Report

Charity sector development report 2024

Find out more about emerging risks and issues in the charities sector, including changes to FRS 102, in our report.

What will the year ahead bring for the automotive sector?

Original equipment manufacturers (OEMs) across the UK's automotive industry have been unable to supply the global market, keeping the prices of both new and used vehicles high. At the end of 2022, the number of new vehicles registered in the UK was 1.61 million units, the lowest number of new registered passenger-vehicles in the last 10 years. This is a 2% decline on 2021, and 30% on pre-COVID-19 levels (2019 full year registrations). Limited new-car supply meant that H1 2022 suffered the greatest decline in new vehicle registrations, leading to a 11.9% year-on-year decline in the new car market.

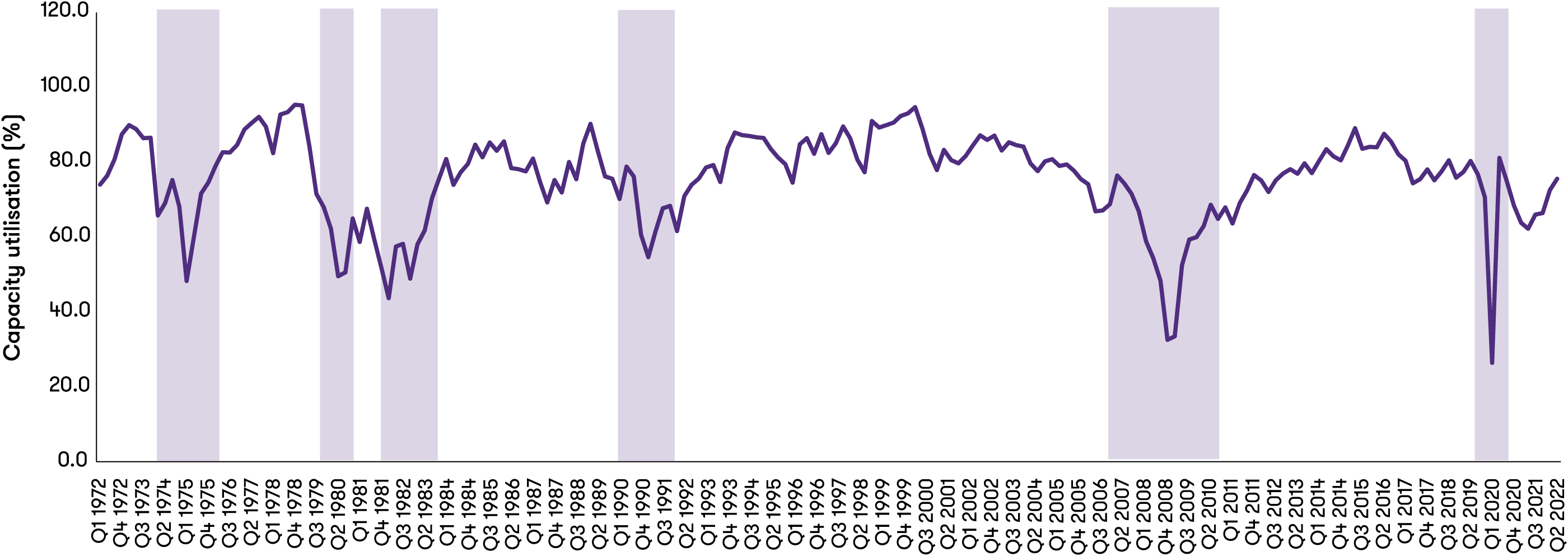

In the second half of 2022 vehicle supply increased, resulting in a return to year-on-year growth rate in new vehicle registrations. The evidence suggests that factories are starting to increase capacity as the semi-conductor shortage slowly becomes less of an issue. We can't determine OEM factory capacity in Europe and the UK as this information isn't readily available.

Capacity Utilization: Automobile and light duty motor vehicle, Percent of Capacity, Quarterly, Seasonally Adjusted (USA)

Source: Federal Reserve Economic Data

Although the supply of semi-conductors is improving, supply and distribution chains are struggling. Some OEMs have indicated that the lack of trucks and truck drivers has meant that even OEMs who have solved their semi-conductor issues can't move vehicles from the factory gate to dealers. However, disruptions in supply chains and distribution are expected to continue well into 2023, prolonging shortages in some brands and models. Recent joint forecasts from our team and Cox Automotive indicate limited improvement in 2023. Any strength in new vehicle growth will be in the later part of the year.

New vehicles registrations 2023

Source: Grant Thornton and Cox Automotive

The shortage of new vehicle supply has also impacted the used car market, where 1.5 million fewer vehicles are estimated to have been supplied to the used car market between 2019 to 2022. In turn, this has led to a shortage in the supply of used vehicles, which has meant that used vehicle sales declined to 6.8 million units in 2022. Expected growth in the used-car market this year will be curbed to some degree by the ongoing shortage of vehicles, and by weak demand exacerbated by faltering consumer confidence and tough economic conditions.

Used car sales 2023

Source: Grant Thornton and Cox Automotive

The chart below shows consumer confidence levels, which have remained negative since May 2016 and are expected to remain negative for the foreseeable future. This weak consumer confidence will be reflected in demand for used and new vehicles in 2023. There might be some weakness in the used-car prices due to poorer demand, but this isn't expected to be significant as used car prices will be supported by the shortage in supply of used vehicles (source: Autotrader).

Consumer confidence

Source: GfK

Used vehicle retail prices in the UK

Source: Autotrader

In 2023 growth in the automotive industry in the UK is expected to be limited – registration and vehicle sales. Production is expected to improve in 2023 as OEMs receive an increased supply of raw materials and semi-conductors, etc, and once again vehicle production starts to increase, albeit starting from very low registration levels. Therefore, the focus this year will be on controlling costs as inflation increases in 2023. Sales teams should be focusing on vehicle sale as consumer confidence remains weak. Every sale needs to be considered and followed up. Cashflow still remains core to retaining a robust positioning in the automotive market.

For more insight and guidance, get in touch with Owen Edwards.

The Fit for 55 proposals aim to provide a coherent and balanced framework for reaching the EU climate objective of reducing net greenhouse gas emissions by at least 55% by 2030. The package will include the following areas of focus:

The proposals were submitted to the European Council in July 2021 and are currently being discussed in relation to several policy areas, such as environmental, energy, transport, and economic, and financial affairs. The EU countries are working on new legislation to achieve the goal of reducing emissions by at least 55% by 2030 and making the EU climate neutral by 2050.

What is included in the Fit for 55 package?

Although it isn't clear whether such regulation will impact the UK, we know that if implemented in law, the OEMs who manufacture vehicles for both the EU and UK will have to abide by the rules within the Fit for 55 package. Therefore, even if future UK emissions legislation is less restrictive than the EU, it's highly likely that the global OEMs will operate to future EU standards.

The Council and the European Parliament have reached a provisional political agreement on stricter Co2 emission performance standards for new cars and vans, with the following outcomes:

It isn't clear when this will be fully implemented, but it provides a clear message to the OEMs that Co2 emissions for cars and vans will become more stringent.

It looks as though the UK government will be following a similar policy and this could be one of two approaches.

1 Working off the current Co2 emissions framework which would mean that vehicles by 2035 would be zero Co2 emitting

2 Introduction of a ZEV mandate / sales target along side Co2 regulations – under this scenario the UK government would set targets for the number of ZEV vehicles sold

At present the UK government is going through consultation and it isn't clear at what level the government will set its targets. However, what we know is that it will have to be sufficient to enable the OEMs to reach a level of ZEV by 2035.

For more insight and guidance, get in touch with Owen Edwards or Raj Kumar.

In 2019 a little under 17,000 Chinese made cars appeared on UK roads; three-quarters were MGs, once a sporty UK brand, but now owned by SAIC of China. The balance were Volvos, almost all of which were S90 Sedans. In 2020 sales of Chinese-made cars rose to nearly 23,000; MG’s share of this rose to 81%, while Volvo’s declined, and the first Polestars appeared on UK roads.

In 2021, with the UK market depressed as a result of the pandemic and reduced availability of cars from Europe as European vehicle manufacturers rebuilt their production systems, Chinese-sourced models sold in the UK more than trebled to nearly 76,000. MG’s share fell to 40% and Tesla leapfrogged MG with a 45% share – Tesla sourced vehicles from China because its US plant couldn't make enough vehicles and its German plant hadn't yet opened. Volvo sales continued, while Polestar’s share grew to c.4,000 and the first Chinese-made BMWs appeared, with the iX3 electric SUV leading the way. This pattern continued in 2022, with a small number of Citroen C5X SUVs and the large DS9 Sedan arriving in the UK.

Other well-known brands will also source new electric vehicles (EVs) from China, including Smart (production having shifted from France) and Mini (replacing the UK-made Mini Electric), while a new small Volvo SUV, possibly called XC20, is also likely to be sourced from China owing to capacity constraints at Volvo in Belgium.

Some of the Chinese-made Teslas will be replaced by models sourced from Germany, but some sourcing from China will likely continue, despite the 10% import duty levied on Chinese-made cars (US-made models also face a 10% import duty). The other well-known brands will continue sourcing from China, largely because the models they source from China are only made in China. MG has added to its imported range with the MG4 Electric being sold across Europe, including in the UK, from early October. The MG4 Electric has been positioned directly against the VW ID3 and is intended to help raise MG’s European sales to over 100,000, with the UK being the largest market for now, accounting for 45-50,000 expected sales this year.

The next stage of the rising influence of Chinese-made models on UK sales will come with BYD, Great Wall, and Ora the unfamiliar names we can expect to see on UK roads in 2023. BYD will sell its Han saloon, Tang SUV and Atto 3 crossover. It will also sell its Seal model, reportedly a direct competitor to the Tesla 3. A BYD spokesman has suggested that European production is possible but if BYD and others can sell Chinese-made models – including the 10% import duty levied on their landed value – at a profit in Europe why will they invest in manufacturing in Europe?

Nio, another new Chinese EV manufacturer, is already selling its cars in Norway and some other European markets and are growing their presence through the installation of innovative battery swapping facilities. No doubt the Nio will appear in the UK soon, but they'll likely be preceded by Ora (a Great Wall brand), with its Cat 01 small hatchback, another model designed to take on the ID3.

Other Chinese brands on their way to the Europe include XPeng, with the P5, a Tesla 3 competitor, and the P7 Sedan; Lynk & Co, a Geely brand, was due to have some production take place at Volvo in Belgium but when this plant ran out of capacity owing to heavy demand for XC40 and C40, plans for European production were shelved. Lynk & Co will launch the 01 hybrid in the UK in 2023, with other models not far behind.

UK – and European – consumers don't appear worried about buying cars from China; some people, including those buying the BMW iX3 and Volvo S90, may not even know their cars come from China.

Undoubtedly, there will be a consumer cohort who wants European-made cars, with some also only wanting to buy cars made in their own countries, but this number is declining. Moreover, with computers, iPhones and much more besides coming from China, if Chinese-made cars pass requisite technical standards and are sold at affordable prices (including 10% import duty levied at port of entry), then consumers appear willing to buy them, especially with mushrooming delivery times for European-made models.

Consumers who once only wanted German cars from Germany have long accepted Mercedes and BMW SUVs from the US, Audis from Mexico or Hungary, and Volkswagens and some BMWs from South Africa. Ford Transit drivers (a vehicle long marketed by Ford as the backbone of Britain) drivers of vehicles made in Turkey, as have drivers of the Renault Clio, Toyota CHR and Hyundai i10 and i20. The geography of manufacturing – even for some premium brands – no longer seems to matter; or perhaps it never did, and we simply thought it did.

For more insight and guidance, get in touch with Oliver Bridge.

Electric vehicles are the future for climate-conscious driving, but extracting the rare earth materials to build lithium-ion batteries isn't an environmentally-friendly process. Developing low-carbon approaches to extracting, refining, and processing these raw materials can reduce the impact of building new batteries, but extending their life through recycling will also be critical.

Ecobat Solutions is the leading pan-European provider of battery collection, dismantling, diagnostics, re-engineering, and first-stage recycling. Their EU marketing manager explained how increasing the supply of second-life modules can make electric-vehicle batteries more sustainable.

"At present, much of our business revolves around production waste, battery recalls, and accident-damaged units. We work with original equipment manufacturers (OEMs) to derive black mass and other recoverable resources from advanced batteries, predominantly lithium-ion batteries from electric vehicles. This gives us a cross-section view of all the different battery types in circulation."

"We're building an extensive resource of safe dismantling procedures ready for the increased demand in a few years. We support research and partner with universities, trade organisations, and government entities to make the business of batteries safer and more sustainable, minimising environmental impact and supporting the drive towards a circular energy economy."

"We would expect electric vehicle batteries to have a service life of 7-10 years. While the recovered elements from end-of-life batteries will be prized by future battery manufacturers, there's a buoyant market for second-life battery modules in a reasonable state of health. We believe that by diagnosing and recertifying modules for further use in second-life applications, the resource-intensive process which created these batteries in the first place will be honoured across a longer period, minimising environmental impact through increased efficiency."

"Our experience in recycling traditional lead-acid traction, automotive, and industrial batteries has enabled us to refine our processes to achieve a material recovery rate of over 97%. As established recyclers, our knowledge of traditional and more advanced battery chemistries is extensive, and while we're currently focusing on lithium-ion batteries, our processes and business can pivot to many other battery types too. We work in partnership with OEMs to realise increased resource efficiency from electric vehicle batteries, extending the useful life of modules and achieving greater traceability and circularity in the supply chain. As we learn more through these partnerships, we'll strive to improve the materials recovery rate from electric vehicle batteries, mindful of the efficiency we get from lead-acid battery recycling."

For more insight and guidance, get in touch with Owen Edwards.

![]()