Report

Charity sector development report 2024

Find out more about emerging risks and issues in the charities sector, including changes to FRS 102, in our report.

Basel 3.1 is at a near-final implementation stage – policy statement 17/23 is the first of two papers from the PRA. This one looks at scope and levels of application, market risk, credit valuation adjustment, operational risk, Pillar 2, and currency redenomination. The second paper, due in Q2 2024, will look at credit risk (standardised and internal ratings-based approach), credit-risk mitigation, output floor, Pillar 3 disclosures, and reporting.

The PRA is waiting for HM Treasury to legally revoke the Capital Requirements Regulation (CRR) before it can update the relevant sections in the PRA rulebook. The regulator will soon publish all final policies, rules, and technical standards in a single policy statement.

For financial services firms this means a wave of technical updates, mapping their financial and non-financial data to new and revised sets of regulatory returns, updating internal regulatory documentation, and market disclosures.

To understand how in-scope firms are navigating the changes, we surveyed 33 banks and building societies of different sizes and complexities. We also posed the same questions to close to 200 in our recent technical webinar.

With the initial implementation date delayed by six months and final rules on a variety of areas still pending, and the PRA foreseeing the need for subsequent clarification papers, a lot of firms feel unsure about what to do.

Some have carried out impact assessments based on the guidance provided within supervisory statement SS and consultation paper CP 16/22, knowing that this is a complex task which requires a detailed assessment, regular catch ups with a variety of stakeholders, and assurance over the implementation programme. Others are waiting for the final rules before doing their assessment and implementation back-to-back.

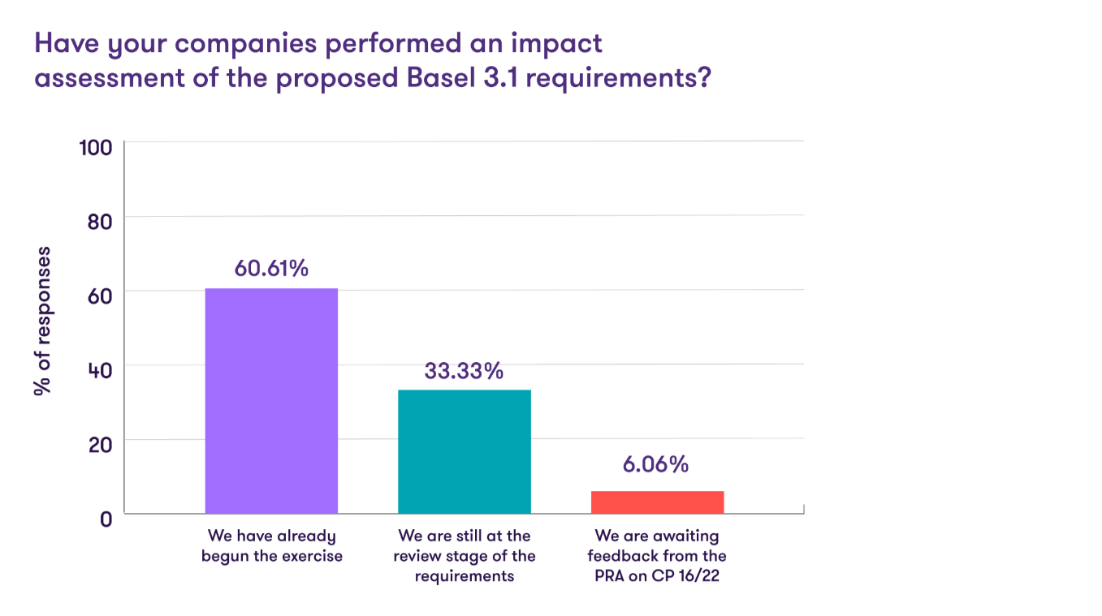

Most firms – 60.6% – have started working on impact assessments and planning, with a third still at the reviewing stage of the requirements. There are, however, a significant minority of firms, 6.1%, either waiting for clarity from the PRA or in the early stages of planning.

In our webinar on Basel 3.1 standards implementation and other considerations, the percentage of firms that have started working fell slightly to 56.3%, reflecting a larger set of respondents – over 190 banks and building societies attended.

Most respondents are waiting for further information and support on implementing changes proposed for the Credit Risk RWAs calculation and regulatory reporting. The PRA is scheduled to publish a second policy statement in Q2 2024, covering credit risk (standardised and internal ratings-based approach) and credit risk mitigation, as well as the output floor, Pillar 3 disclosures, and reporting.

Reporting and disclosure requirements are also high on the agenda. Chapter 12 of the consultation paper 16/22 covers the proposed changes to reporting. Firms will have to manage 19 new templates and updates to 23 templates to meet Basel 3.1 requirements.

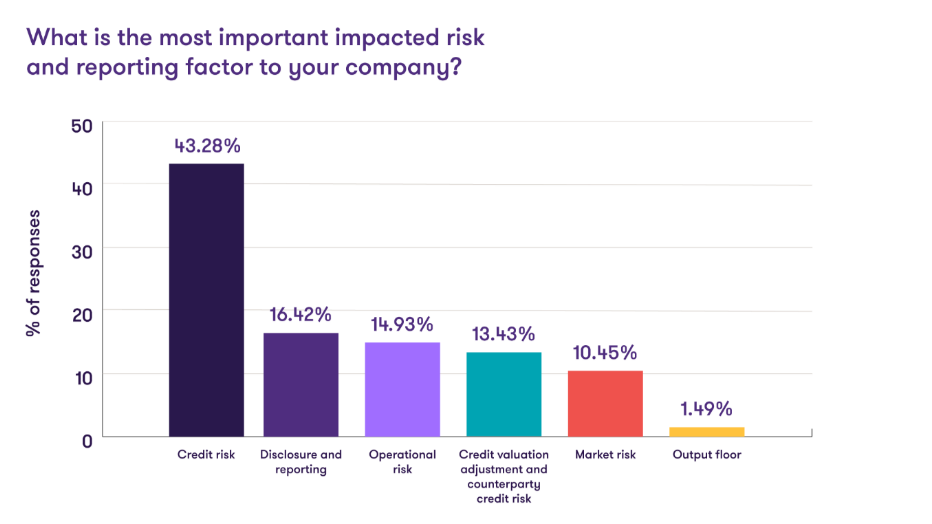

Among the banks initially surveyed, operational risk, credit valuation adjustment, and counterparty credit risk, and market risk are currently less significant factors, with only 1.5% of respondents pointing to the output floor - a new concept introduced under Basel 3.1. However, the near-final rules came out just before our webinars. We saw more respondents requiring further guidance on these following elements, particularly on the output floor and market risk.

As firms familiarise themselves with these areas, they're realising that they need more clarity.

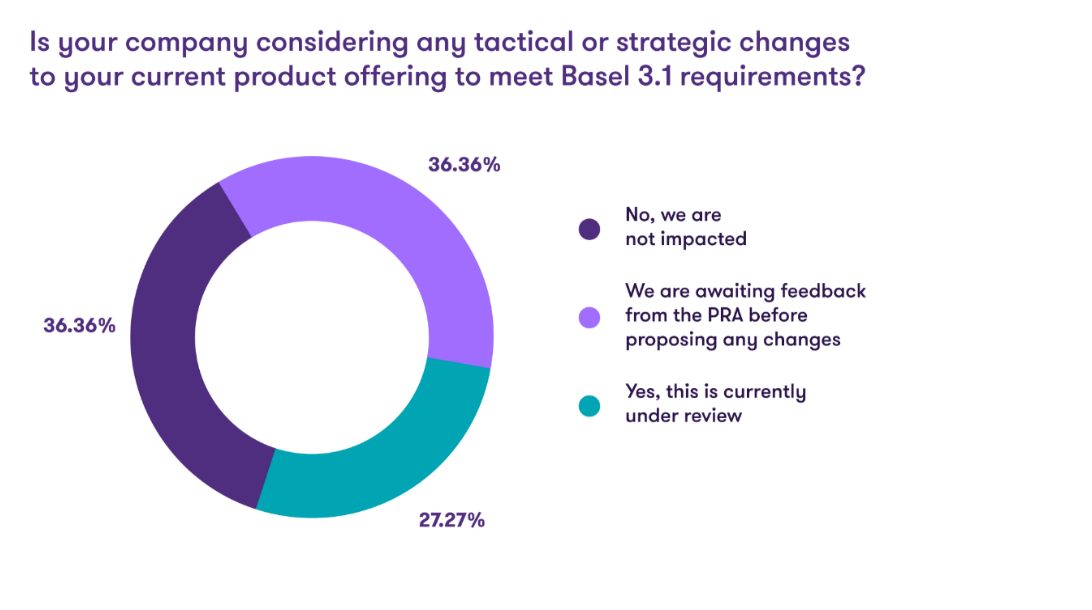

The Basel 3.1 reforms will impact on some products that financial services firms offer.

Close to two-thirds of firms are either actively reviewing their products already or anticipate making some changes when the PRA feedback is published. This is mainly driven by the introduction of a more risk-sensitive approach to Standardised Credit Risk.

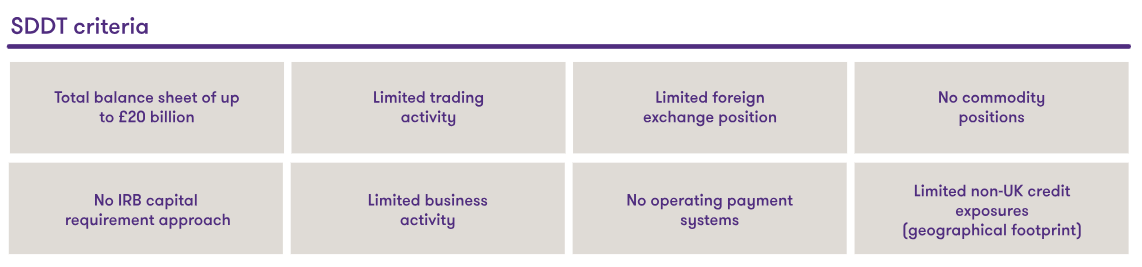

The timelines for Basel 3.1 and the Small Domestic Deposit Takers (SDDT) regime – formerly the strong and simple framework – don't line up that well. So, the PRA’s giving smaller firms two choices. They either stay on the Capital Requirements Regulation (CRR) and move to the SDDT regime when it comes in – this option’s called the Transitional Capital Regime (TCR). Or they can adopt Basel 3.1 now and move to the SDDT regime later.

Since 1 January 2024 eligible banks and building societies can submit a request to become SDDT by submitting a modification by consent request to the PRA.

Adopting the TCR may reduce business disruption and save money on implementation costs. But some firms may find that the other option reduces capital requirements in the short term – but it depends by how much, as implementation costs could wipe out any savings. It may just come down to what's practical for each firm.

Our survey showed only a small proportion of firms, 3%, are planning to implement the SDDT regime – formerly the strong and simple framework. Either firms don't meet the eligibility criteria for implementing the SDDT regime or don't want implementation changes in two stages. This signals how the industry is responding to the PRA’s proposed approach for regulating small to medium-sized financial institutions, which is likely to see more developments.

In contrast, our webinar showed that 77% of respondents said they're looking to leverage the regime, highlighting the change as the full implications of the regulatory requirements become clearer. As such, firms need to think about their business growth plans and the cost/benefit of adopting the more complex Basel 3.1 requirements.

For some firms, the Board has become familiar with the CRR and, therefore, prefers adopting the Basel 3.1 changes.

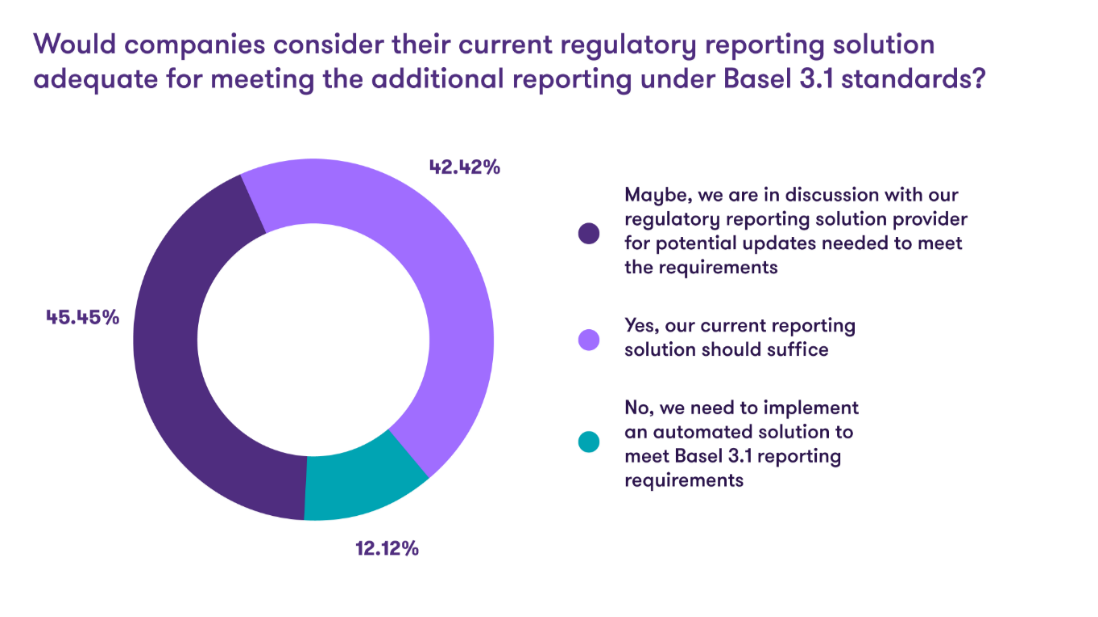

42% of firms responded that their current regulatory reporting system will be able to handle the additional reporting requirements, while 45.5% are in discussion with their reporting solution provider to see if that's possible. Only 12.1% of firms that were planning to change their systems and improve automation.

In our webinar we asked firms the challenges the faced on broader data requirements: close to half of respondents that data quality and consistency was their biggest issue, 29.4% noting that data integration from multiple systems was proving difficult.

Firms should consider building about a data warehouse - a data management system that centralises all data to support quality and consistency. This can also change how firms approach reporting and strengthen the accuracy and alignment with Basel 3.1.

Data governance is another core concern. More firms are starting to approach it in a holistic way that combines data policies, data standards, and data governance frameworks. They're also starting to prioritise their most important data to make sure data remains reliable and fit for purpose.

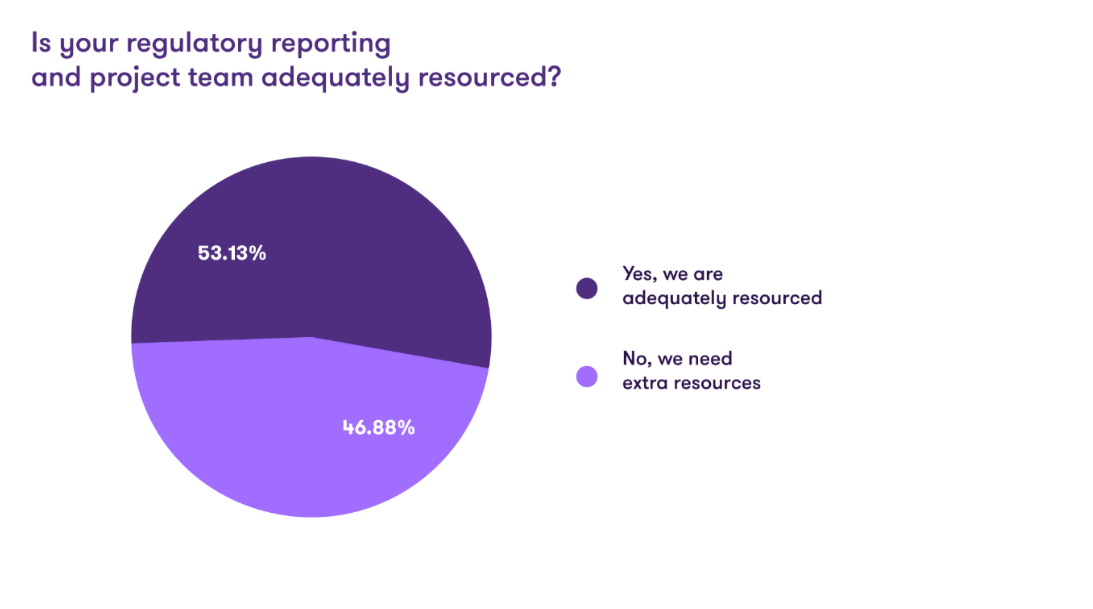

This could be a key factor feeding into the need for more resources. 46.9% of firms said regulatory reporting and project teams need additional resource to comply with the incoming standards.

With a looming deadline of 1 July 2025, you should act sooner rather than later.

The changes in Basel 3.1 represent complex regulatory challenges for firms, and ensuring there's a robust implementation programme is important. You'll have to consider the impact on their business models, product lines, as well as keep the project sponsor abreast of developments to ensure effective oversight.

While there's no one set path to compliance, the PRA’s consultation paper shows the direction of travel – stakeholders should understand the impact, plan, and allocate sufficient resources.

To learn more about these changes and how to overcome key challenges, contact Kantilal Pithia, Sonam Nawani, and Paul Cook.

![]()