Automotive review Q1 2023

What will the year ahead bring for the automotive sector?

With further significant change expected, what's the outlook for UK automotive in 2023? In this review you can read insight on the long-term consequences of these challenges, and other updates on the future of the sector.

Our experts share their views on China's price war spreading to Europe, and how tough new EU emissions regulations are affecting UK automotive. You'll also find out why solid-state batteries may hold the key to the future of electric vehicle production.

In 2022, the automotive market changed once more with supply chain issues still affecting both the upstream and the downstream. Battery electric vehicles (BEVs) also remained a focal point for change, and will continue to do so.

Chinese manufacturers are at the forefront of the BEV market and performed strongly in their own domestic market. In 2022, the Chinese new electric vehicle market increased by 93.4% versus the broader passenger car market, which rose by just 2.1%.

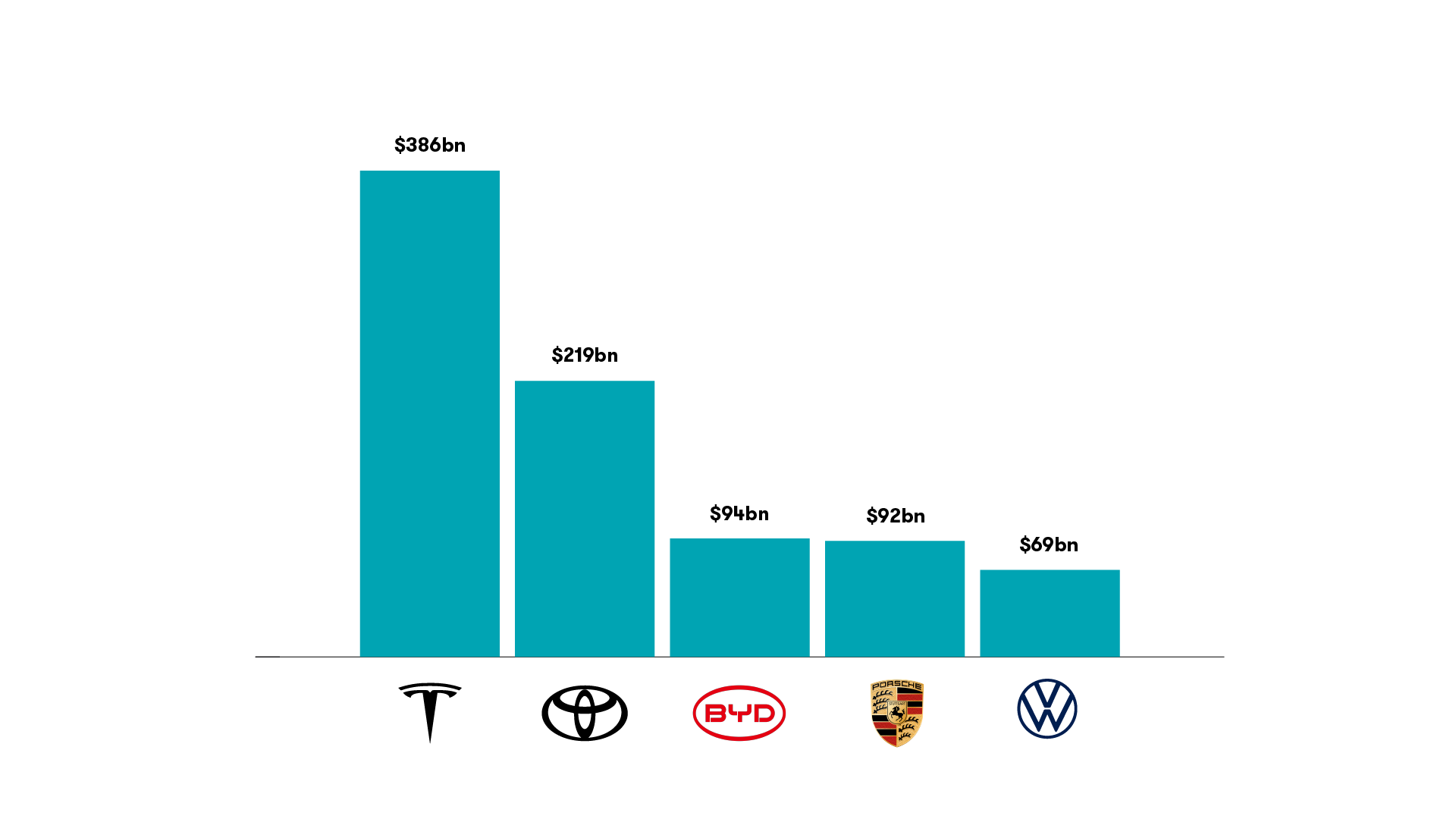

BYD was the strongest-performing Chinese original equipment manufacturers (OEM), selling 1.62 million BEV and hybrids, an increase of 132% year on year (YoY). Such strong sales in BEVs have driven up BYD’s market value, making it the world’s third-largest automotive company by value after Tesla and Toyota. Tesla remains the most highly valued, although the company’s share price dropped by around 70% in 2022 from its all-time high of USD1.2 trillion.

Top 5 global automotive manufacturers by market cap value (USD billion)

Source: Sino Auto Insights (3 January 2023)

The Chinese brands have started a BEV pricing war in their home market. They're more price competitive than the European and American incumbent OEMs (E&A OEMs) – BMW, Stellantis, Mercedes-Benz, Ford, Tesla, etc – and the following table of mid-sized SUV prices shows that the Chinese manufacturers continue to price aggressively in their own market.

Aggressive pricing by the Chinese OEMs in the China market

Mid-sized SUV – premium market

| BMW iX3 | MB EQB | MB EQC | Audi e-tron | Tesla Model Y | Nio ES6 | Xpeng G9 | |

|---|---|---|---|---|---|---|---|

| Platform | Legacy | Legacy | Legacy | Legacy | Dedicated | Dedicated | Dedicated |

| Body style | SUV | SUV | SUV | SUV | Crossover | SUV | SUV |

| Variant | - | 260 | 350 | 50 Deluxe | LDRM | 70Kwh | LR |

| Price (RMB) | 399,990 | 351,800 | 491,900 | 546,800 | 357,900 | 386,000 | 349,000 |

Source: BNP Paribas Exane research

Although retail prices for Chinese brands aren't significantly lower than the E&A OEMs, the Chinese brands are significantly better equipped with full infotainment and advanced driver-assistance systems (ADAS). The E&A OEMs fall short in providing this as standard.

Such an aggressive stance has made it difficult for some western incumbent OEMs to compete, both for BEVs and internal combustion engine (ICE) vehicles. This is borne out by the GAC-Stellantis Jeep joint venture’s decision to file for bankruptcy in October 2022. Stellantis CEO Carlos Tavares indicated that Peugeot and Citroen, its other brands sold in China, could also exit manufacturing in the Chinese market.

During 2022, fewer than 2,000 Jeeps (ICE vehicles) were sold in China – only one Jeep sold in May 2022. This suggests that the Chinese brands are taking the pricing war not only to BEVs, but also to ICE vehicles. With aggressive pricing for both BEVs and ICE vehicles in China, it's not clear whether there will be other OEM casualties. But we do know that with China’s advanced battery technology, sourcing of raw materials and more advanced BEV supply chain, Chinese OEMs are able to manufacture BEVs at EUR10,000 cheaper than European automakers, representing a significant cost advantage.

BEV pricing competition is expected to continue increasing in China as the Chinese OEMs try to establish a price level at which the price of a BEV is at parity with that of ICE vehicles. Increased emissions legislation will drive up the supply of BEVs across the globe,ensuring that BEVs will have a higher global market share than BEVs in the medium term. Europe is expected to experience an influx of Chinese brands over the next 12 to 24 monthsas China’s domestic sales of ICE vehicles and BEVs lose traction – although BEV growth is estimated to be double digit.The Chinese BEV OEMs are pushing into Europe’s premium and mass market with cut-price product offerings designed to gain market share quickly. This could trigger a BEV and ICE vehicle pricing war in Europe,pushingBEV and ICE vehicle prices lower.

Chinese product in the mass hatchback segment BEV European market

Hatchback – mass market

| VW ID.3 | Renault Megane | Peugeot e-308 | MG MG4 | ORA Funky Cat | |

|---|---|---|---|---|---|

| Platform | Dedicated | Dedicated | Legacy | Legacy | Legacy |

| Body style | Hatchback | Hatchback | Hatchback | Hatchback | Hatchback |

| Variant | Pro Perf | E60 220 | Pro | 64Kwh | - |

| Price (EUR) | 38,060 | 46,600 | 44,000 | 35,990 | 36,500 |

Source: BNP Paribas Exane estimates

Increasingly competitive pricing by the Chinese OEMs creates a risk that the margins of European OEMs might come under pressure. It's not yet clear, however, if Europe will react to this influx of vehicles by imposing further tariffs on imported vehicles, and the Chinese OEMs will have to consider the long-term positioning of setting up factories in Europe. The US has recently passed the Inflation Reduction Act , which is restricting overseas OEMs from importing vehicles into the US. Although this provides an opportunity for the Chinese OEMs to expand into new markets, it may take time for the Chinese brands to gain a strong hold in Europe. This is due to the lack of brand recognition, consumer acceptance and the reduction in future BEV subsidies across Europe that will slow BEV growth in general.

OEM profitability remained robust in the face of supply chain disruptions as vehicle shortages meant that retail prices remained high, allowing profit margins in 2021 and early 2022 to hold up well. But the rise in raw material prices and disruptions in the supply chain, caused by gas shortages in Europe, is having an impact on profits. According to JP Morgan, many OEMs are reducing their exposure to European gas: Renault cut its gas consumption by 10% in 2022; 20% of VW’s gas intake has been reduced or replaced with coal or oil, and BMW cut its gas usage in Germany and Austria by 15% in 2022.

However, some automotive raw material prices have declined over the coming month, albeit from a high level in Q3-Q4 2021 and Q1 2022. [SRE23] [OE24] Raw material prices are still not back to 2019 levels and in some cases – such as polypropylene – have experienced limited declines, while prices for other raw materials, such as steel, are significantly lower.

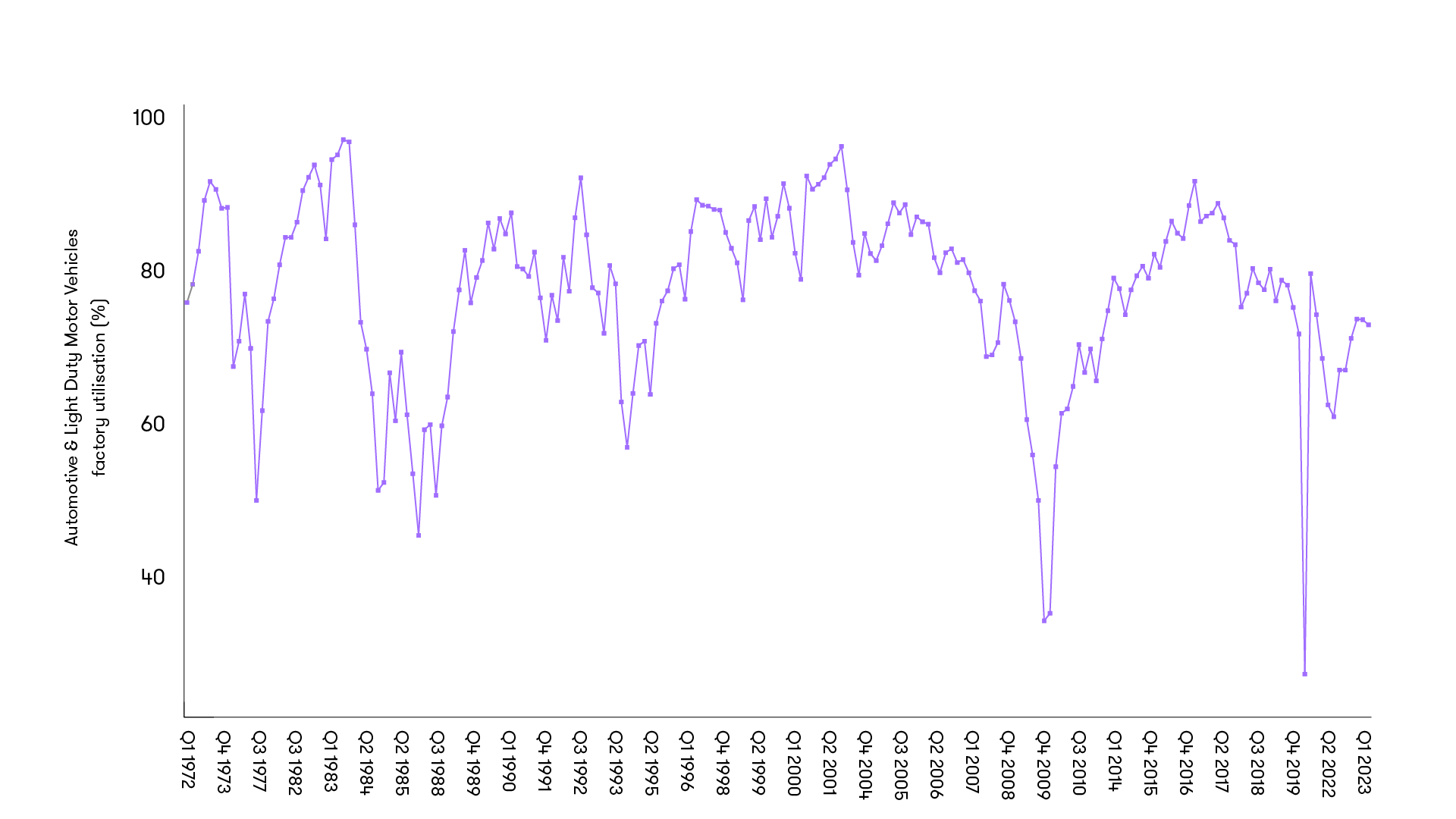

In 2023, OEMs are likely to stabilise their earnings against a backdrop of lower costs for some raw materials, and a less volatile supply and distribution chain. The following chart shows that production in the US factories is on the rise and capacity utilisation is heading back to more normalised levels of 76%.

Capacity utilisation: automotive and light duty motor vehicles

Source: Board of Governors of the Federal Reserve Systems (US)

While this is positive news, global economic conditions remain uncertain. The supply of and demand for vehicles could also be affected by any trade disruption caused by intensifying protectionism and sanctions, alongside any new pandemic impacts.

BEVs will continue to experience robust growth driven by legislation. In the UK, the Department of Transport is consulting on its zero emissions vehicle (ZEV) policy, which could mandate automotive manufacturers to register a certain amount of zero emission cars and vans in the UK by 2024 in preparation for a 2030 ban on new pure petrol and diesel cars.

More information on this mandate is expected later this year, with potential implementation on 1 January 2024.

For more insight and guidance on the automotive market, get in touch with Owen Edwards.

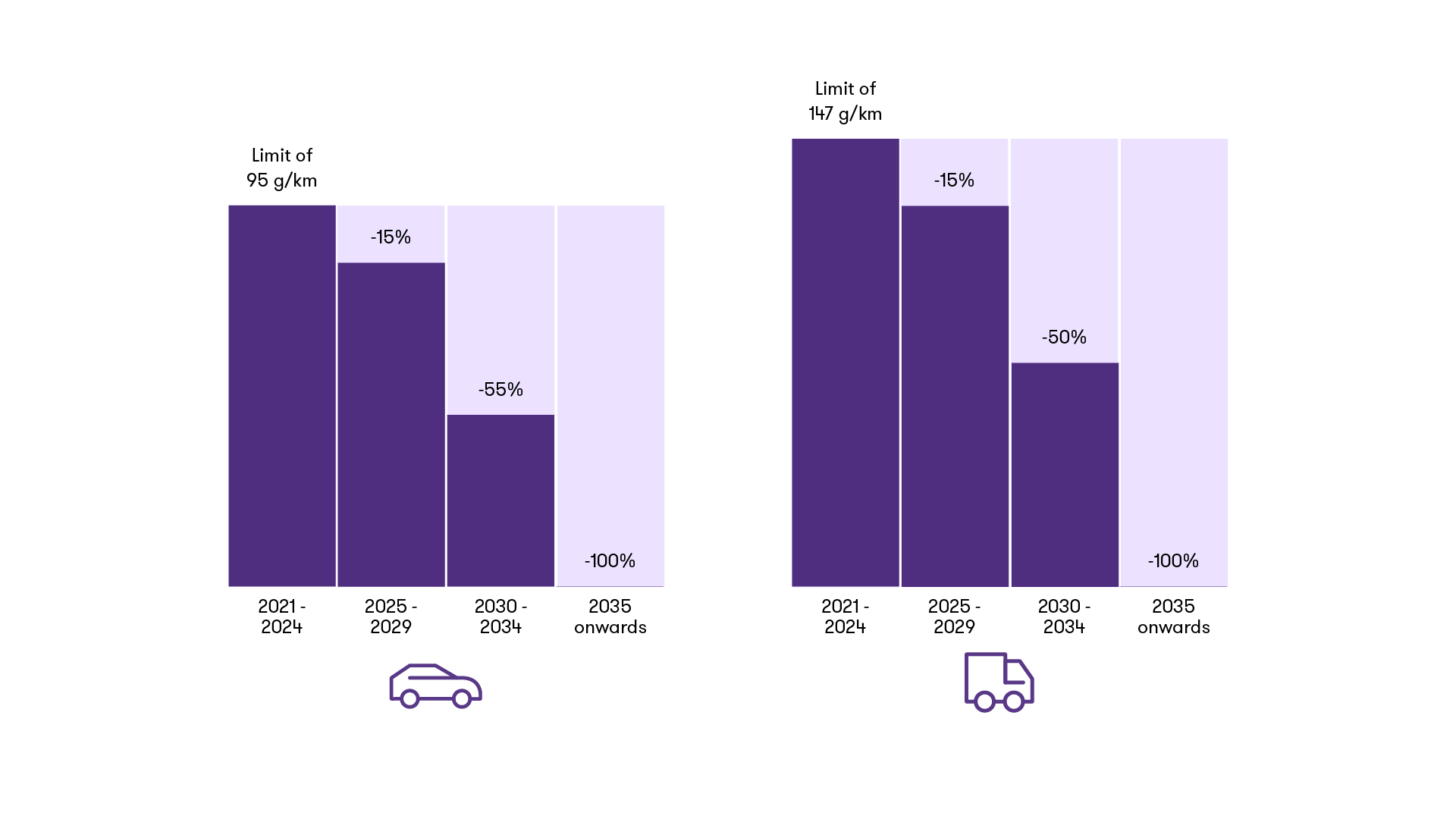

In our last automotive review we introduced the European Union's Fit for 55 package of ambitious climate policies and its potential significant impacts for the UK. Figures from 2021 from the Society of Motor Manufacturers and Traders (SMMT) show that the country's automotive sector employs over 182,000 people and produces around 0.8 million vehicles annually. It also accounts for 10% of the country's exports, making it a crucial player in the UK's economy. The industry has made significant strides in reducing carbon emissions but it still has a long way to go to meet the government's zero emissions target by 2030.

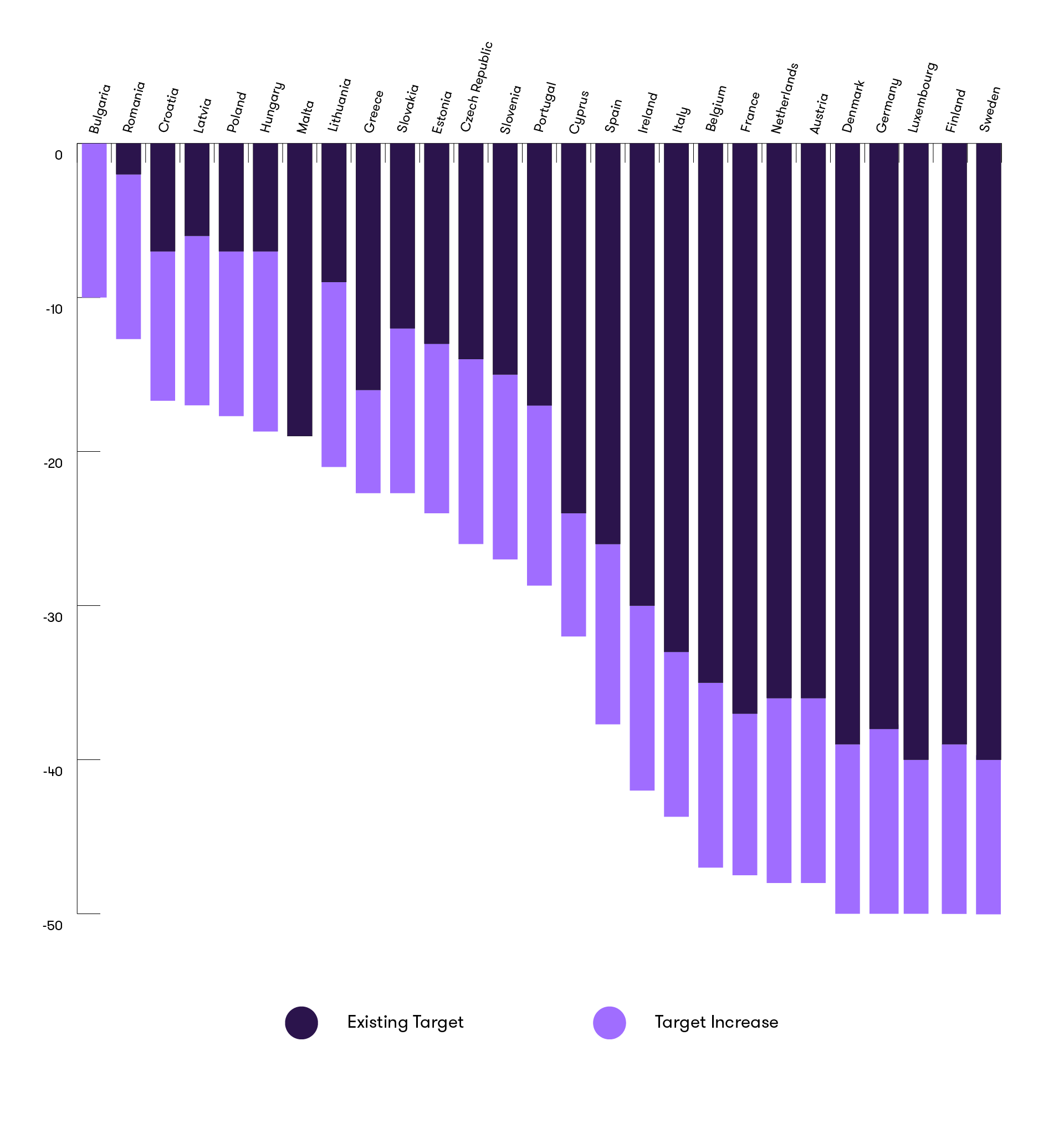

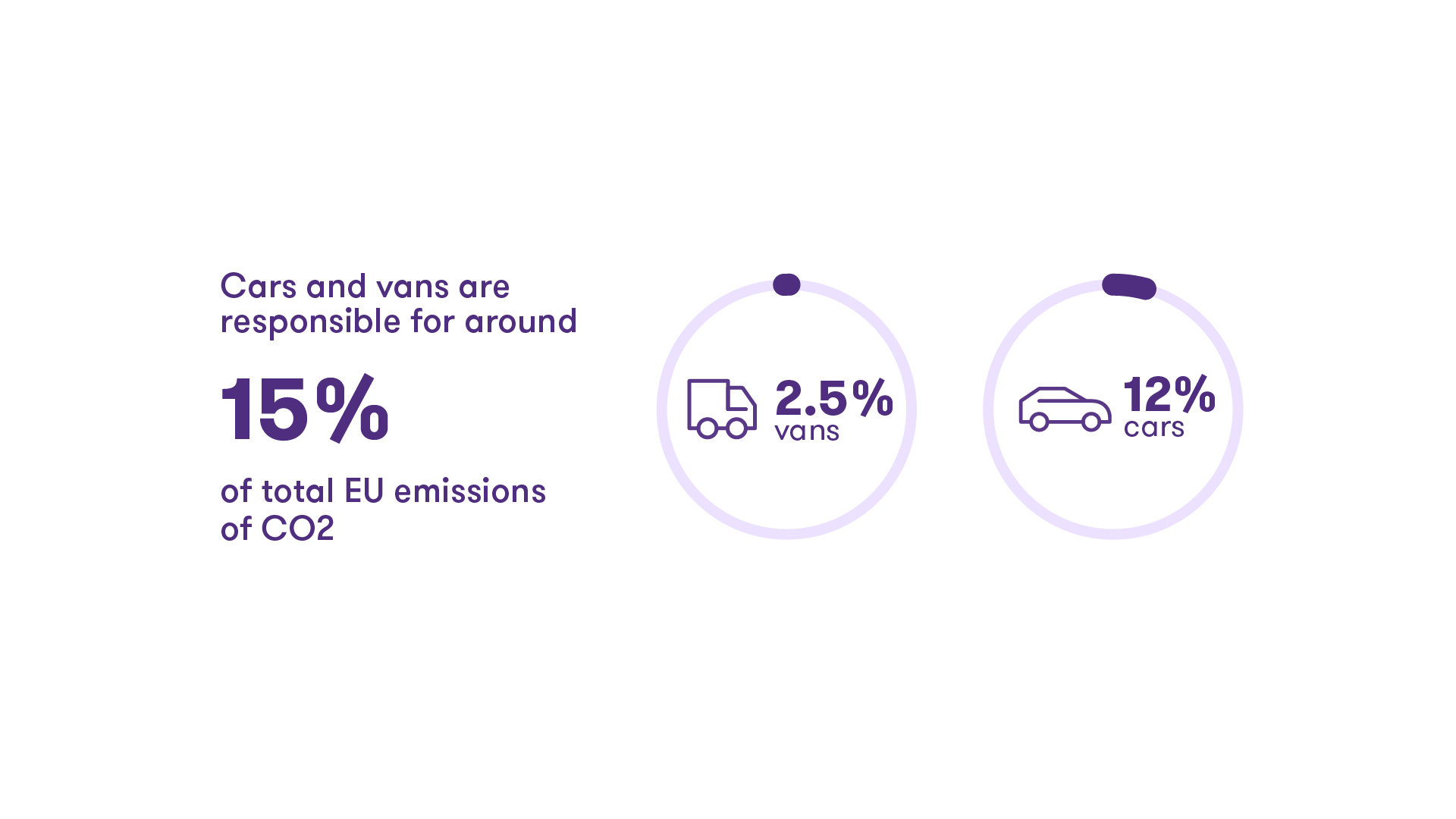

With EU member states making some bold forecasts on their carbon emissions reductions by 2030 (see chart), it's likely that the UK will look to align with the EU and its commitments. Original equipment manufacturer (OEMs) who manufacture vehicles for both the EU and UK will also have to abide by Fit for 55 rules. Cars and small commercial vehicles being manufactured form approximately15% of EU’s CO2 emissions.

Proposed projected target increases by 2030 per member state (in%)

Source: Fit for 55: reducing emissions from transport, buildings, agriculture and waste © European Union, 2022

Source: Fit for 55: why the EU is toughening CO2 emission standards for cars and vans © European Union, 2022

![]()

One of the most significant impacts of the Fit for 55 regulations is on the production and sale of vehicles. The regulations require that all new cars sold in the EU must emit less than 95 grams for domestic vehicles of CO2 per kilometre by 2021, which has been revised for 2030 to achieve a further 55% reduction. The new revised targets have been adopted by the council in March 2023. This means that car manufacturers must significantly reduce emissions from their vehicles.

Source: Fit for 55: why the EU is toughening CO2 emission standards for cars and vans © European Union, 2022

To meet this target, car manufacturers are turning to electric and hybrid vehicles. The UK automotive industry is investing heavily in the development of electric cars, with many manufacturers now offering a range of models to meet the demand from customers. Many more BEV and hybrid launches are expected in the coming years.

![]()

Another Fit for 55 impact is on the supply chain. As manufacturers switch to new technologies so demand rises for new materials, components, and batteries. Raw materials, such as lithium nickel, manganese and cobalt, are critical components of electric vehicle batteries. As a result, the UK automotive industry is working to secure its supply chains and reduce its reliance on imports from countries, such as China.

![]()

As the automotive industry shifts towards new technologies, this requires new skills and expertise in the workforce. New training programmes are being developed to upskill workers and attract new talent to the industry. Increased investment in research and development is also needed to support the development of new technologies and to ensure that the UK automotive industry remains competitive in the global market.

![]()

Automotive exports are also affected by Fit for 55 rules. The regulations are creating a more level playing field for European manufacturers, which means that UK manufacturers may face increased competition in the EU market. However, the regulations also present an opportunity for UK automotive to develop new technologies and products that can be exported to other countries.

In conclusion, the Fit for 55 regulations are having a big impact on UK automotive in 2023. The industry is working hard to meet the new emissions targets and to develop new technologies to reduce its environmental impact. Amid the challenges, such as securing supply chains and upskilling the workforce, lie significant opportunities for the industry to innovate and compete in the global market.

For more insight and guidance, get in touch with Raj Kumar

Adoption of battery electric vehicles (BEVs) is on the increase, but consumers still have concerns over the range and safety of BEVs. However, emerging battery technology, such as solid-state batteries should be safer with lower susceptibility to thermal runaway. The range per charge will also be higher than what is available from current technology.

Ilika plc is a pioneer in ground-breaking solid state battery technology designed to meet a wide range of applications: medtech, industrial internet of things (IoT), BEVs, and consumers electronics. The business is headquartered in the UK, but has operations in USA, China, and Israel.

What is Ilika’s role in the battery market?

"Ilika are developers of solid state battery (SSB) cells in the UK. We started working on materials for SSB as early as 2008 when Ilika was offering contract R&D services to major OEMs. In 2016, we developed our first range of SSB, a mm-scale battery produced using techniques common to the semi-conductor and integrated chips. These are intended to enable miniaturisation in implanted medical devices, and we've recently signed a memorandum of understanding (MoU) with US medical device company Cirtec Medical for the manufacture and commercialisation of these cells.

"Then in 2018, we were lucky to be awarded three grants from Innovate UK (Faraday Battery Challenge), which kickstarted the development of Goliath, our second range of SSB. This one is targeting electric vehicles (EV), and uses materials, equipment and processes much more in line with lithium-ion manufacture."

How are you preparing for rising demand for EV batteries?

"Lithium-ion chemistry was really an enabler for the deployment of electric vehicles. But although electric vehicle uptake is growing, it's still low and reflects various doubts from passengers in terms of range, safety, reliability and price, as well as anxiety related to the availability of charging points. In terms of performance, current lithium-ion chemistries will likely plateau in the next few years. To alleviate limitations placed on vehicle performance, we believe that solid state battery chemistry will eventually take over from lithium-ion due to its unique features and benefits."

What's different about solid state batteries?

"SSB are essentially lithium-ion rechargeable batteries with a different electrolyte (the component between the positive cathode and negative anode). Lithium-ion uses a liquid electrolyte whereas SSB’s electrolyte is solid. This simple difference provides a safety improvement because the solid electrolyte is less susceptible to thermal runaway and gas evolution, and superior energy density as the denser solid electrolyte can provide smaller batteries or more power in same-size battery.

"Improvement can also be realised at pack level. SSB can also operate at higher temperatures than lithium-ion, which helps battery pack designers to reduce the complexity of the cooling and testing system, leading to lighter packs and therefore vehicles."

What are your plans for the future?

"Our efforts are focused onto two areas. First, we'll concentrate on developing our first product: an SSB cell for electric vehicles. Technical work is still needed to increase the dimensions of our prototypes and the number of layers in the pouch, as well optimising some of the performance parameters.

"Second, we're preparing for scale-up in parallel. We're collaborating with tool suppliers and automation specialists to ensure that production equipment exists for the mass manufacture of SSB. The good news is that the majority of machines used for lithium-ion battery production can also be used with SSB, and we're already working with collaborators on the development of those pieces of kit that are more SSB-specific. Our goal is to license our technology to original equipment manufacturers for manufacture at giga-scale. In the meantime, we aim to exemplify SSB manufacture on production-intent equipment."

For more insight and guidance, get in touch with Owen Edwards.

![]()