Report

Charity sector development report 2024

Find out more about emerging risks and issues in the charities sector, including changes to FRS 102, in our report.

There are opportunities in the current circumstances. We're here to help you navigate these choppy waters.

24 February 2021

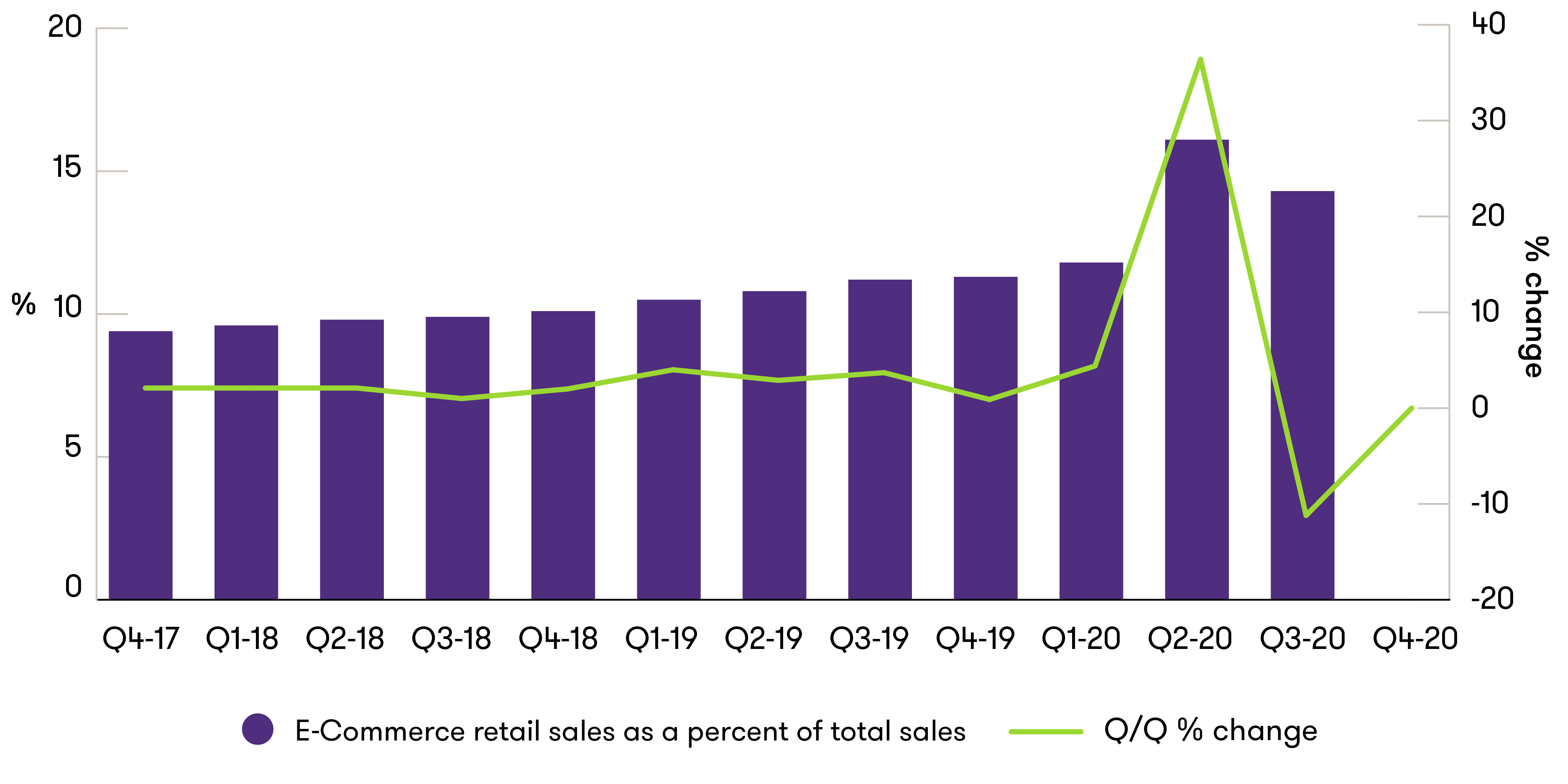

Rising online sales are a key component in this growth. It's the culmination of a decade-long channel shift from high street to online shopping, some of which will be permanent.

The coming months offer courageous management teams an opportunity to reshape their business with a successful retail proposition and take advantage of a new post-COVID-19 landscape.

Here are some of the most pressing issues and opportunities for retailers.

Boosted by a rise in home shopping during lockdown, online retailers outperformed all expectations from April through December. We expect demand for online stores to continue once normality returns and that the sector will maintain a strong performance.

With this surge in online sales being noticed, there was an uptick in M&A activity in the retail sector during the last quarter of 2020. Owners and management teams were keen to capitalise on their hard work by selling equity. These partial exits cleared space for new investors to sit beside existing management, merging new ideas with experienced leadership.

High performance also attracted private equity to take a fresh look at the retail sector and identify strong strategic growth opportunities. An uncertain economy makes valuations challenging, as underlying earnings are subject to outside influence, but there's no doubt the sector is drawing interest.

Private equity houses' keen interest in direct-to-consumer businesses is focused on the online retail sector as consumer demand continues to be altered by world events. This demand for resilient, high-performing businesses will make for a competitive market, and retailers with proven models will command strong valuations.

Recent retail sector M&A activity is showing several common features among acquired firms:

Given the high levels of private equity interest in the space and the increasing volume of transactions, pre-process preparation is more important than ever. This includes financial model preparation.

We believe the volume of retail sector M&A transactions will continue to increase through 2021.

In November 2020, the chancellor announced a review of capital gains tax, which was thought would be reflected in the March budget. This has created a sense of urgency in transactions during the first quarter of 2021.

Although a rise in capital gains tax is now considered less likely, given ongoing lockdown restrictions, this has already driven strong valuations. And while the increase will likely be pushed back to the long term, it will remain a looming driver for the market.

Given the strong performance of the sector and the boost offered by recent events, we feel the retail market will remain active for a long time to come.

If you'd like to discuss M&A opportunities in the retail and ecommerce sector, get in touch with Nicola Sartori.

![]()

All of us are aware of the impact of coronavirus on the high street. But many retailers will also be concerned about the tax reforms for off-payroll workers finally coming into effect in April. This is due to the large number of contractors and outsourced workers in the sector.

When the IR35 reforms were put on hold last year, it was a welcome gift to unprepared businesses. Unfortunately, many took the delays as a sign the reform was to be cancelled and have yet to take the necessary steps to ready themselves.

Some impacted firms don't even have an exact count of the number of contractors they have across their business. For example, designers may bring in other designers without proper visibility.

On the other hand, retailers that have used the extension to assess their contractor model have noticed the value of a flexible workforce. Given the uncertainty of 2020 and the stop-start nature of coronavirus restrictions on retail businesses, there are legitimate commercial reasons to see contractors as invaluable.

Many businesses have been taking a blanket approach to IR35, assessing all contractors as deemed employees or telling them that they must take permanent contracts. Some are now starting to realise this may not be the commercial answer.

The additional national insurance contribution cost of over-prudent assessment has also come sharply into focus. Assessing IR35 is a balance between the tax and people risks, and over-compliance could even be costly. This would particularly be the case if HMRC were to contest that reasonable care was not being taken.

Under-compliance can also come with a cost if HMRC were to challenge any assessments. PAYE and NIC risk would now sit with the end-client or the business that failed to properly pass the Status Determination Statement along the chain. HMRC may also impose penalties and charge interest on any unpaid income tax and NIC.

Equally, let's not overlook the administrative burden of contractor appeals and disputes, which must be responded to within 45 days.

It's crucial you have adequate processes in place for accurate and timely IR35 assessments. And you should also be wary of the well-publicised limitations of HMRC’s Check Employment Status for Tax (CEST) tool.

A potential positive for your business is that many contractors are now less reluctant to be treated as employees. IR35 can be an emotive issue for contractors, who often object to being treated and taxed like an employee. The Coronavirus Job Retention Scheme and similar concerns have changed that mindset.

If anything is certain, it's that you need to prepare for April 2021 and ensure a robust implementation of the IR35 reforms.

For support in preparing your organisation for IR35, get in touch with Michelle Perry.

![]()

ASOS’s £265 million acquisition of four Arcadia brands, which includes Topshop, and Boohoo’s double swoop to buy Debenhams’ intellectual property for £55 million, and three Arcadia brands – Dorothy Perkins, Wallis and Burton – for £25 million have made contentious headlines. The deals will leave the new owners with the brands, but not the hundreds of stores that once formed the bedrock of these high street businesses. Many say this sounds like the death knell of the UK high street.

But could the pure players be missing a trick? The future of high street retail is changing but reports of its death may be greatly exaggerated.

Bricks-and-mortar businesses that can are starting to reshape their offer to meet the challenges of online competition. Meanwhile, commercial rents are falling resulting in lower costs. And while online sales are a rising trend, many shoppers will still prefer to visit a physical store with a brand name they know above the door. There is still everything to play for.

Ironically, I think one of the biggest winners from this buying spree could be the business that walked away from the Arcadia deal.

Next plc chose to drop out of the bidding for Topshop and Topman and allow ASOS to claim the spoils. It also has a beautifully balanced omnichannel business, with just about half its sales in a normal year coming from online retail, and half from its well invested store estate.

The complete loss of the Debenhams' store estate from the UK high street, and the £1.8 billion sales it generated, represents an enticing opportunity for Next, the value of whose UK store sales are remarkably similar in value to Debenhams’. Most former Debenhams store shoppers will not migrate online and, when shops reopen in a few months’ time, Next will undoubtedly gain sales as a result of Debenhams’ and Arcadia’s demise.

If Next can rapidly develop its beauty business, launched in 2018, it could become a legitimate competitor to Frasers Group and the John Lewis Partnership in this lucrative category. It has already acquired five former Debenhams sites in which to do so.

Next will also be a winner in that most of its stores are in prime locations, and it has already agreed deals with many landlords to ensure that it profits from any general rental reductions afforded to its competitors. With multiple vacancies on the high street and in shopping centres, I expect rental levels may fall sharply in the next 12 months and beyond.

Of course, the loss of the better part of 18 million square feet of occupied retail space from the closure of the Debenhams and Arcadia retail stores is a huge challenge. And it won’t be the first or last of the closures.

But retailers like Next, JD Sports and even M&S are likely to benefit from the reduced competition and costs – once shoppers return, as they inevitably will.

With COVID-19 driving consumers towards online shopping and home deliveries, you could be forgiven for thinking that the writing is on the wall for brick-and-mortar retail. Recent UK headline retail casualties that depended on physical locations include Debenhams, Topshop and Edinburgh Woollen Mill at the end of 2020.

Somewhere in between the thrivers and the failures are the survivors: those retailers who have successfully altered their capabilities to address evolving customer buying habits and needs.

Share of online sales decreased as lockdown eased

Many who have shifted to a more pro-active ‘bricks and clicks’ omnichannel sales strategy will now be wondering when and how their sales will re-adjust after markets stabilise. And how they can continue to evolve and integrate the physical and digital retail sides of their business.

Three factors are emerging that will shape the retail landscape and affect decision making:

The role of retail locations varies from pure ‘showroom’ retailers, which feature samples with no sellable inventory, to more traditional store-first retailers that depend on stores for almost all sales and are just beginning to offer online ordering.

There is no golden ratio for in-store versus online sales in a successful bricks-and-clicks strategy, but the penetration of online sales is clearly growing and will continue to do so. Each retailer needs to find the right omnichannel balance by considering the three core factors of inventory, interaction and experience, and planning for trends that continue to tip the scales toward online retail.

![]()