The Financial Reporting Council (FRC) published “Amendments to FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland and other FRSs – Periodic Review 2024” on 27 March 2024 (Amendments to FRS 102). These amendments change the requirements of the Financial Reporting Standard applicable in the UK and Republic of Ireland (FRS 102), including important changes to lease accounting. Most notably, most leases will need to be capitalised and brought onto the balance sheet.

Who is this relevant for?

The amendments are relevant for companies reporting under FRS 102, and reflect changes implemented by IFRS 16 back in 2019. Companies who lease large quantities of retail stores, offices, cars, aircraft or other high-cost items will face a substantial impact on their financial statements, covenant compliance, systems, processes and controls.

While some investors and stakeholders may have already adjusted, and mid-market listed companies already have to report under IFRS at a plc level, underlying group accounts and financial covenants may be entirely UK GAAP based.

The new accounting guidelines are expected to affect 3.2 million reporting entities in the UK and will come into effect on 1 January 2026.

How will the new rules affect lease accounting?

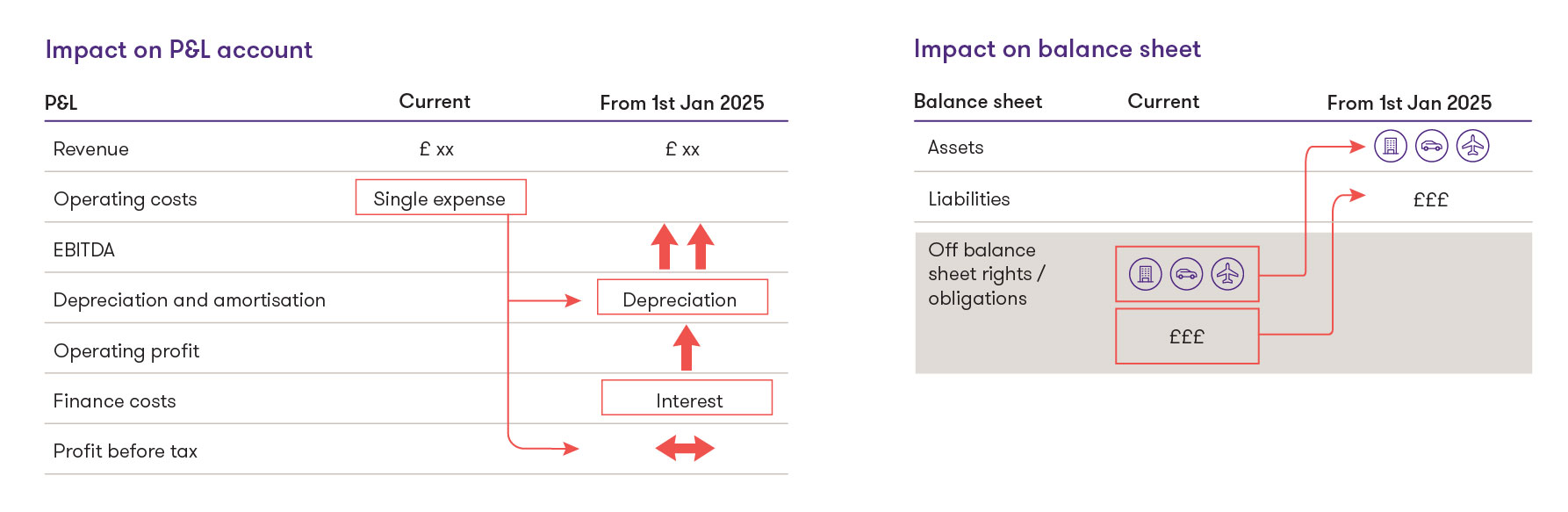

Currently, companies with operating leases (for example rental agreements for real estate) treat rental payments as a business expense in the profit or loss account. Changes are considered necessary as this accounting method does not consider that a business is able to benefit from an asset such as a property that it rents under a long lease, nor that the asset is tied to a long-term liability.

From 1 January 2026, companies will be required to capitalise the majority of their operating leases. This will be done by recognising the present value of the lease payments and showing them as either ‘right-of-use’ assets, or together with ‘property, plant and equipment’.

The ‘right-of use’ assets will need to be depreciated over the remaining term of the lease. Any current operating lease expense will be replaced by a depreciation charge on the asset, and a finance charge on the lease liability.

![Two Illustrations depicting Impact on P&L account and impact on balance sheet]()

On transition date, the lease liability should be measured at the present value of the lease payments remaining at that date. These should be discounted using the lessee’s incremental borrowing rate, or ‘obtainable’ borrowing rate at the transition date. If neither of these can be determined, the lessee can use a gilt rate. The FRS 102 amendments in respect of borrowing rates do differ from the requirements of IFRS, which states that the rate used should be the ‘rate implicit in the lease’ or the lessee’s incremental borrowing rate (with no mention of gilt or obtainable borrowing rates).

If groups report under IFRS in their consolidated financial statements, FRS 102 amendments permit entities to use, as the opening balance, carrying amounts previously determined in accordance with IFRS 16 (ie using the same discount rates as those used under IFRS 16). This should provide efficiencies within groups and minimise measurement differences between reporting frameworks.

However, if this option is not taken, given the different rate choices available under each framework, this could potentially lead to different carrying amounts.

In summary:

- Assets will increase – being the ‘right of use’ asset

- Liabilities will increase - being the discounted amount of future lease payments. This could be viewed like a long term loan

- EBITDA and operating profit will increase – as part of the cost of the lease will now sit in finance costs.

Impact on financial ratios and covenant compliance

The impact of these changes on financial reporting, covenant compliance, systems, processes and controls could be substantial – especially to those companies who lease large quantities of retail stores, offices, cars, aircraft or other big-ticket items.

Many financial ratios and performance metrics will be impacted, including interest cover, EBITDA and operating profit. Leverage may increase and capital ratios will decrease. These changes may therefore affect a company’s ability to meet financial covenants and comply with existing loan documentation.

‘Permitted baskets’ in restrictive covenants may also be breached due to the different treatment of operating leases.

The valuation of a business could be affected, as well as bonus / remuneration / share option schemes if these are linked to financial performance.

There are certain exemptions. Leases with less than 12 months remaining at the transition date or leases for assets of low value can continue to be accounted for as operating leases.

Working with borrowers and private equity financial sponsors on raising and refinancing debt

Learn more about how our Debt & Capital Advisory services can help you

How can companies prepare?

Management should seek advice on remodelling and recalculating financial covenants considering FRS 102 changes.

Borrowers should speak to their lenders now if they have debt covenants which may be affected by these accounting changes. Financial and restrictive covenant levels may need to be amended, or consideration given to using ‘frozen GAAP’.

The process and cost of implementing these changes could be significant, especially if there is no current system to collate relevant lease data, and management need to start putting these systems in place as soon as possible. Information must be complete and accurate, including determining the appropriate borrowing rates attached to each lease, and the least term (taking into account options to extend, or terminate).

Companies should start preparing now to be ready for the implementation date of 1 January 2026.

For more information or advice, contact Christopher McLean, Jon Bramwell, Pinkesh Patel and Jennifer Ilsley.

Read our expert insights from our UK debt advisory specialists, who can help you to navigate the complex lending landscape and wider debt markets.