turn of revenue multiple. However, IT services and telecoms multiples were flat in the quarter.

| EV / Sales multiple | SaaS Cloud | Software | Media |

|---|---|---|---|

| Quarter end valuation | 7x | 6.6x | 4.7x |

| 5 year average | 12.7x | 7.3x | 7.4x |

| Quarterly change | + 1.1x | + 0.7x | + 1.1x |

| YoY change | -1.4x | -4.6x | -0.2x |

| EV / EBITDA multiple | IT services | Telecoms |

|---|---|---|

| Quarter end valuation | 13.4x | 7.0x |

| 5 year average | 13.6x | 6.9x |

| Quarterly change | -0.2x | -0.1x |

| YoY change | -3.9x | -0.2x |

M&A valuation: converging to medium term average levels?

In private company M&A, valuations continue to hold up more robustly, but there is a clear convergence to medium-term average multiples. While premium valuation deals are still out there, a notable shift has taken place in favour of profitable software businesses and away from high-burn, high-growth models with a more challenging route to cash EBITDA positive.

| EV / EBITDA multiple | Telecoms | IT services |

|---|---|---|

| Quarter end valuation | 14x | 15.9x |

| 5 year average | 14.2x | 14.8x |

| Quarterly change | -8.7x | -4.1x |

| YoY change | -4.9x | -0.3x |

| EV / Sales multiple | Software | Media |

|---|---|---|

| Quarter end valuation | 4.3x | 2.2x * |

| 5 year average | 4.7x | 2x |

| Quarterly change | +0.3x | -1.1x |

| YoY change | -0.5x | -0.8x |

* No disclosed deal values for media sector in Q1 2023, so calculated using average of last four quarters

Private equity

PE and PE-backed businesses continue to remain a significant player in M&A activity across the sector. The percentage of deals involving PE was flat on Q4 2022, still six percentage points down compared to the five-year average. We've seen a very strong couple of years for PE, so we fully expected a quieter 2023 for PE exits as funds take stock of balancing growth potential with trickier market and debt conditions. There remains a strong focus for PE on deploying capital through existing buy-and-build platforms, with new platform deals proving more challenging.

What isn’t in doubt is the appetite across PE for tech assets, as evidenced by the recent survey from Private Equity Wire setting out priorities for PE investment in 2023.

Survey on which UK sector is most attractive for PE in 2023

Source: Private Equity Wire survey, March 2023

Q1 notable deals

![conversation icon]() Spotlight on consulting

Spotlight on consulting

Q1 2023 has been a particularly impressive quarter for consultancies with a number of notable deals in the UK market, the majority involving PE. The strong market drivers for digital transformation and the ever-increasing demand for cyber and security skills have created significant opportunities for growth for independent, specialist consultancies. Despite pure contracted revenues typically lower than in other managed service businesses, PE is attracted to the ability to scale, regulatory drivers of demand and the high margin potential. The need for specialist third-party expertise as corporates adapt to stay ahead of the curve in integrating technologies like AI into systems and processes is strong.

Notable consultancy deals in Q1 2023:

- CBPE capital/LDC investment into FSP

- GCP investment into 101 ways

- Cognizant acquisition of Mobica and Version 1 acquiring 2 tech consultancies

![120x120-artificial-intelligence-icon]() Spotlight on consulting

Spotlight on consulting

AI continues to make the headlines in 2023 with Chat GPT reaching one million users in five days (compared to 3.5 years for Netflix). All the big tech giants are jumping on the AI bandwagon. Microsoft's announced integration of ChatGPT into its Microsoft Office products later this year has also sparked talks of an AI bot from the likes of Google, Facebook and Tesla. Within the UK mid-market, we've seen particular themes around conversational AI, AI-focused cyber and AI-focused recruitment. It'll be interesting to see how UK firms commercialise AI into products and services.

Notable AI deals in Q1 2023:

- Instadeep, an AI-based decision making solution for biology and energy sectors sold to BioNTech

- Horsefly, a recruitment software business with AI search capabilities, invested into by LDC

Grant Thornton Q1 deal highlights

Advising the shareholders of Tiger TMS, the software provider to the hotel and hospitality industries, on its sale to Canadian consolidator Valsoft.

Advising GCP-backed digital transformation specialist HippoDigital on its acquisition of The Data Shed.

Advising the shareholders of Horsefly on its investment from LDC. Horsefly is a technology recruitment platform that provides talent data, analytics and sourcing solutions.

The investment in field service management software specialist JobLogic by Axiom Equity.

The sale of Livingstone Group to One Equity backed Trustmarque Solutions, creating an exit for Carlyle.

For more insight and guidance, get in touch with Andy Morgan.

What does it take to be a top performer in UK tech?

So many start-ups and scale-ups brand themselves as 'disruptors' that it's difficult to know which ones are really making a mark. The Megabuyte Emerging Stars programme recognises the UK's 25 best-performing smaller software and ICT companies with reported revenues between £3 and £10 million in the last financial year.

Andy Morgan explains the factors that enabled some companies to make the grade

![]()