Report

Charity sector development report 2024

Find out more about emerging risks and issues in the charities sector, including changes to FRS 102, in our report.

Stay informed on UK automotive - latest news, trends, and insights

Business models in automotive are evolving quickly, fuelled by the move to Net Zero. In this review, you can find out how manufacturers, large and small, are adapting.

Our experts take a deeper look at the pressures driving change for original equipment manufacturers (OEMs) and share latest regulatory updates on government action to decarbonise road transport. We also look at how an ultra-low volume carmaker is stepping into the electric market.

Historically, automotive OEMs sought to reduce their costs by outsourcing the supply and distribution of their vehicles. They applied pressure on tier 1-4 parts suppliers to levels at which the profit margins in some suppliers were only just achievable. The pandemic highlighted the stresses of outsourcing on the OEMs’ supply chain. Technological changes have also pushed OEMs to review supply chains, a key example being the production of batteries and the raw materials associated with the production process. Controlling more of the supply chain dynamic allows the OEM to create a more secure supply chain, improved quality and consistency of the parts supplied and to reduce costs, with less profit margins being given to those third-party tier 1-4 parts suppliers.

The answer is no. OEMs will still retain some third-party providers as they won't be able to bring 100% of the production in-house – since they generally don't have the capital or the technical expertise to undertake all processes. Therefore, we believe that there'll be three business models for OEMs:

![]()

However, we're starting to see a number of OEMs who are moving down the vertical strategic route in order to gain greater control over the most important parts of their supply and distribution chain. The semiconductor shortage has helped fuel this change. Toyota, for example, started to design its own semiconductors and then set up its own factories to produce its own semiconductors. This move has enabled Toyota to create a more secure supply chain – crucial for success in the growth of electric vehicles. It's estimated that between 500 and 1,000 more semiconductors will be required in EVs and autonomous vehicles, and controlling this section of the supply chain is key whether in-house or through partnerships.

Currently, Tesla’s supply chain is one of the most effective and efficient in the automotive industry. The company has no legacy vehicle manufacturing and distribution processes and has therefore been able to construct new and more efficient plants compared with a number of the older OEMs.

Although Tesla continues to use tier 1-4 parts suppliers, the number of these parts providers is being reduced by designing them out of the process, and in some cases by bringing selected processes in-house. For those processes not taken over by Tesla, there'll still be a number of Tesla staff implants in the 1-4 tier parts suppliers to ensure the part's manufacturing consistency and quality. In the first generation of Tesla vehicles, Model S, there were 3,400 of tier 1 parts suppliers and 21,000 of tier 2. In the most recent Model 3 and Model Y vehicles, this has been reduced to 2,100 of tier 1 parts suppliers and 19,000 of tier 2 – and there's increased focus on reducing the parts providers further.

Notwithstanding increased efficiency in vehicle production, OEMs need to secure their raw materials, especially for BEVs. The number of OEMs that have partnered with the large lithium and critical mineral mining companies has increased.

For example, Australia's Pilbara Minerals has a partnership with Great Wall Motor Company in China. Stellantis has a lithium hydroxide offtake agreement with Vulcan Energy Resources in Germany and also has a USD 76 million equity investment in the firm, making Stellantis the firm’s second-largest shareholder. And Tesla has also been prolific in securing supply of its raw materials with offtake agreements with Core Lithium and Liontown Resources.

Refining and battery manufacturing is also key to the process. Tesla has led the way with the construction of the 50 gigawatt Corpus Christi Lithium Refinery in the US. It's also building a 60GW cathode plant in Texas, has gigafactories for batteries in the US (Nevada), Germany and China, and is constructing factories in other areas of the world such as Mexico.

The security of the supply chain is only part of the OEMs’ strategic focus: they're also reviewing other areas of the downstream automotive industry (factory gate to the end consumer). Ford has its own logistics company in the UK, transporting its vehicles from Dagenham to its UK dealers. Some OEMs own their own dealer networks – in the UK, this includes Stellantis and Ford. Furthermore, the agency model also represents a move by the OEMs to enter the new vehicle sales market, ensuring that the OEM has full access to customer details. The agency model is being implemented by Mercedes-Benz and being considered by a number of other OEMs in the UK and Europe.

Used vehicles are also becoming interesting for OEMs wanting to have a presence in this area of the market. Heycar and Motor Depo are owned by OEMs, for example. Stellantis has taken the process a step further with its exposure to the refurbishment vehicle market with Stimcar in France. Others are looking at new areas relating to the customer, such as charging with Ionity, whose OEM partners are Mercedes-Benz, Ford, BMW, VAG and Hyundai. This charging not only serves the UK, but operates across Europe, with a network of 350kW ultra rapid chargers. This follows the strategy being employed by Tesla with its rapid chargers, which is encouraging a greater uptake of customers and customer loyalty to the BEV OEMs.

The OEMs have become increasingly interested in becoming involved in supplying fuel to BEVs. Tesla has already started with the supply of its Powerwall and Solar Roof power generation assets. Mercedes-Benz has launched a US energy division, and Ford and General Motors in the US are becoming involved in Virtual Power Plants working with both retail consumers and B2B customers.

Such a process enables the OEMs and their partners to pool together thousands of decentralised energy resources, such as BEV and powerwalls with permission from customers, to provide this stored power back to the electricity grid. RMI, one the early adopters of this technology, estimates that virtual power plants could reduce US peak demand by 2030 by 60 gigawatts – the average consumption of 50 million households – and by 200GW by 2050.

OEMs are reaching out and positioning themselves in the supply chain and also the distribution and B2C markets. Although the production of vehicles will remain central to the OEMs’ activities, it will become only one activity of many to ensure the security of their supply chain, and their customer and distribution chains, with the aim of ensuring maximum touch points with the consumer.

For more insight and guidance, get in touch with Owen Edwards.

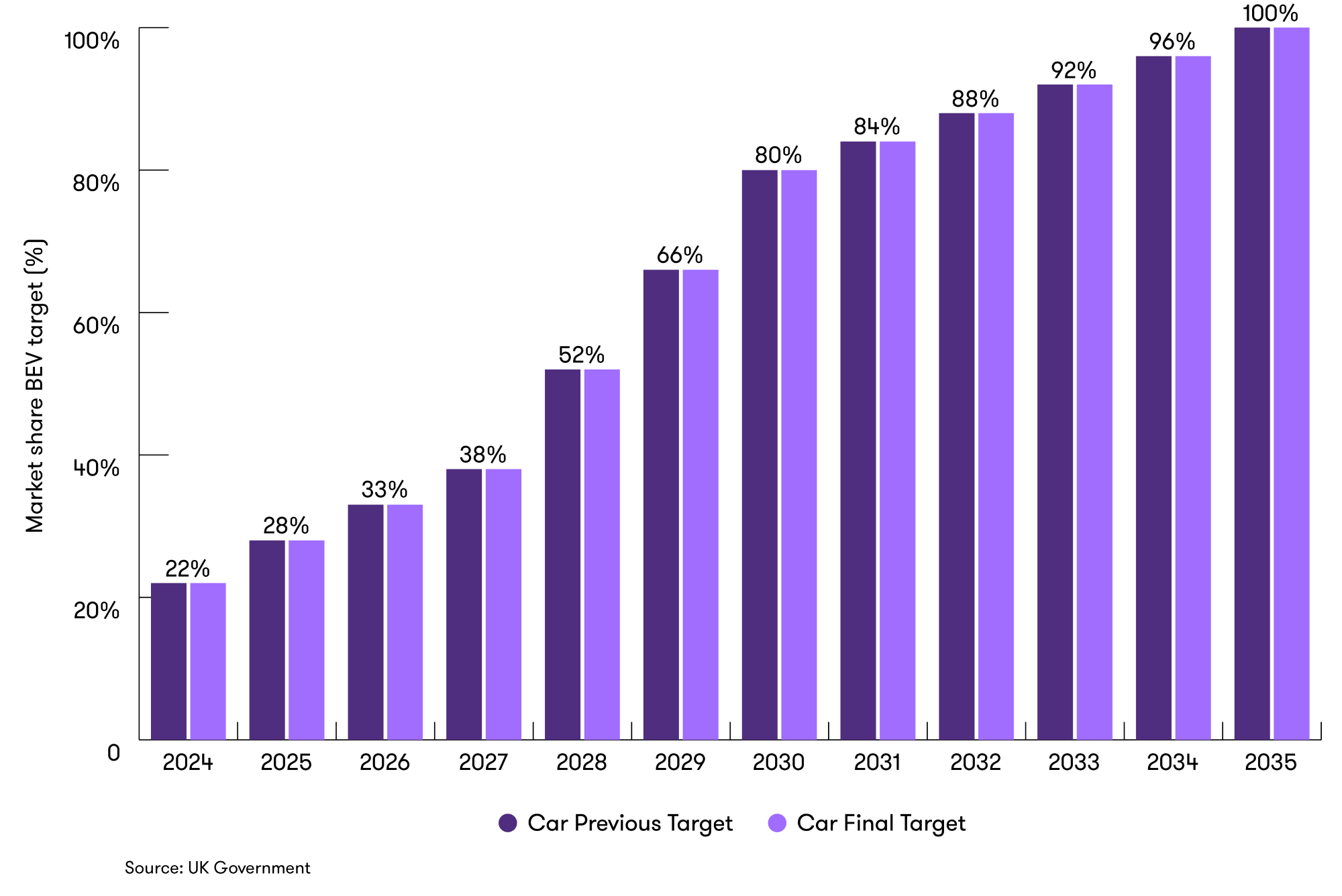

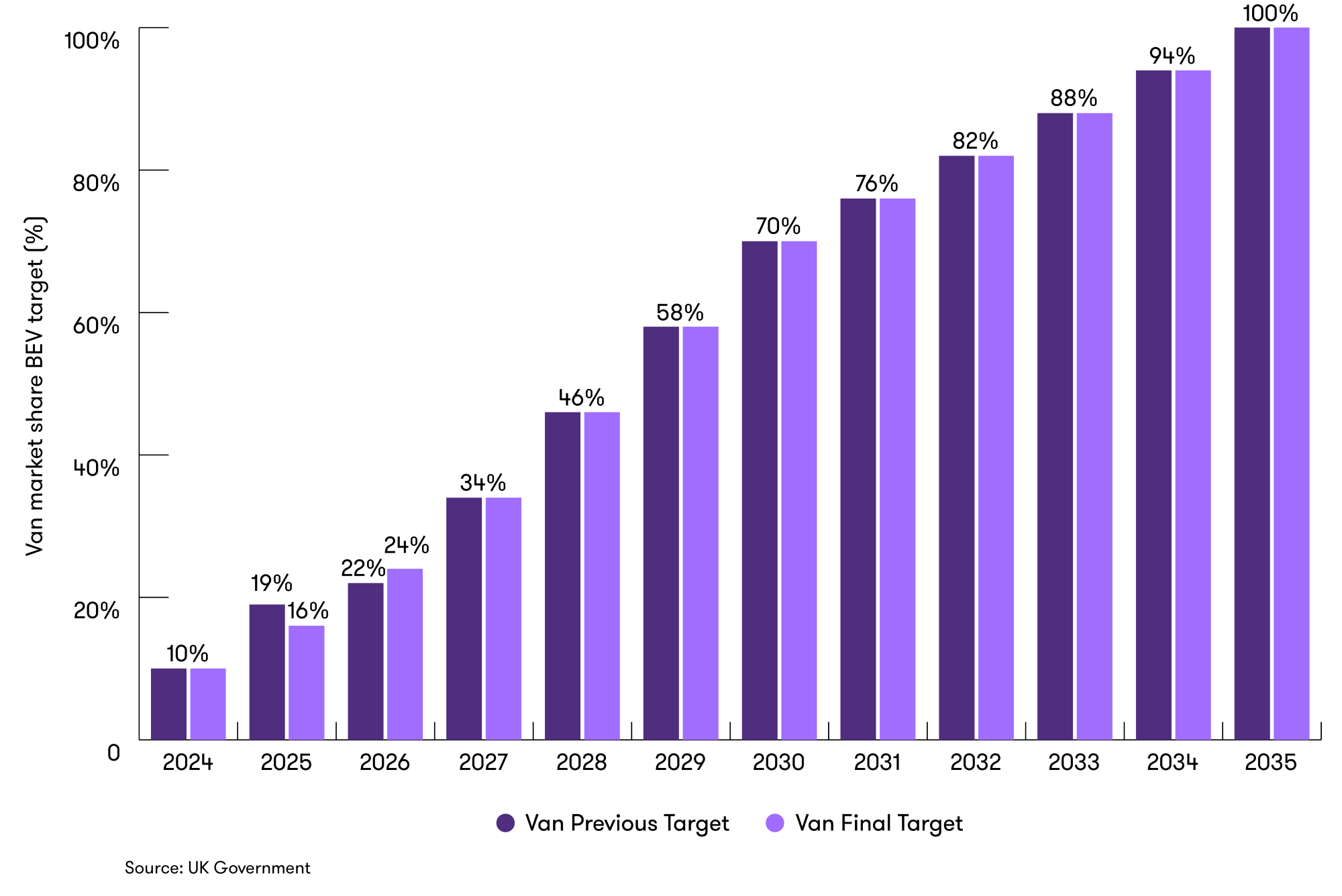

For both for cars and vans, UK government policy was to set a percentage target for new ZEVs registered in the UK between 2024 and 2035. There was little change between the consultation and the joint government response.

There was no change for cars as our chart shows: 22% of all cars registered in 2024 should be ZEVs, and those manufacturers that fail to meet these targets will be fined £15,000 per car. Rules for vans, however, have changed, as the government see the van market as less “mature” and therefore less prepared for the move to become ZEVs.

Car annual targets for ZEV sales share from 2024 to 2035 – previous and final targets

The only significant change from the consultation document and the document released on the 28 September 2023 is an update for vans. The annual target for ZEV sales share for vans in 2024 remains the same but has now fallen from 19% to 16% in 2025, enabling the 2026 target to be increased by 2% to 22% (see chart). The government has indicated that the van market was less mature than cars in its move to a 100% ZEV market. Furthermore, the fines allocated to vans are now less severe in 2024 – with an £8,000 fine per van which misses the target – to then increase in 2025 to the original £18,000 per vehicle.

Van annual targets for ZEV sales share from 2024 to 2035 – previous and final targets

The stipulation for 22% of cars sold by manufacturers presents a challenge for a number of brands and may not be achieved by some original equipment manufacturers (OEM) that have either focused on hybrid vehicles or have a large percentage of their manufacturing process exposed to ICE vehicles.

However, the government has facilitated a flexible approach for vehicle manufacturers who produce less than 2,500 per annum: they won't have to meet the requirements of the ZEV mandate but will have to apply for the exception. Furthermore, all special purpose vehicles will be exempt from the ruling. The government recognises the challenges facing larger OEMs (those with production in excess of 2,500 vehicles per annum) in the car and van segment, and has implemented a ZEV allowance borrow scheme.

Between 2024 and 2027, vehicle manufacturers will be able to borrow allowances for cars – this will be 75% of the ZEV allowance target in 2024, falling to 50% in 2025 and 25% in 2026.

There will be more flexibility for the van sector, with manufacturers able to borrow allowances for vans of 90% of the ZEV allowance target in 2024, falling to 50% for 2025 and 25% in 2026. The allowances can be borrowed at a 3.5% compound interest rate that reflects the lost environmental benefits to society.

There's also an option for OEMs that exceed their allowance across the period of the ZEV mandate to be able to bank allowances for future use, with no limit on numbers but with an expiry date of three years after the year in which it was allocated.

The government has set out a clear policy in the ZEV mandate to ensure the UK tries to meet its net zero commitment. It has also built some flexibility into the implementation process, while still ensuring that the UK will have zero tailpipe emitting vehicles by the end of 2035, bringing the UK in line with the rest of Europe.

For more insight and guidance, get in touch with Owen Edwards.

Caterham has been building the Seven for 50 years and although the design has evolved, the basic architecture of the vehicles has remained the same. There are now changes afoot at the company. Emissions legislation and the move to battery electric vehicles (BEV) has meant that the brand is starting a new chapter in its history with the production of its first designed from the ground up BEV. It's CEO, Bob Laishley, took some time to tell us about its history and its exciting journey into the world of electric vehicles.

"Caterham specialises in lightweight sports cars, most notably the Caterham Seven. The company was founded in 1973 by Graham Nearn, when he acquired the rights to produce the Lotus Seven and this year, throughout 2023, Caterham has been celebrating it’s 50th anniversary as a brand.

The Caterham Seven is a simple, lightweight car that's designed for pure driving enjoyment. It's available in various specifications and power outputs, depending on the customer requirements. From touring weekends to track days and racing, the cars are hugely popular amongst a very enthusiastic group of owners. The Seven is available in both kit and factory-built form, and the global dealer network supports sales across the UK, Europe, Asia and the US."

"Caterham continues to enjoy strong demand globally for the product, with a 10-12 month waiting list across most vehicles. The business owners, VT Holdings, have recently made a significant investment in new factory premises, securing the production of the Seven well into the next decade from the new facility. Located in Dartford, a short distance from the existing location, the new home of Caterham will bring together the majority of the 130 employees under one roof and support an increase in production to more than 700 cars per year.

Legislation means the Seven in its current form as a road car will have a natural shelf-life (in the UK), but there remains a future for the vehicles, especially given that ultra-low-volume carmakers will be allowed to continue using internal-combustion engines indefinitely in Europe. Currently, the US market has been widely untapped for Caterham and provides further opportunities for sales growth in the coming years."

"Caterham is building an aerodynamic electric coupe that will draw on the traditional Caterham values of lightness, performance, simplicity, and agility. This won't be a Seven, but it’ll have all the characteristics today’s Caterham customers know well: lightness, simplicity, agility, performance, and fun to drive. Today there's no EV in the market that focuses on those core Caterham values.

The approach with Project V supports Caterham’s future sustainable growth of the brand in line with the ambitions of our owners. The industry is moving to electric, and so are we as a business."

"Caterham have remained true to the core DNA of the brand, building simple, lightweight, and 'fun to drive' cars that continue to resonate with a passionate community of international owners."

For more insight and guidance, get in touch with Owen Edwards.

Automotive industry trends and predictions for 2024 →

![]()